Our chart this week takes a look at the effect of the Spring Budget 2024 on the public finances.

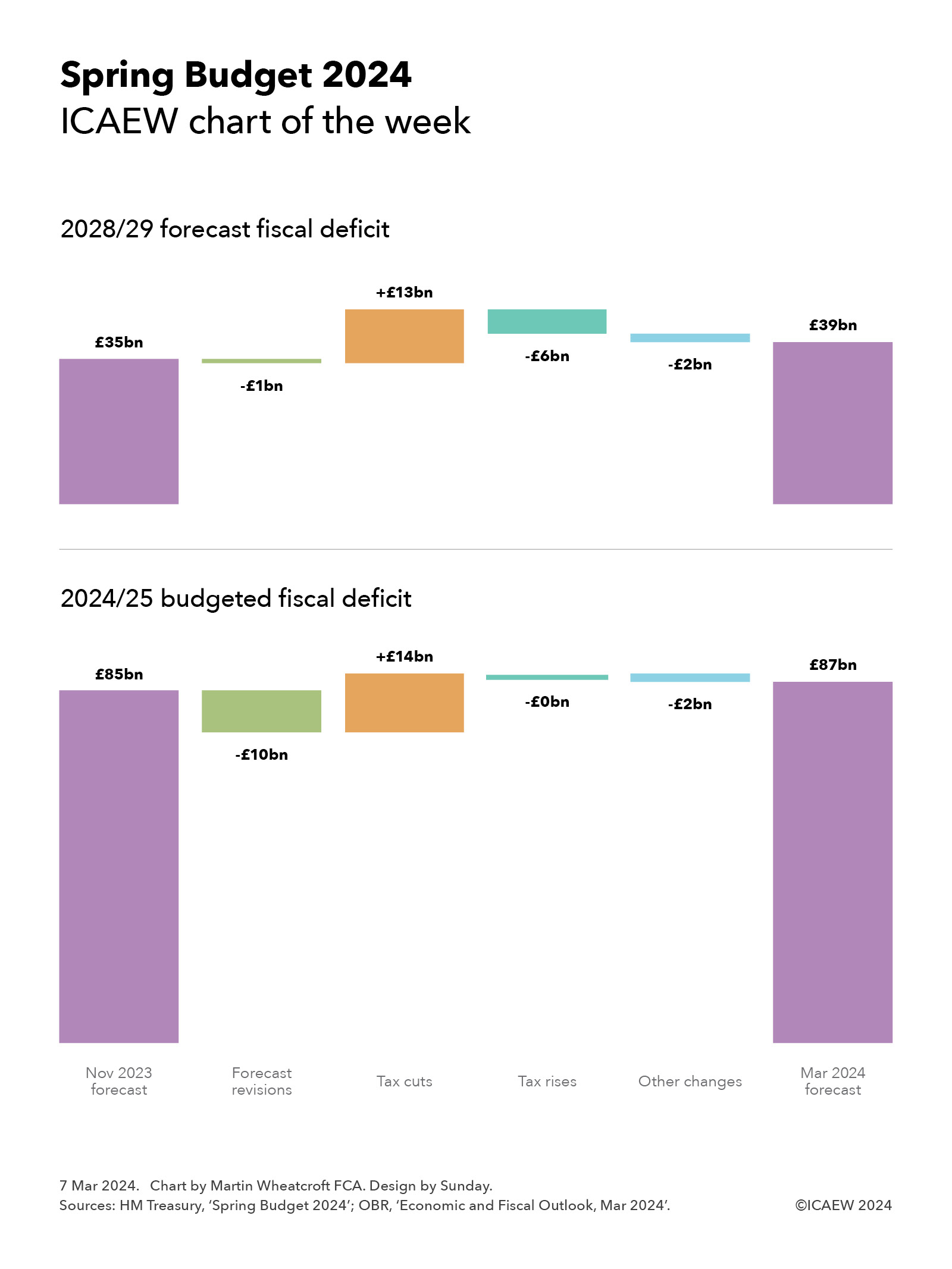

This week’s chart summarises the changes announced in the Spring Budget 2024, analysing the changes in the budgeted fiscal deficit for 2024/25 and the forecast fiscal deficit for 2028/29 since the forecasts that accompanied the Autumn Statement 2023 last November.

As the chart illustrates, the budgeted deficit for 2024/25 of £85bn anticipated in November has been revised up to £87bn, comprising forecast revisions reducing the deficit of £10bn, followed by tax cuts of £14bn increasing the deficit, offset by tax rises of close to zero and other changes of £2bn reducing the deficit.

The chart also shows the changes to the final year of the forecast period, with the forecast of deficit £35bn at the time of the Autumn Statement 2023 reduced by £1bn from forecast revisions, increased by £13bn to fund tax cuts, reduced by £6bn from tax rises and £2bn from other changes to reach a new forecast for the deficit in 2028/29 of £39bn.

The good news for the Chancellor was the improvement in the public finances in the earlier years of the forecast, with interest rate expectations coming down from last year. This resulted in an improvement in the forecasts of £16bn in 2024/25 and £14bn in 2028/29, offset by the effect of lower inflation expectations on tax and other receipts of £2bn and £13bn respectively to result in net forecast revisions of £10bn and £1bn respectively. The lower inflation assumption has a bigger impact over time as there is a compounding effect on tax and other receipts.

This allowed the Chancellor to announce a two-percentage point cut in national insurance pushing up the deficit by £10bn in 2024/25 and £11bn in 2028/29, together with freezes in fuel and alcohol duties, changes in the high-income child benefit charge, an increase in the VAT threshold from £85,000 to £90,000, and a four-percentage point cut in capital gains tax on property sales from 28% to 24%. The latter change is expected to increase tax receipts by a few hundred million pounds a year as it is expected to encourage more property sales, with higher volumes offsetting lower tax on each sale. Overall, these other tax cuts push up the deficit by £4bn in 2024/25 and £2bn in 2028/29.

The forecast revisions weren’t enough to allow the Chancellor to cover the cost of cutting taxes, and so he also announced some tax rises. These include the introduction of a duty on vaping and an increase in tobacco duty, an extension of the energy profits levy to March 2029, and changes in the tax treatment of ‘non-doms’. These have a relatively small effect in 2024/25 but build up to a reduction in the deficit around £6bn a year by 2028/29.

Other changes of £2bn in 2024/25 comprised £1bn in other policy measures and £1bn in indirect benefits to the economy from the Chancellor’s announcements in 2024/25, while the £2bn in 2028/29 reflected £1bn from improvements in tax collection, £1bn in other measures, and £2bn from indirect benefits to the economy, offset by £1bn from interest on increased borrowing, and £1bn to be invested in public sector productivity.

In summary, these are relatively tiny changes in the outlook for the public finance in the context of £1.2trn of public spending each year and public sector net debt that is still on track to exceed £3.0trn by the end of the forecast period in March 2029.

Even relatively small changes in economic assumptions, in spending plans, or in tax policies could have a significant impact on the fiscal forecasts, especially those for 2028/29.

For more information about the Spring Budget 2024 and ICAEW’s letters to the Chancellor and HM Treasury, click here.