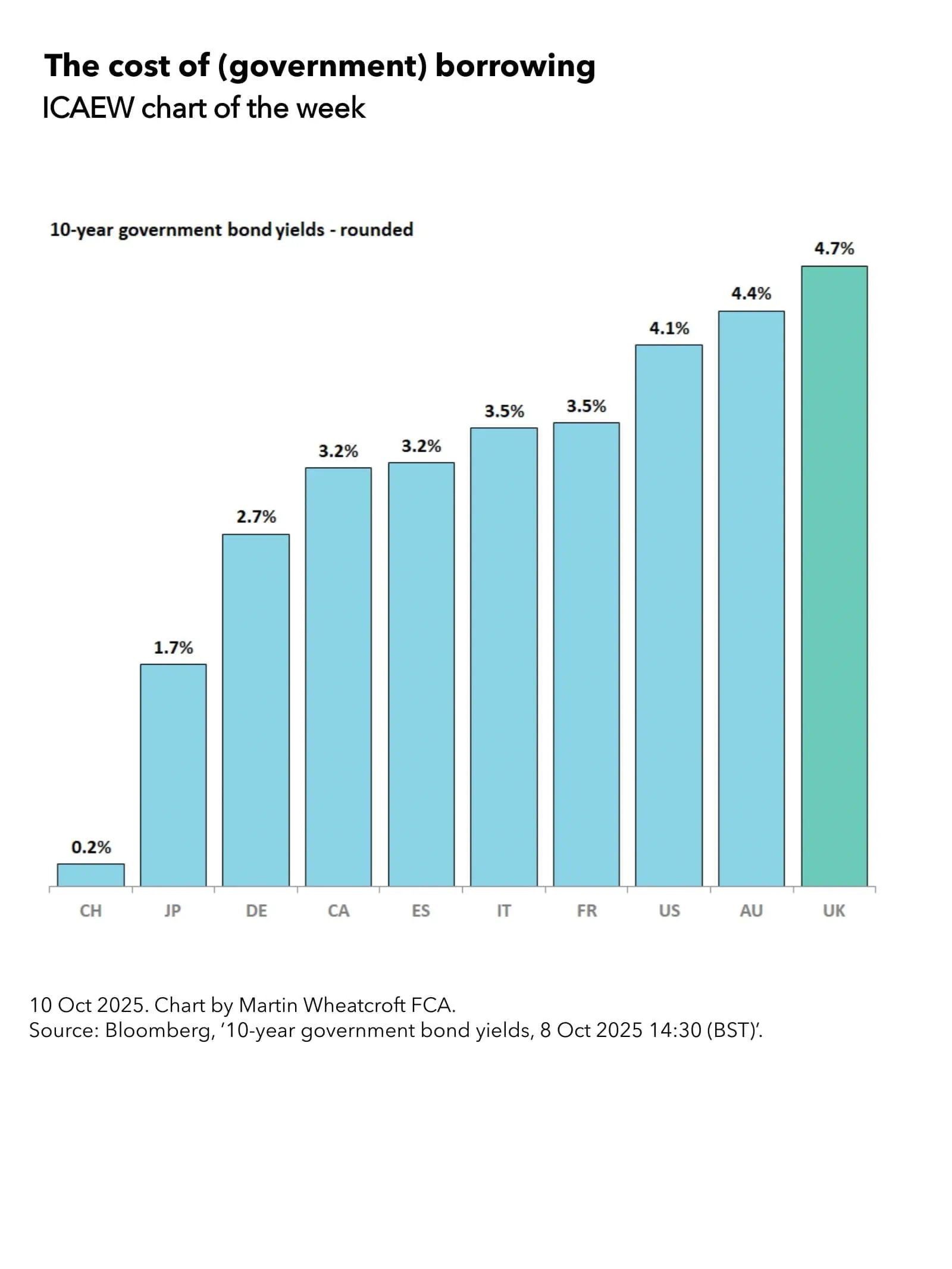

My chart for ICAEW this week looks at the cost of government borrowing by country based on 10-year government bond yields.

The calculated yield on 10-year UK government gilts on Wednesday 8 October 2025 at around 13:00 BST was 4.7% – the effective interest rate the government would need to pay if it had issued new debt at that time.

As my chart of the week for ICAEW illustrates, the UK now has the highest government borrowing cost among developed countries, compared with Switzerland 0.2%, Japan 1.7%, Germany 2.7%, Canada 3.2%, Spain 3.2%, Italy 3.5%, France 3.5%, the US 4.1% and Australia 4.4%.

With debt interest running at around 10% of total public expenditure, the cost of borrowing is a major issue for the Chancellor as she puts together the Autumn Budget 2025.

Reasons for the relatively high borrowing costs in the UK include persistently high inflation, growing public debt, an uncertain economic and fiscal outlook, the Bank of England’s quantitative tightening programme of selling its quantitative easing gilt holdings into the market, and reduced demand from debt investors.

This contrasts with Switzerland, where a strong currency, low public debt (around 37% of GDP), low inflation, and a lower-than-expected forecast for the fiscal deficit in 2025 permits the government to pay almost nothing to borrow at the moment.

Eurozone countries also pay less than the UK, even those with high debt levels such as Italy and France, with lower inflation (2.0% vs 3.8% in the UK in August 2025) being a major driver of lower yields on 10-year government bonds. Canada, with much stronger public finances than most developed countries but rising inflation and trade concerns, is paying more than Germany but approximately the same as Spain.

The US is currently paying 4.1% for new federal government borrowing, with rising inflation and growing fiscal deficits all contributing to a higher risk profile for debt investors. Australia is paying slightly more than the US despite much stronger public finances as it struggles to bring down inflation (3.0% in the year to August 2025).

Not shown on the chart are other countries with lower 10-year borrowing costs than the UK such as Singapore at 1.8%, the Netherlands at 2.8%, South Korea at 2.9%, Portugal at 3.1%, Greece at 3.3%, and New Zealand at 4.2%. There also countries with higher 10-year borrowing costs, including India at 6.5%, Mexico at 8.8%, and Brazil at 14.0%.

For the UK, the headlines have tended to focus on the 5.5% yield payable on 30-year government gilts, but in practice the Debt Management Office is currently issuing very little long-dated debt. The majority of gilts by value are being issued for less than 10 years, reflecting an expectation (or hope) that medium- and long-term borrowing costs will come down over the next few years as inflation returns to target and the volume of quantitative tightening slows.

A substantial proportion of the £3.2tn that the UK public sector current owes (£2.9tn after deducting cash and liquid financial assets) was borrowed when interest rates were much lower, meaning the government is currently paying somewhere in the region of 3% on its debts overall.

Unfortunately, the need to issue £1.3tn in new debt over the next five years (around half to refinance existing debt as it falls due for repayment and another half to finance planned fiscal deficits, lending and working capital requirements) means that the average weighted effective interest rate on UK debt is likely to increase even as the Bank of England base rate (currently 4.0%) is expected to come down.

