January’s public sector finance surplus of £2.9bn was driven by a boost to tax revenues as inflation drove up VAT receipts and self assessment income grew, putting further pressure on Chancellor Rishi Sunak to increase support to households facing huge rises in energy prices.

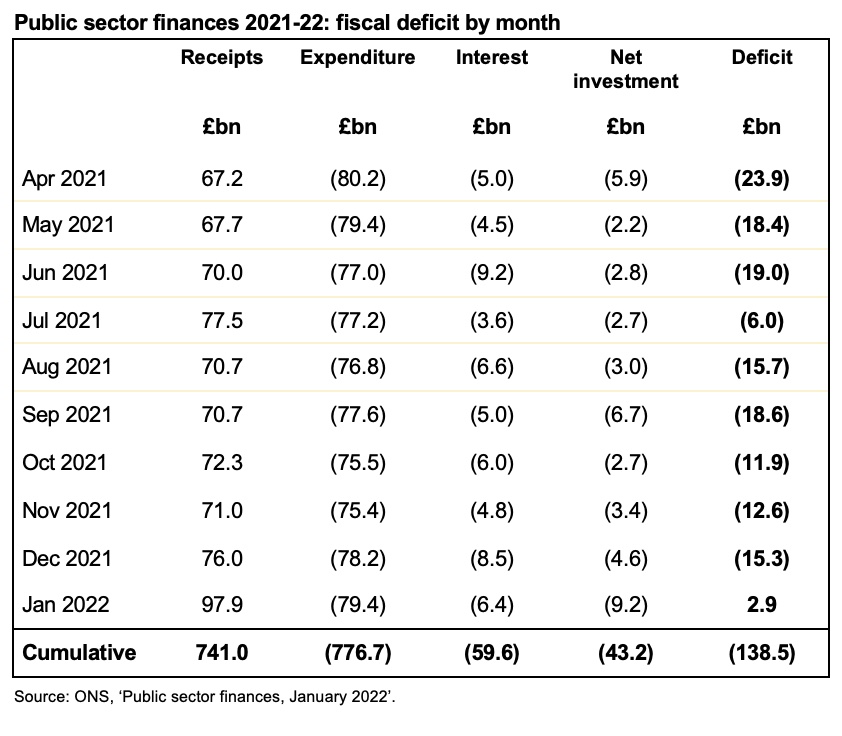

The public sector finances for January, released on 22 February, reported a surplus for the month of £2.9bn. This was an improvement of £5.4bn from the deficit of £2.5bn reported for January 2021, but £7bn smaller than the £9.9bn surplus reported for January 2020.

Total receipts were £97.9bn in January, up from £76.0bn in the previous month.