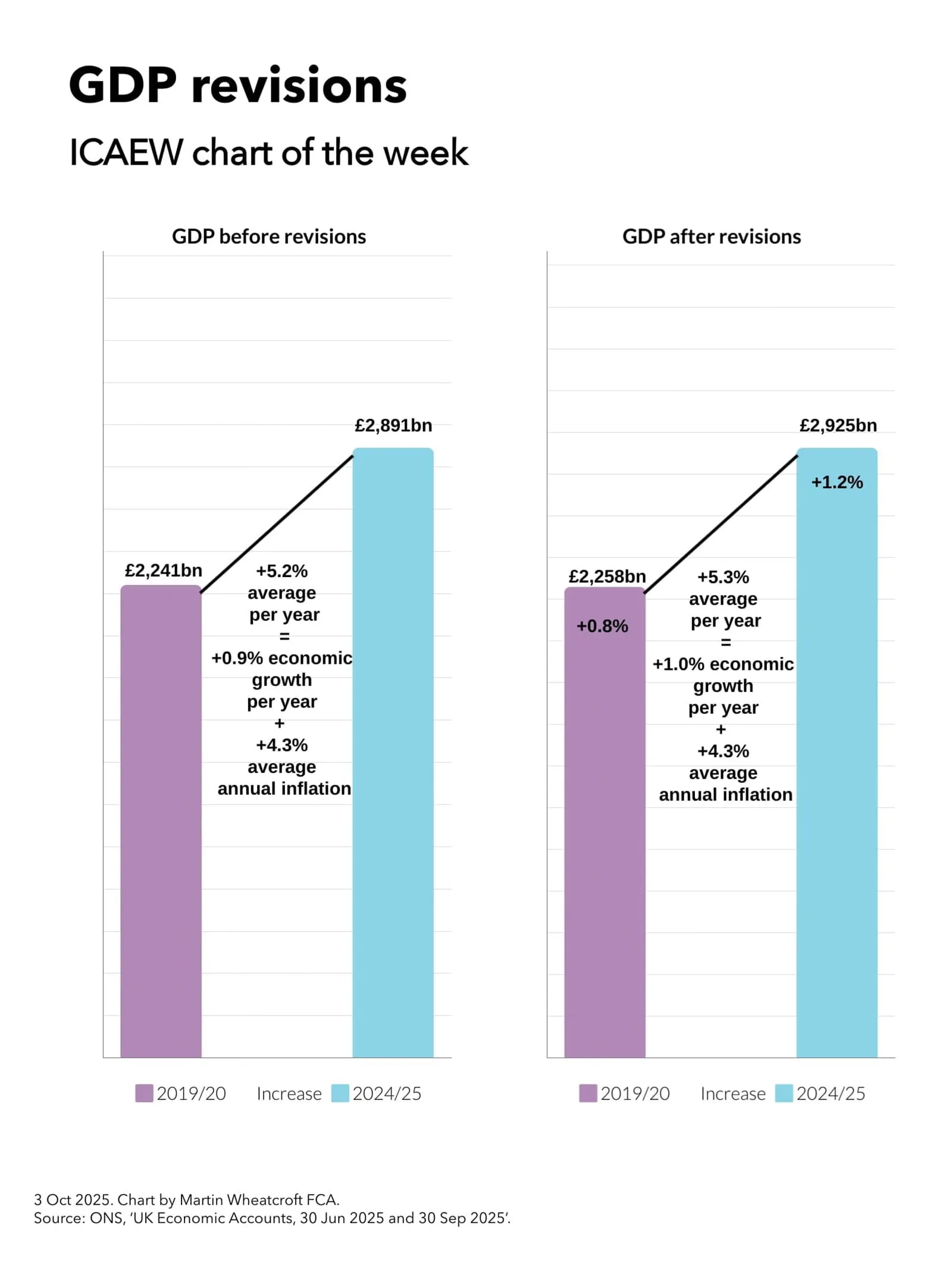

My chart for ICAEW this week looks at how a large upward revision in GDP for 2024/25 translates into a relatively modest 0.1 percentage point increase in economic growth per year since the pandemic.

On 30 September, the Office for National Statistics (ONS) published its latest quarterly GDP statistics for April to June 2025. The headline pointed to a slowdown in quarterly economic growth to 0.3% over that period, down from 0.7% growth in the first quarter of the year. However, more significant was a large revision that increased reported GDP for the year to March 2025 (2024/25) by 1.2%, taking it from £2,891bn to £2,925bn.

The ONS also revised GDP for previous years, including a 0.8% upward revision in reported GDP for 2019/20 from £2,241bn to £2,258bn.

My chart for ICAEW this week illustrates how this resulted in the increase in GDP over the five years to 2024/25, going from an average of 5.2% a year in GDP before revisions, to 5.3% a year after revisions. As inflation is similar before and after the revisions (at an average of 4.3% per year), this means that average annual real economic growth over the past five years has been revised up by 0.1 percentage points from 0.9% a year to 1.0% a year.

While the effect on economic growth over the past five years has been relatively modest, it will knock off at least a percentage point from the public sector net debt to GDP ratio – all without the Chancellor needing to lift a finger.

The statistical revisions reflect the typical process of updating historical numbers for more recent data, such as corporation tax returns that reported higher corporate profits than originally estimated and higher estimates of educational output, business inflation and output of pharmaceutical companies. However, the largest revision was a methodology change that increased the estimate of investment in research and development by approximately 1 percentage point of GDP, bringing the UK more in line with comparable countries in the developed world.

Unfortunately, even with this statistical boost to research and development, the UK still underperforms compared with the US, where economic growth since before the pandemic has been more than twice as fast, as well as lagging (albeit slightly) behind the Eurozone.

ICAEW’s business growth campaign has identified how it has become increasingly too uncertain, too difficult and too expensive to do business in the UK and calls for fundamental reform of tax, regulation and economic policy to support stronger business growth going forward.

Read more in ICAEW’s recommendations on how we can tackle the barriers to improving productivity in our business growth campaign.

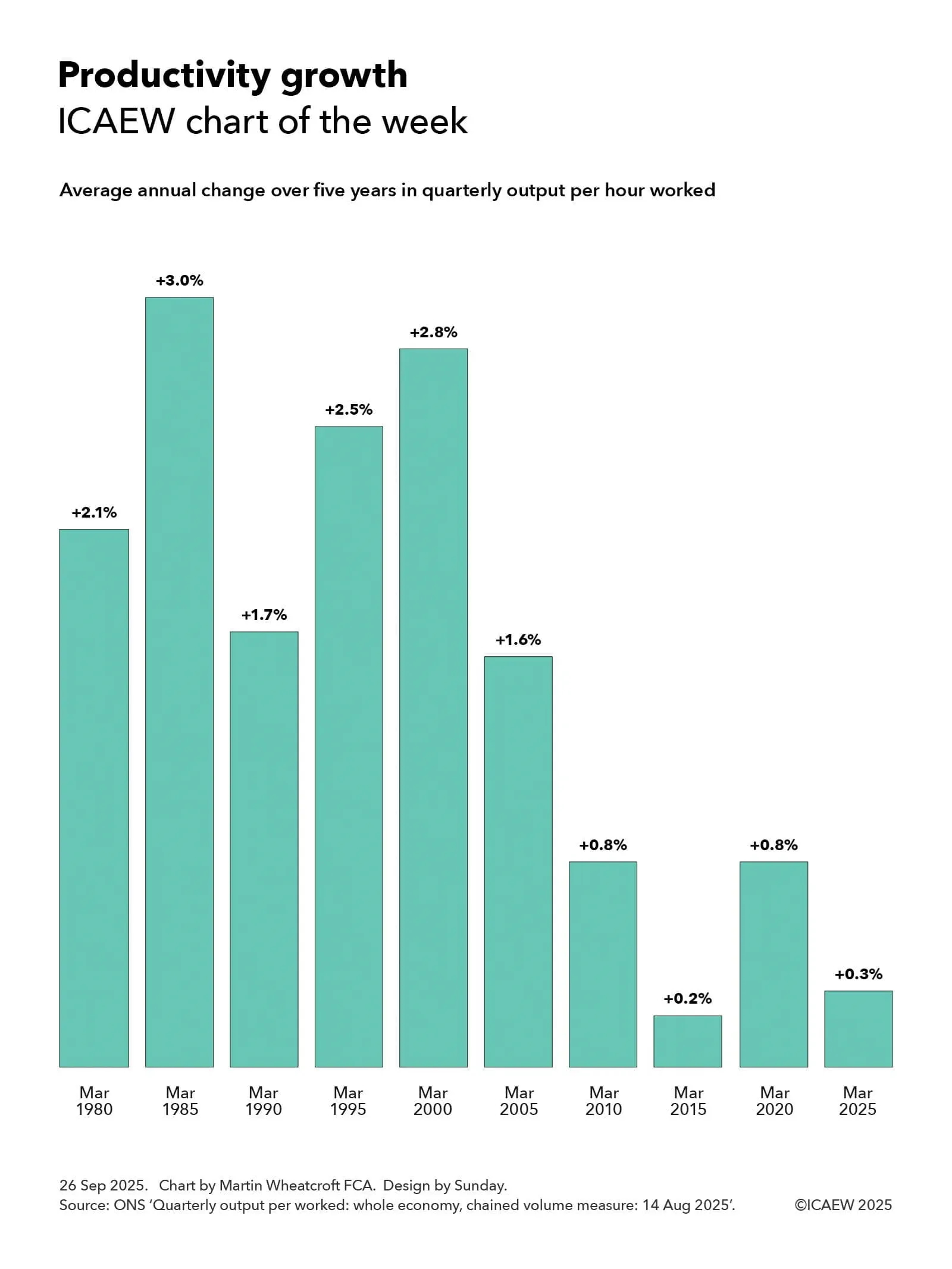

My chart for ICAEW this week looks at how productivity growth has slowed significantly over the past quarter of a century and asks what can be done to turn it around.

One of the biggest challenges facing the UK economy is the decline in productivity growth over the past quarter of a century as illustrated by my chart of the week for ICAEW. This shows how the average annual change over five years in quarterly output per hours worked in March 1980 was the equivalent of 2.1% a year higher than it was in the quarter to March 1975, five years earlier.

The chart also shows how output per hour rose by an annual average of 3.0% a year to March 1985, 1.7% to March 1990, 2.5% to March 1995, and 2.8% to March 2000.

Unfortunately, productivity growth has declined since then with quarterly output per hour increasing by an average of 1.6% a year over the five years to March 2005, 0.8% to March 2010, 0.2% to March 2015, 0.8% to March 2020 and 0.3% to March 2025.

These percentages go a long way to summarising how the UK economy has stalled since the start of the century, especially from the start of the financial crisis in 2007 through the austerity years, Brexit, the pandemic and the energy and cost-of-living crisis. We are producing less value per hour worked even as the population has grown and technology has further advanced.

While the crises we have gone through may partly explain some of the reduction in historical productivity growth over the last quarter of a century, the big question worrying many economists is why productivity has not returned to anywhere close to the levels seen before the turn of the century, or to even to those seen in the USA where, until recently, productivity growth has continued to hold up despite everything.

The Office for Budget Responsibility’s (OBR) most recent economic and fiscal forecast published in March 2025 was based on a central assumption of productivity growth averaging around 1.0% a year over five years to March 2030, significantly lower than the levels seen in the last century. There have been suggestions that the OBR intends to reduce this assumption when it updates its forecasts for the Autumn Budget 2025 in November, adding to the Chancellor’s headaches when she arrives at the despatch box.

One reason for the much lower levels of productivity growth this century may be the demographic change that has resulted in a much higher proportion of the population in retirement and a much older workforce on average. Another may be a question about whether the advent of the smart phone and ‘always on’ connectivity to the office has actually hindered rather than helped people be productive. A further reason could be the increasingly dire state of the public finances with debt rising from less than 35% of GDP in March 2005 to close to 95% of GDP, hampering the government’s ability to deliver the public services we need to thrive, in addition to raising the tax burden to historically high levels.

However, many of the reasons are likely to be driven by the challenges identified by ICAEW’s business growth campaign. This has identified how it has become increasingly too uncertain, too difficult, and too expensive to do business in the UK and calls for fundamental reform of tax, regulation and economic policy to support stronger business growth going forward.

Read more in ICAEW’s recommendations on how we can tackle the barriers to improving productivity in ICAEW’s business growth campaign.

Weaker receipts than expected combined with prior month corrections resulted in a £12bn year-to-date budget overrun in the August monthly public finances.

The monthly public sector finances release for August 2025 published by the Office for National Statistics (ONS) on 19 September reported a provisional shortfall between receipts and total public spending of £18bn in August 2025 and £84bn for the five months then ended. These were £6bn and £12bn over budget respectively and £4bn and £16bn higher than in the same periods in 2024.

Martin Wheatcroft, external adviser on public finances to ICAEW, says: “This month’s public finance numbers took a turn for the worse as not only did weaker than expected receipts drive a £6bn budget overrun in August, but revisions to prior months added a further £6bn to the deficit to turn a broadly neutral position a month ago into a £12bn year-to-date budget overrun for the first five months of the 2025/26 financial year.

“These numbers are far from helpful to a Chancellor in desperate need of some good financial news, adding to the prospect of even higher tax rises in the Autumn Budget 2025 than previously feared.”

Month of August 2025

Receipts of £93bn in August 2025 were £5bn or 5% higher than the same month last year, while total public spending was £111bn, £8bn or 8% more than in August 2024. The latter can be analysed between current spending including depreciation of £107bn, slightly below the £108bn monthly average in the first four months of the financial year, and net investment of £4bn, in line with the monthly average incurred between April and July 2025.

Excluding net investment, the current budget deficit for the month of £14bn represented a £4bn deterioration over the current budget deficit of £10bn in the same month last year, highlighting how receipts have failed to keep pace with increases in current spending.

The overall £18bn fiscal deficit for the month was £6bn over budget and £4bn more than in August 2024.

Five months to August 2025

Table 1 highlights how year-to-date receipts of £477bn were up 6% on last year’s equivalents. This included income tax receipts, up 8% from a combination of inflation and fiscal drag from frozen tax allowances, and national insurance receipts, up 18% as a consequence of the increase in employer national insurance from April 2025. VAT receipts were flat year-on-year, in effect a 3% to 4% fall after taking account of consumer price inflation, highlighting the weak economic conditions facing the UK.

Meanwhile, the 8% increase over last year in current spending including depreciation to £539bn in the first five months to August 2025 has principally been driven by public sector pay rises, higher supplier costs, and the uprating of welfare benefits.

This included a £7bn or 12% increase in debt interest to £64bn, which comprised a £6bn increase in indexation on inflation-linked debt as inflation resurged and a £1bn increase in interest on variable and fixed-interest debt. The latter reflects a higher level of debt compared with a year ago being partially offset by a lower Bank of England base rate.

The resulting current budget deficit of £62bn to August 2025 was 29% higher than the £48bn for the same five months last year, a major concern given that the government’s plan was to reduce the cumulative current budget deficit to £47bn at this point.

Net investment of £22bn in the first five months of 2025/26 was £2bn or 10% higher than the same period last year with capital expenditure of £39bn up by £3bn and capital transfers (capital grants, research and development funding, and student loan write-offs) of £13bn up by £1bn, offset by depreciation of £30bn up by £2bn.

The overall provisional deficit for the five months to August 2025 of £84bn is £16bn or 24% more than in the same five months last year and £12bn higher than budget. The latter can be analysed as a £15bn budget overrun on current receipts less current spending for the year-to-date, less a £3bn saving on net investment.

Table 1: Summary receipts and spending

5 months to Aug

2025/26 £bn

2024/25 £bn

Change %

Income tax

122

113

+8%

VAT

84

84

–

National insurance

80

68

+18%

Corporation tax

43

40

+7%

Other taxes

96

93

+3%

Other receipts

52

51

+2%

Current receipts

477

449

+6%

Public services

(301)

(276)

+9%

Welfare

(129)

(122)

+6%

Subsidies

(15)

(14)

+7%

Debt interest

(64)

(57)

+12%

Depreciation

(30)

(28)

+7%

Current spending

(539)

(497)

+8%

Current deficit

(62)

(48)

+29%

Net investment

(22)

(20)

+10%

Deficit

(84)

(68)

+24%

Borrowing and debt

Table 2 summarises how the government borrowed £99bn in the first five months of the financial year to take public sector net debt to a provisional £2,909bn on 31 August 2025. This comprised £84bn in public sector net borrowing (PSNB) to fund the deficit and a further £15bn to fund government lending and working capital requirements.

The table also illustrates how the debt to GDP ratio increased by 1.6 percentage points from 94.8% of GDP at the start of the financial year to 96.4% on 31 August 2025, with incremental borrowing of £99bn, equivalent to 3.3% of GDP, being partly offset by 1.7 percentage points from the ‘inflating away’ effect of inflation and economic growth adding to GDP, the denominator in the net debt to GDP ratio.

Table 2: Public sector net debt and net debt/GDP

5 months to Aug

2025/26 £bn

2024/25 £bn

PSNB

84

68

Other borrowing

15

7

Net change

99

75

Opening net debt

2,810

2,686

Closing net debt

2,909

2,761

PSNB/GDP

2.8%

2.4%

Other/GDP

0.5%

0.2%

Inflating away

(1.7%)

(2.3%)

Net change

1.6%

0.3%

Opening net debt/GDP

94.8%

95.6%

Closing net debt/GDP

96.4%

95.9%

Public sector net debt on 31 August 2025 of £2,909bn comprised gross debt of £3,339bn less cash and other liquid financial assets of £430bn.

Public sector net financial liabilities were £2,550bn, comprising net debt of £2,909bn plus other financial liabilities of £715bn less illiquid financial assets of £1,074bn.