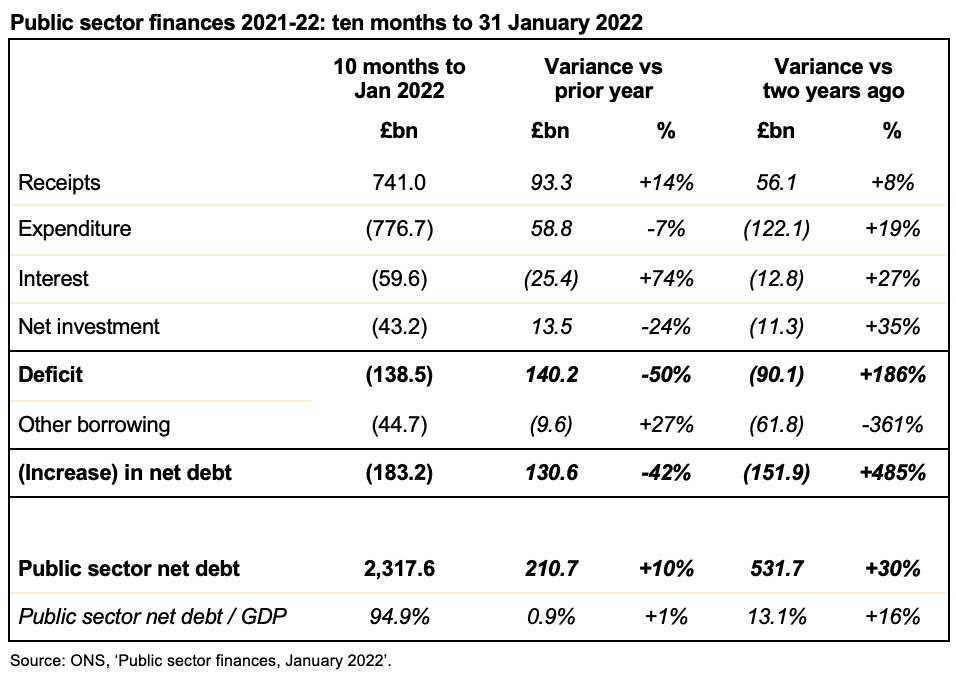

Public sector net debt fell from £2,339.7bn at the end of December to £2,317.6bn or 95% of GDP at the end of January, with tax and loan recoveries supplementing the surplus for the month. Despite that, debt is £210.7bn higher than at the start of the financial year and £524.5bn higher than in March 2020.

The cumulative deficit for the first 10 months of the financial year was £138.5bn, compared with £278.7bn and £48.4bn for the same period last year and the year before that respectively.

This was £17.7bn below the forecast published by the Office for Budget Responsibility (OBR) alongside last October’s Autumn Budget and Spending Review 2021, although higher than forecast tax receipts were partially offset by higher than forecast interest charges on index-linked debt. Both are driven by higher rates of inflation, which takes more time to feed through to non-interest expenditure.

Cumulative receipts in the first 10 months of the 2021/22 financial year amounted to £741bn, £93.3bn or 14% higher than a year previously, but only £56.1bn or 8% above the level seen in the first 10 months of 2019/20. At the same time, cumulative expenditure excluding interest of £776.7bn was £58.8bn or 7% lower than the same period last year, but £122.2bn or 19% higher than two years ago.

Interest amounted to £59.6bn in the 10 months to January 2022, £25.4bn or 74% higher than the same period in 2020/21, principally because of the effect of higher inflation on index-linked gilts. Interest costs were £12.8bn or 27% more than in the equivalent 10-month period ended 31 January 2020.

Cumulative net public sector investment up to January 2022 was £43.2bn. This was £13.5bn or 24% below the £56.7bn reported for the first 10 months of last year, which included around £17bn of COVID-19-related lending that the government does not expect to recover. Investment was £11.3bn or 35% more than two years ago, principally reflecting greater capital expenditures, including on HS2.

The increase in debt of £183.2bn since the start of the financial year comprises the cumulative deficit of £138.5bn and £44.7bn in other borrowing. The latter has been used to fund lending to banks through the Bank of England’s Term Funding Scheme, lending to businesses via the British Business Bank (including bounce-back and other coronavirus loans), student loans, and other cash requirements, net of the recovery of taxes deferred last year and loan repayments.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “The strong tax receipts reported today will provide a welcome respite for the public finances, reducing the shortfall in the government’s income compared with its expenditure from previous forecasts. However, the deficit is still on track to be the third highest ever recorded in peacetime, while public debt is more than half a trillion pounds higher than it was at the start of the pandemic.

“The challenge for Sunak will be balancing the strong pressures on him to increase the support package for households facing rapidly rising energy costs and retail prices, with the need to strengthen the resilience of the public finances in the face of a great deal of economic uncertainty and increasing global security concerns. The Chancellor will be acutely aware that while inflation is adding to tax revenues today it will go on to add to public spending tomorrow”.

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The ONS made a number of revisions to prior month and prior year fiscal numbers to reflect revisions to estimates. These had the effect of decreasing the reported fiscal deficit for the nine months to December 2021 from £146.8bn to £141.4bn and increasing the deficit for the year ended 31 March 2021 from £321.8bn to £321.9bn.