Public sector negative net worth was £893bn, being net financial liabilities of £2,550bn less non-financial assets of £1,657bn.

Revisions

Caution is needed with respect to the numbers published by the ONS, which are repeatedly revised as estimates are refined and gaps in the underlying data are filled. This includes local government, where the numbers are only updated in arrears and are based on budget or high-level estimates in the absence of monthly data collection.

This month was no different, with the ONS revising the previously reported deficit for the four months to July 2025 up by £6bn, as well as updating prior year numbers for the annual results of the Bank of England and several other public bodies as well as other typical annual updates such as revised student loan calculations.

More significantly, the ONS revised reported deficits back to 1998 for methodology and classification changes and back to 2011 for local government outturn numbers that had not previously been incorporated. The reported deficits for 2020/21 and 2021/22 were decreased by £3bn and £2bn to £311bn and £120bn respectively, 2022/23 remained unchanged at £127bn, 2023/24 was increased by £2bn to £134bn, and 2024/25 was reduced by £2bn to £146bn.

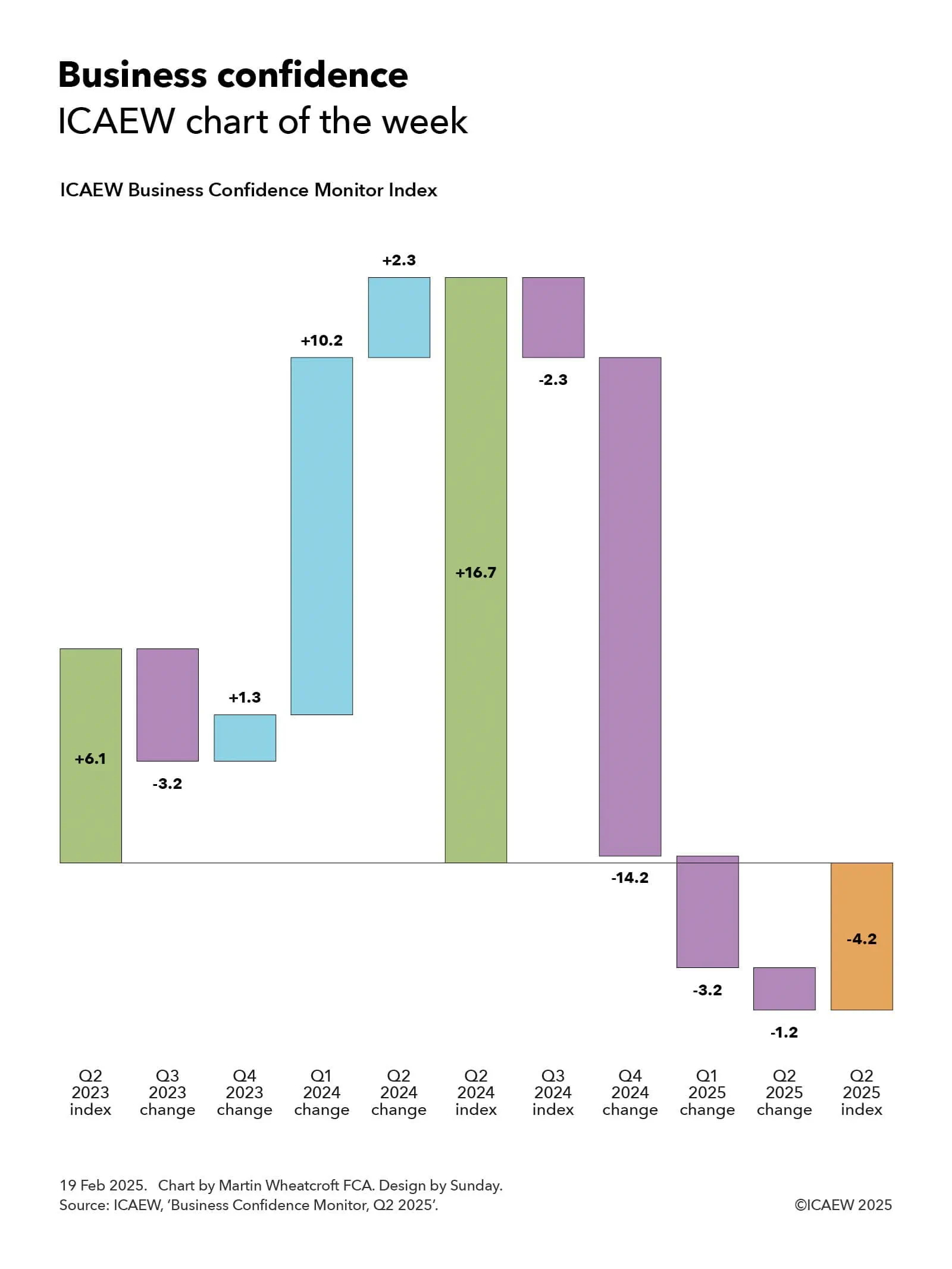

My chart for ICAEW this week looks at how business confidence has entered negative territory, driven by uncertainty about both the economic outlook and potential tax rises.

One of the major themes of ICAEW’s growth campaign is how uncertainty for businesses can be tackled in order to improve business sentiment and hence the appetite of businesses to invest.

My chart for ICAEW this week highlights how business confidence as measured by the ICAEW Business Confidence Monitor (BCM) Index rose from +6.1 in the second quarter 2023 to +16.7 a year later, before crashing over the past year to -4.2 in Q2 2025.

The +6.1 score in Q2 2023 was a significant improvement over the -20.1 registered half a year earlier in Q4 2022 at the height of the cost-of-living crisis. It was also better than the +4.1 pre-pandemic average and +5.0 overall average measured by the BCM Index.

As the chart shows, the index declined in Q3 2023 by -3.2 (to 2.9) but then rose by 1.3 in Q4 2023 (to 4.2), by 10.2 in Q1 2024 (to 14.4), and by a further 2.3 in the second quarter of 2024 to reach a peak of 16.7 following the general election and the consequent change in government.

Unfortunately, business sentiment has declined rapidly over the past year, with the BCM Index falling by 2.3 in Q3 2024 (back to 14.4) and by a huge 14.2 in the fourth quarter last year (to 0.2, only just positive). The index turned negative this year with a decline of 3.2 in Q1 2025 (to -3.0) and then a further fall of 1.2 in Q2 2025 to reach a score of -4.2 in the most recent calendar quarter.

According to the BCM commentary, the business sentiment score of -4.2 in Q2 2025 marked a fourth consecutive decline during a period of heightened global uncertainty and weakening UK activity. Confidence among exporters was particularly downbeat, falling into negative territory for the first time in almost three years.

Domestic sales growth had slowed during the second quarter and businesses had lowered their expectations about domestic and exports sales for the coming year. Concerns about customer demand and competition in the marketplace had risen sharply, while regulatory requirements continued to be the second biggest challenge for businesses.

The tax burden remained the greatest growing challenge in Q2 2025, with the reported rate close to the survey high, and these concerns rose to new record highs in some key sectors.

Expectations for employment growth in the year ahead dropped to the lowest level since Q3 2020, but businesses expected salary growth to continue to ease, adding to the more positive outlook for inflationary pressures than reported in the previous quarter.

Confidence declined in most sectors surveyed and sentiment remained highly unequal, with confidence most negative in manufacturing and engineering, and retail and wholesale; and most positive in information and communication, and construction.

More detail about business confidence by sector and by regions is available in the ICAEW Business Confidence Monitor section of the ICAEW website.

More detail on how it is too difficult, expensive and uncertain to do business in the UK, and ICAEW’s call for the government to do what it can to streamline regulations, reduce unnecessary costs, and provide businesses with the confidence that they need to invest, is available on ICAEW’s growth campaign.

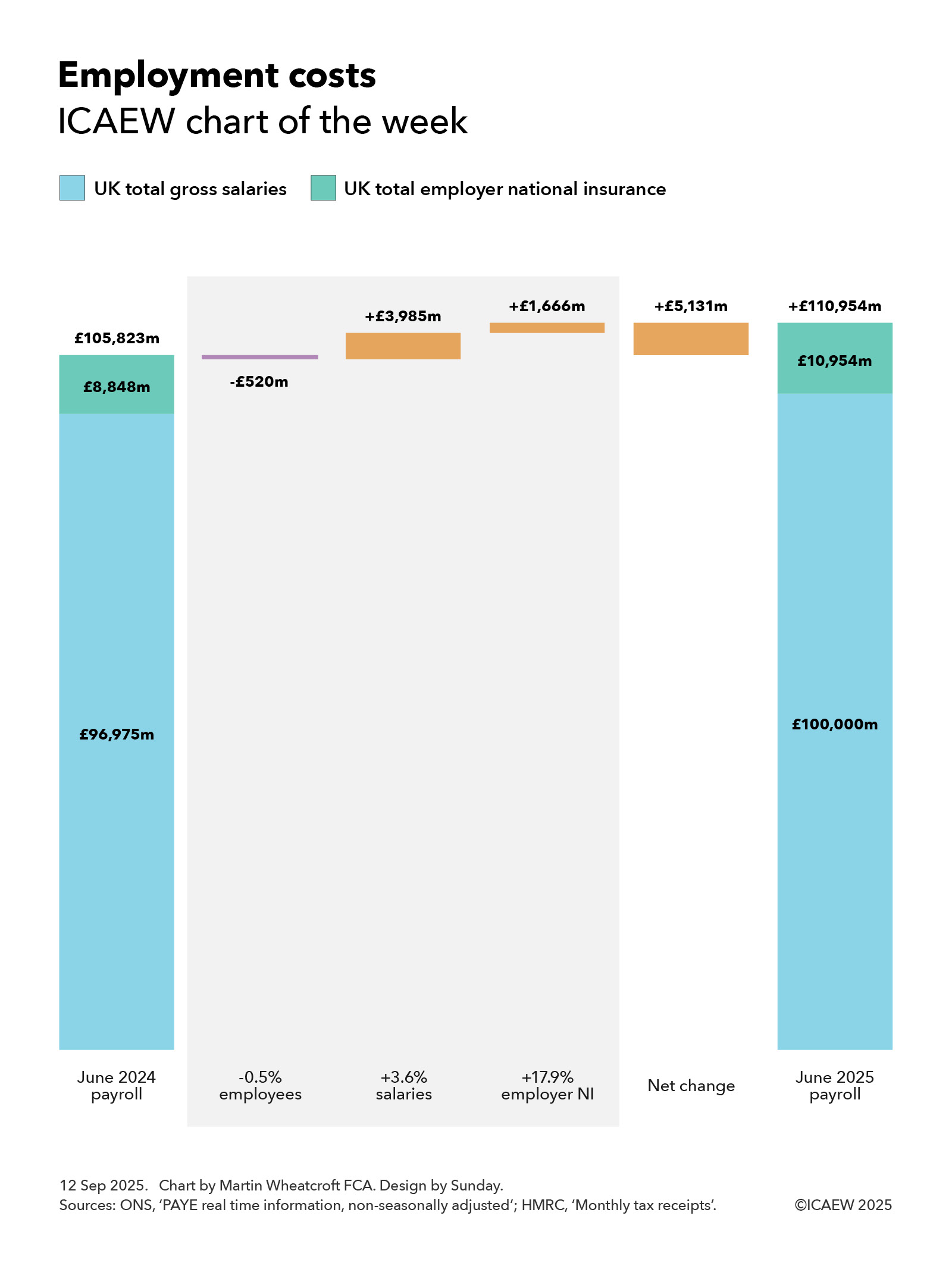

My chart for ICAEW this week looks at how employment costs in June 2025 have risen by 4.8% compared with the same month last year, adding to the expense of doing business in the UK.

According to the Office for National Statistics (ONS) and His Majesty’s Revenue and Customs (HMRC), UK employers paid a total of £111bn in gross salaries and employer national insurance in June 2025, an increase of £5.1bn or 4.8% over the same month a year ago.

My chart this week starts with the payroll in June 2024 of £105,823, comprising gross salaries paid by employers of £96,975m and employer national insurance of £8,848m, although it excludes employer pension contributions.

This monthly cost was reduced by £520m from a reduction in the national workforce, which saw the number of payrolled employees drop by 149,937 or 0.5% from 30,532,600 in June 2024 to 30,382,663 in June 2025. This arose from 7,296,859 leavers exceeding 7,146,922 joiners, most of which are people moving jobs. The reduction in the number of payrolled employees at a time of still-rising overall population numbers highlights the difficult economic situation currently facing the UK. The reduction comprised £476m in less pay and £44m in less employer national insurance (calculated at last year’s rates)

Salary increases since last year of approximately 3.6% added £3,985m or 3.8% to the cost of employment, with mean salaries increasing from £3,176 in the month of June 2024 to £3,291 in the month of June 2025. This comprised an increase of £3,501m or 3.6% in gross salaries and an estimated increase in employer national insurance of £484m or 5.5% (based on last year’s rates).

The median monthly salary increased from £2,389 in June 2024 to £2,530 in June 2025, which is a 5.9% increase compared with a year previously. This was less than monthly pay at the 25th percentile, which increased by 7.8% from £1,408 to £1,518, which was partly driven by a 6.7% increase in the minimum wage implemented in April 2025 (16.3% for those aged 18 to 20 and 18% for those aged under 18) that help lift the salaries of lower paid workers.

Pay at the 75th percentile increased by 4.7% (from £3,632 to £3,803) compared with a year previously, while pay at the 95th and 99th percentiles increased by 3.1% (from £7,461 to £7,692) and 2.6% (from £15,181 to £15,583) respectively. These lower rates of increase for higher paid workers primarily relate to base pay and so do not tell the full story as bonuses and other variable compensation for 2025 will in most cases not show up in pay packets until early next year.

A further £1,666m or 1.5% was added to the total cost of employment as a consequence of changes in employer national insurance effective from April 2025. These took the rate payable by employers from 13.8% of salaries over £792 a month to 15.0% of salaries above £417 per month, adding an extra 17.9% to the amount paid in employer national insurance after taking account of changes in the number of payrolled employees and salary increases since last year. Just under half of the increase (£808m) resulted from the change in the main rate of employer national insurance going up from 13.8% to 15.0% on salaries above £792 a month, with the balance (£858m) coming from lowering the threshold at which the 15.0% applies to £417 per month.

The overall effect was a net increase of £5,131m or 4.8% in total pay and employer national insurance to £110,954m in June 2025, comprising a net increase of £3,025m or 3.1% in total gross salaries to £100,000m and a net increase of £2,106m or 23.8% in employer national insurance to £10,954m.

The chart does not reflect the full cost of employment as it does not include employer pension contributions, non-payrolled benefits, and employment-related costs such as facilities, equipment, training and travel amongst others. However, it still gives a useful illustration of how payroll costs have changed significantly over the course of one year.

ICAEW’s growth campaign identifies how it is too difficult, expensive and uncertain to do business in the UK and calls for the government to do what it can to streamline regulations, reduce unnecessary costs, and provide businesses with the confidence they need to invest.

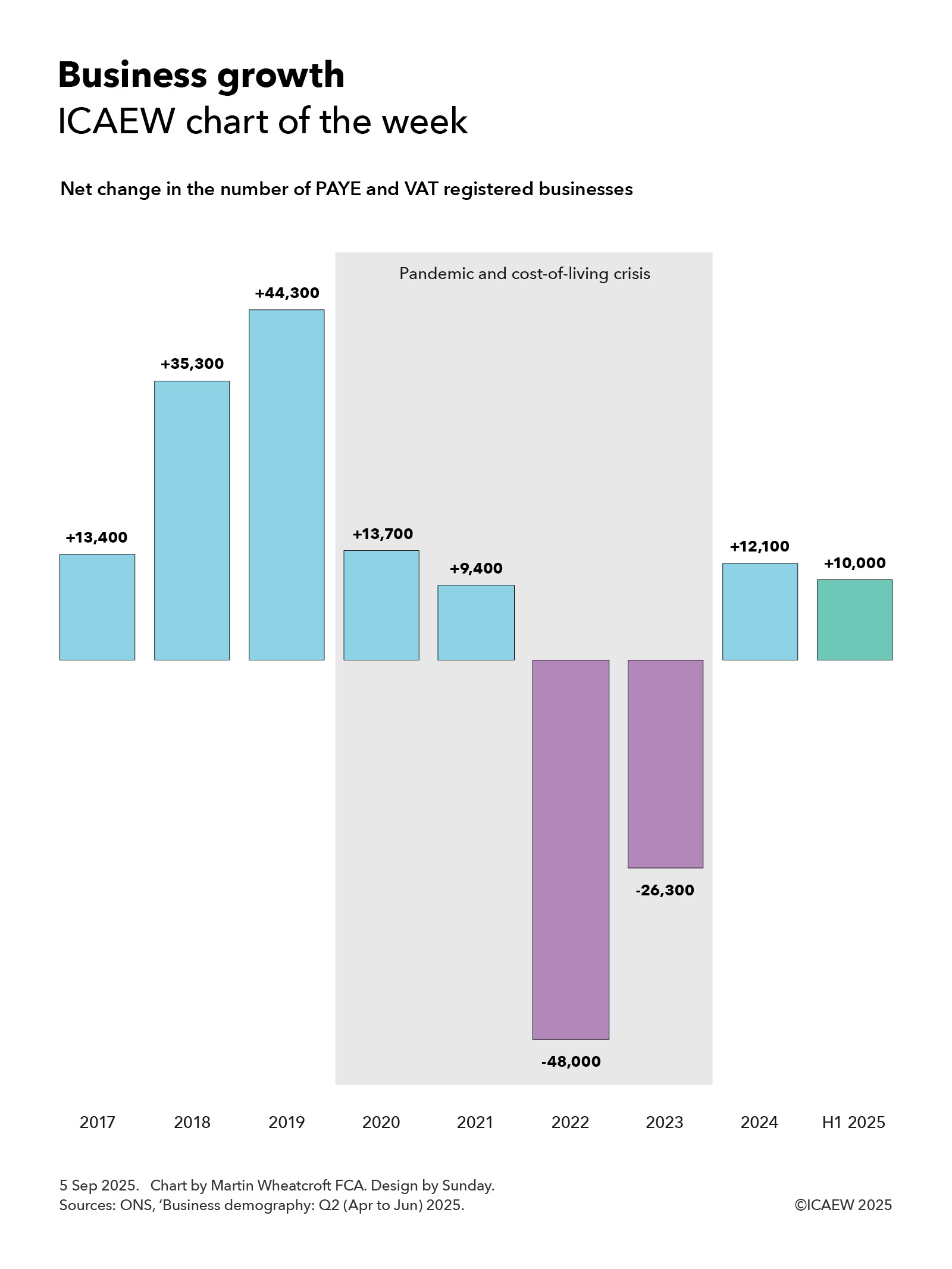

Our chart this week asks whether the recent low rate of growth in numbers of businesses registered for PAYE and VAT is linked to the increasing difficulty of doing business in the UK.

According to the Office for National Statistics, there were net additions of approximately 13,400, 35,300 and 44,300 to the UK inter-departmental business register in 2017, 2018 and 2019 respectively. This was followed by net additions of 13,700 and 9,400 in 2020 and 2021 during the pandemic and then net reductions of 48,000 and 26,300 in 2022 and 2023 during the cost-of-living crisis.

The register started growing again in 2024 with net additions of 12,100, followed by a net increase of approximately 10,000 in the first half of 2025. This rate of increase is significantly lower than the average rate of net business formation before the pandemic but is a significant improvement over the net contraction in the number of businesses in 2022 and 2023 during the cost-of-living crisis.

The net changes are equivalent to 0.5%, 1.3%, 1.6%, 0.5%, 0.3%, -1.7%, -1.0% and 0.4% in the total number of registered businesses in 2017 to 2024 respectively and annualised growth of 0.7% in the first half of 2025.

The total number of PAYE and VAT registered businesses is projected to have reached around 2.75m in June 2025, based on the last published count for March 2024 plus reported movements since then. This is out of an overall total of somewhere in the region of 5.5m businesses in the UK, with the difference mainly due to single-person companies and sole traders that do not employ any staff and operate below the VAT threshold of £90,000 per year.

The approximately 2.75m registered businesses can be analysed into just under 2.1m companies and other types of corporations, approximately 400,000 sole proprietors, 150,000 or so partnerships, and around 100,000 non-profit bodies, mutual associations and public sector organisations. Approximately 945,000 registered businesses are in London and the South East, 675,000 are in the Midlands and the East of England, 535,000 in the North of England, 340,000 in the South West of England and Wales, 175,000 in Scotland, and 80,000 in Northern Ireland.

Business births between 2017 and 2024 were approximately: 338,700; 341,100; 355,700; 322,000; 354,300; 327,500; 307,100; and 310,100; there were 167,600 in the first half of 2025. Business deaths in 2017 to 2024 were: 325,300; 304,800; 311,400; 308,300; 344,900; 375,500; 333,400; and 298,000; with 157,600 in the first half of 2025.

The overall change in the total number of registered businesses between 2017 and the first half of 2025 was 63,900, an average of 7,500 or 0.3% a year over eight and a half years, comprising an annual average of 332,100 business births less 324,600 business deaths in that time.

The chart highlights both the very difficult economic times we have been through in the past few years with the pandemic and cost-of-living crisis and the current period of weak economic growth that has yet to return to pre-pandemic levels.

One of the key ways that we can increase the rate of net business formation is to make it easier to do business in the UK, as discussed in ICAEW’s growth campaign. This asks why it is too difficult, too expensive and too uncertain to do business in the UK today and suggests ways the government can streamline regulation, reduce costs and unnecessary frictions, and provide businesses with greater confidence to invest and grow.

Borrowing to fund the deficit in the first four months of the financial year of £60bn was in line with expectations.

The monthly public sector finances release for July 2025 published by the Office for National Statistics (ONS) on 21 August reported a provisional shortfall between receipts and total public spending of £60bn for the four months ended 31 July 2025. This is in line with budget and £7bn more than in the same period last year.

Martin Wheatcroft, External Adviser on Public Finances to ICAEW, says: “This month’s ‘not bad’ result may provide a small amount of relief to a Chancellor under significant pressure.

“The monthly deficit for July was slightly better than expected, while the cumulative result for the first third of the financial year was almost exactly in line with the Office for Budget Responsibility’s prediction at the time of the Spring Statement 2025.

“Unfortunately, this does not change the dismal outlook for the public finances and the rising costs of public services, welfare provision and debt interest that means the Chancellor is again having to work out how she can ask Parliament to authorise higher levels of taxation.”

Month of July 2025

Receipts of £108.8bn in July 2025 were £9.2bn or 9% higher than in July 2024 and also higher than the £92.6bn average for the first three months of the financial year, principally as a result of a boost from income tax self-assessment collections in the month.

Meanwhile, current spending including depreciation of £105.5bn in July was £6.0bn or 6% more than in the same month a year previously. This was slightly lower than the £108.0bn monthly average incurred during April to June 2025.

The result was a current budget surplus for the month of £3.3bn, a £3.2bn improvement over the current budget surplus of £0.1bn in the same month last year.

Net investment of £4.4bn in July 2025 was £0.9bn more than the £3.5bn incurred in July 2024 and slightly higher than the £4.2bn average incurred during the three months to June 2025.

The provisional fiscal deficit for July 2025 was therefore £1.1bn, £1.0bn less than the £2.1bn budget for the month and a £2.3bn improvement over the £3.4bn deficit in July 2024.

Four months to July 2025

Table 1 highlights how year-to-date receipts of £387bn were up 7% on last year’s equivalents, with income tax receipts up 8% from a combination of inflation and fiscal drag from frozen tax allowances, and national insurance receipts up 19% as a consequence of the increase in employer national insurance that was implemented in April 2025.

Meanwhile, the 8% increase over last year in current spending including depreciation to £430bn in the first four months to July 2025 was primarily as a consequence of public sector pay rises, higher supplier costs, and the uprating of welfare benefits.

This included a £6bn or 13% increase in debt interest to £53bn, which comprised a £5bn increase in indexation on inflation-linked debt as inflation resurged and a £1bn increase in interest on variable and fixed-interest debt. The latter was primarily the result of a higher level of debt compared with a year ago partially offset by a lower Bank of England base rate.

The resulting current budget deficit of £43bn to July 2025 was 16% higher than for the same four months last year.

Net investment of £17bn in the first four months of 2025/26 was £1bn or 6% higher than the same period last year. Capital expenditure of £30bn was up by £1bn and capital transfers (capital grants, research and development funding, and student loan write-offs) of £11bn were up by £2bn, less depreciation of £24bn that was up by £2bn compared with the same four month period a year prior.

The consequence is a provisional deficit for the first third of the 2025/26 financial year of £60bn, which is £7bn or 13% more than in the same four month period last year. Despite being almost exactly in line with budget (only £0.1bn higher) this is the third-highest April-to-July deficit since monthly records began in 1993 (after 2020/21 and 2021/22 during the pandemic).

Table 1: Summary receipts and spending

4 months to July

2025/26 £bn

2024/25 £bn

Change %

Income tax

100

93

+8%

VAT

70

67

+4%

National insurance

64

54

+19%

Corporation tax

35

32

+9%

Other taxes

76

74

+3%

Other receipts

42

41

+2%

Current receipts

387

361

+7%

Public services

(239)

(221)

+8%

Welfare

(103)

(97)

+6%

Subsidies

(11)

(11)

–

Debt interest

(53)

(47)

+13%

Depreciation

(24)

(22)

+9%

Current spending

(430)

(398)

+8%

Current deficit

(43)

(37)

+16%

Net investment

(17)

(16)

+6%

Deficit

(60)

(53)

+13%

Borrowing and debt

Table 2 summarises how the government borrowed £81bn in the first third of the financial year to take public sector net debt to a provisional £2,891bn on 31 July 2025. This comprised £60bn in public sector net borrowing (PSNB) to fund the deficit and £21bn to fund government lending activities and working capital movements.

The table also illustrates how the debt to GDP ratio increased from 94.8% of GDP at the start of the financial year to 96.1% on 31 July 2025, with the incremental borrowing partly offset by the ‘inflating away’ effect of inflation and economic growth adding to GDP, the denominator in the net debt to GDP ratio.

Table 2: Public sector net debt and net debt/GDP

4 months to July

2025/26 £bn

2024/25 £bn

PSNB

60

53

Other borrowing

21

(1)

Net change

81

52

Opening net debt

2,810

2,686

Closing net debt

2,891

2,738

PSNB/GDP

2.1%

1.9%

Other/GDP

0.7%

–

Inflating away

(1.5%)

(1.9%)

Net change

1.3%

–

Opening net debt/GDP

94.8%

95.6%

Closing net debt/GDP

96.1%

95.6%

Public sector net debt on 31 July 2025 of £2,891bn comprised gross debt of £3,309bn less cash and other liquid financial assets of £418bn.

Public sector net financial liabilities were £2,525bn, comprising net debt of £2,891bn plus other financial liabilities of £707bn less illiquid financial assets of £1,073bn. Public sector negative net worth was £899bn, being net financial liabilities of £2,525bn less non-financial assets of £1,626bn.

Revisions

Caution is needed with respect to the numbers published by the ONS, which are repeatedly revised as estimates are refined and gaps in the underlying data are filled. This includes local government, where the numbers are only updated in arrears and are based on budget or high-level estimates in the absence of monthly data collection.

The latest release saw the ONS revise the previously reported deficit for the three months to June 2025 up by £1bn. The ONS also revised up its estimate of GDP in the first quarter of the financial year, resulting in a 0.4 reduction in the opening debt to GDP ratio on 1 April 2025 from 95.2% to 94.8% and the debt to GDP ratio for 30 June 2025 from 96.2% to 95.8%.

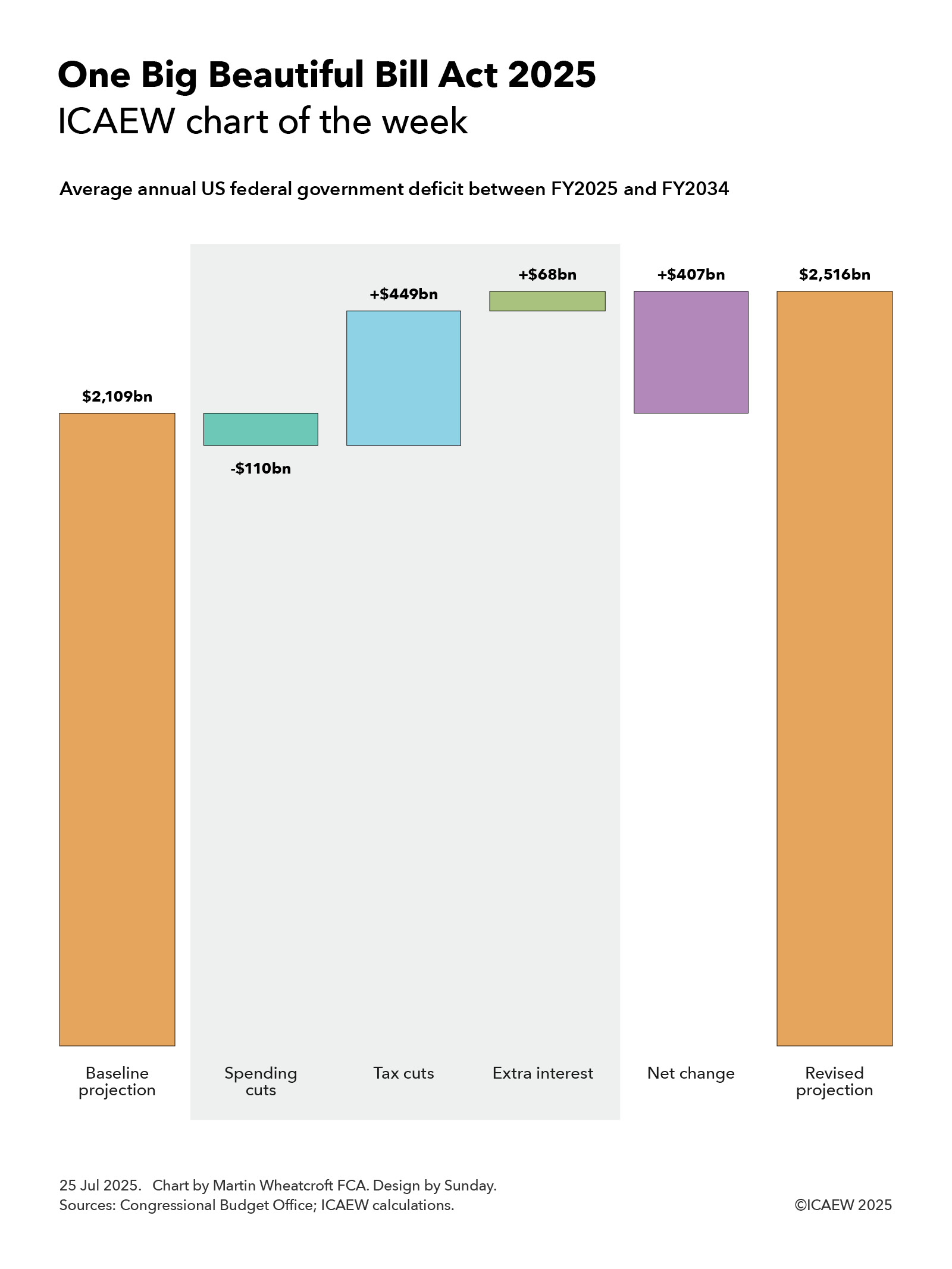

My chart for ICAEW this week looks at the impact on the US federal government deficit of the major tax and spending changes passed by Congress and signed into law by President Trump on 4 July 2025.

My chart this week looks at the impact on the US federal government deficit of the major tax and spending changes passed by Congress and signed into law by President Trump on 4 July 2025.

The Congressional Budget Office (CBO) published on 21 July 2025 its assessment of Public Law 119-21 (the 21st law passed by Congress in its 119th session), also known as the One Big Beautiful Bill Act 2025 (OBBBA).

OBBBA was passed by Congress and signed into law by President Trump on 4 July 2025 and contains sweeping changes to the US federal tax system as well as a significant shift in spending priorities.

The chart this week attempts to illustrate the impact of OBBBA on the federal deficit by looking at how it changes the average annual projected deficit over the next 10 years from FY2025 (the current fiscal year ending on 30 September 2025) to FY2034, compared with the CBO’s baseline projection.

The baseline projection, published by the CBO in January 2025, was for the federal government deficit to increase from $1,865bn in FY2025 to $2,597bn in FY2034, an average deficit over the 10 years of $2,109bn or 5.8% of GDP.

According to the CBO, OBBBA is expected to increase the federal deficit each year by $339bn on average over the period to FY2034, with a net cut in federal spending of $110bn on average offsetting a net cut in revenues of $449bn. The CBO’s assessment does not take account of the additional cost of financing these higher deficits, which ICAEW calculates would add a further $68bn a year on average to the interest bill.

The consequence is a net increase in the annual federal deficit of $407bn on average over 10 years, taking it to an average of $2,516bn or 7.0% of GDP.

Net spending cuts of $110bn comprise spending increases of $66bn a year on average, net of spending reductions of $164bn a year and incremental ancillary income that is deducted from spending of $12bn. Extra spending includes an extension of child tax benefits ($19bn a year on average) and more money for homeland security and immigration enforcement ($18bn), the military and coastguard ($17bn), farm subsidies ($5bn), air traffic control ($1bn), the mission to Mars ($1bn) and other items ($5bn).

Spending reductions include cuts in Medicaid and Medicare programmes ($106bn on average each year), education and student loan relief ($30bn), other welfare and health programmes ($19bn), clean energy subsidies ($8bn) and other cuts ($1bn), while ancillary income comprises $9bn on average from spectrum auctions, $2bn from oil and gas leases, and $1bn extra from higher visa fees.

Net tax cuts comprise $511bn a year in tax cuts less $62bn a year in tax increases.

Tax cuts include making previous temporary tax cuts permanent ($379bn), business tax reforms ($97bn), personal tax reforms ($26bn), energy related tax credits ($4bn), Medicaid and Medicare related tax deductions ($3bn), and other ($2bn). Tax increases include the termination of tax reliefs for clean energy ($47bn a year), addressing tax loopholes ($6bn), additional immigration fees included in revenue ($4bn), taxing low-value international shipments ($4bn) and other ($1bn).

The CBO doesn’t directly conclude what this will mean for the US national debt (debt held by the public), which was expected in January’s baseline projection to increase from $28.2tn or 98% of GDP at the start of the current financial year to $49.5tn or 117% of GDP on 30 September 2034. Adding $4.1tn over 10 years to that amount suggests this would increase to $53.6bn or 127% of GDP.

These numbers don’t take account of the anticipated economic boost of lower taxes that should partially offset some of the tax impacts set out in the CBO’s analysis, as well as increasing the denominator in the deficit to GDP ratio. However, they also don’t take account of other factors such as US trade policy – including the additional tax receipts from tariffs and the potential effect that those higher taxes will have on the US economy – or many other policies of the US administration. We will need to wait for the CBO’s next full economic and fiscal projections later in the year to understand more about what that might mean.

Either way, the OBBBA will go down as one of the most consequential legislative acts of the US Congress in recent years.

Despite borrowing to fund the deficit in the first three months of the financial year of £58bn being in line with expectations, it was still the third-highest first quarter result on record.

The monthly public sector finances release for June 2025 published by the Office for National Statistics (ONS) on 22 July reported a provisional deficit of £21bn for the month of June and £58bn for the three months then ended. This is £4bn more and in line with budget respectively, and £7bn and £8bn more in each case than the first fiscal quarter a year ago.

Alison Ring OBE FCA CPFA, ICAEW Director of Public Sector and Taxation, says: “Even if borrowing to fund the deficit in the month of June was only a little higher than expected and was in line with expectations in the first three months of the financial year, the first quarter was still the third highest since monthly records began. This trajectory will not have lightened the Chancellor’s mood as she decides which taxes to put up in the Autumn Budget later this year.

“The government has two big problems with the public finances: the short-term outlook – which is bad – and their long-term prospects – which are worse. Public spending continues to outpace tax receipts by a significant margin, while the OBR has reiterated its conclusion that the public finances are unsustainable over the next 25 to 50 years if this and future governments continue on the current path.

“Unfortunately, the major challenges facing the public finances over the next quarter of a century and beyond means that this will not be the last time a chancellor of the exchequer needs to come back asking for more. Now is the time to stop kicking the can down the road and develop a comprehensive long-term fiscal strategy to put the public finances onto a sustainable path.”

Month of June 2025

The fiscal deficit for June 2025 was £21bn, £4bn more than budgeted and £7bn more than a year previously. According to the ONS, this was the second-highest June deficit since monthly records began in 1993, with only June 2020 during the pandemic being higher.

First quarter to June 2025

The deficit for the first three months of the 2025/26 financial year was £58bn, £8bn more than a year previously. Despite being in line with budget, this is the third-highest first quarter deficit since monthly records began (after the first quarter deficits in 2020/21 and 2021/22).

Table 1 highlights how total receipts and total current spending in the three months to June 2025 of £278bn and £323bn were up 7% and 8% respectively, compared with the same period last year.

Receipts were boosted by the employer national insurance increase from April 2025 onwards in addition to the effect of fiscal drag on income tax caused by the continued freeze in personal tax allowances. Meanwhile, the increase in current spending over the past year was primarily as a consequence of public sector pay rises, higher supplier costs and rises in welfare benefits.

The increase in debt interest of £5bn to £42bn consisted of a £6bn increase in indexation on inflation-linked debt as inflation returned less a £1bn reduction in interest on variable and fixed-interest debt. The latter was primarily the effect of a lower Bank of England base rate offsetting a higher level of debt compared with a year ago.

Net investment of £13bn in the first quarter of 2025/26 was £1bn or 8% higher than the same period last year. Capital expenditure of £22bn was up by £1bn and capital transfers (capital grants, research and development funding, and student loan write-offs) of £9bn were up by £1bn, less depreciation of £18bn up by £1bn.

Table 1: Summary receipts and spending

3 months to June

2025/26 £bn

2024/25 £bn

Change %

Income tax

64

60

+7%

VAT

52

50

+4%

National insurance

48

41

+17%

Corporation tax

26

24

+8%

Other taxes

57

56

+2%

Other receipts

31

30

+3%

Current receipts

278

261

+7%

Public services

(178)

(165)

+8%

Welfare

(77)

(72)

+7%

Subsidies

(8)

(8)

–

Debt interest

(42)

(37)

+14%

Depreciation

(18)

(17)

+6%

Current spending

(323)

(299)

+8%

Current deficit

(45)

(38)

+18%

Net investment

(13)

(12)

+8%

Deficit

(58)

(50)

+16%

Borrowing and debt

Table 2 summarises how the government borrowed £64bn in the first quarter to take public sector net debt to £2,874bn on 30 June 2025. The movements comprised £58bn in public sector net borrowing (PSNB) to fund the deficit and £6bn to fund government lending activities and working capital movements.

The table also illustrates how the debt to GDP ratio increased from 95.2% of GDP at the start of the financial year to 96.3% on 30 June 2025, with the incremental borrowing partly offset by the ‘inflating away’ effect of inflation and economic growth adding to GDP, the denominator in the net debt to GDP ratio.

Table 2: Public sector net debt and net debt/GDP

3 months to June

2025/26 £bn

2024/25 £bn

PSNB

58

50

Other borrowing

6

(3)

Net change

64

47

Opening net debt

2,810

2,686

Closing net debt

2,874

2,733

PSNB/GDP

2.0%

1.8%

Other/GDP

0.2%

(0.1%)

Inflating away

(1.1%)

(1.5%)

Net change

1.1%

0.2%

Opening net debt/GDP

95.2%

95.6%

Closing net debt/GDP

96.3%

95.8%

Public sector net debt on 30 June 2025 of £2,874bn comprised gross debt of £3,286bn less cash and other liquid financial assets of £412bn.

Public sector net financial liabilities were £2,504bn, comprising net debt of £2,874bn plus other financial liabilities of £706bn less illiquid financial assets of £1,076bn. Public sector negative net worth was £878bn, being net financial liabilities of £2,504bn less non-financial assets of £1,626bn.

Revisions

Caution is needed with respect to the numbers published by the ONS, which are repeatedly revised as estimates are refined and gaps in the underlying data are filled. This includes local government where the numbers are only updated in arrears and are based on budget or high-level estimates in the absence of monthly data collection.

The latest release saw the ONS revise the previously reported deficit for the two months to May 2025 down by £1bn and revise public sector net debt on 31 May 2025 up by £7bn.