Better than expected self assessment tax receipts helped generate a small fiscal surplus of £5bn in January, reducing the year-to-date deficit to £117bn, £7bn more than the comparative period in the previous financial year.

The monthly public sector finances for January 2023 released on Tuesday 21 February 2023 reported a provisional surplus for the month of £5bn. This was a significant improvement over the deficit of £26bn reported for the previous month (December 2022), but £7bn less than the surplus reported for the same month last year (January 2022).

A surplus arose primarily because better than expected self assessment tax receipts were sufficient to offset the effect of higher interest costs, higher inflation on index-linked debt, and the cost of the energy price guarantee for households and businesses incurred during the month. January also saw the Office for National Statistics (ONS) record a £2bn charge for custom duties that the UK had failed to collect when it was a member of the EU Customs Union.

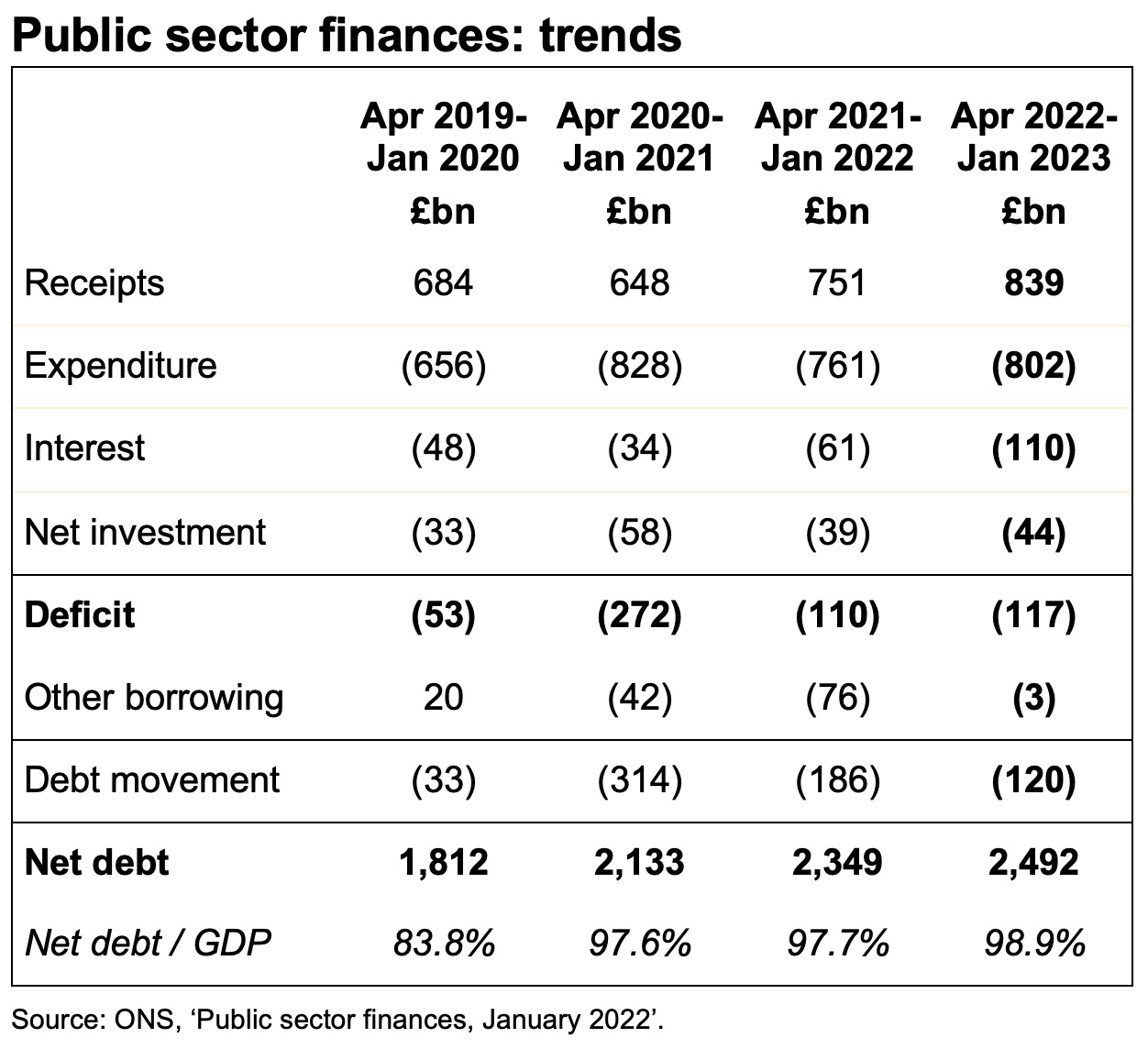

The cumulative deficit for the first 10 months of the financial year was £117bn, which is £7bn more than in the same period last year but £155bn lower than in 2020/21 during the first stages of the pandemic. It was £64bn more than the deficit of £53bn reported for the first 10 months of 2019/20, the most recent pre-pandemic pre-cost-of-living-crisis comparative period.

The deficit was £22bn below the Office for Budget Responsibility (OBR)’s revised forecast made at the time of the Autumn Statement in November, primarily because the energy price guarantee has cost less than anticipated.

Public sector net debt was £2,492bn or 98.9% of GDP at the end of January 2023, dipping below the £2.5tn reported last month because of corrections to prior month data. This is £672bn higher than net debt of £1,820bn at 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic. The OBR’s latest forecast is for net debt to reach £2,571bn by March 2023 and to approach £3trn by March 2028.

Tax and other receipts in the 10 months to 31 January 2023 amounted to £839bn, £88bn or 12% higher than a year previously. Higher income tax and national insurance receipts were driven by rising wages and the higher rate of national insurance for part of the year, while VAT receipts benefited from inflation in retail prices.

Expenditure excluding interest and investment for the ten months of £802bn was £41bn or 5% higher than the same period in 2021/22, with Spending Review planned increases in spending, the effect of inflation, and the cost of energy support schemes partially offset by the furlough programmes and other pandemic spending in the comparative period not being repeated this year.

Interest charges of £110bn for the 10 months were £49bn or 80% higher than the £61bn reported for the equivalent period in 2021/22, through a combination of higher interest rates and higher inflation driving up the cost of RPI-linked debt.

Cumulative net public sector investment to January was £44bn, £5bn more than a year previously. This is much less than might be expected given the Spending Review 2021 pencilled in significant increases in capital expenditure budgets in the current year.

The increase in net debt of £120bn since the start of the financial year comprised borrowing to fund the deficit for the 10 months of £117bn together with a further £3bn to fund student loans, lending to businesses and others, and working capital requirements, net of cash inflows from repayments of deferred taxes and loans made to businesses during the pandemic.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “With a small surplus, January’s fiscal numbers benefited from stronger self-assessment tax receipts than expected, providing some comfort to Chancellor Jeremy Hunt as he assembles his first Budget. The deficit for the current financial year is still on track to be one of the highest ever recorded, reaching £117bn for the ten months to January 2023 after energy support and interest costs more than offset the benefit of higher tax receipts.

“Although it appears that inflation has peaked, the near-term economic outlook continues to deteriorate and so calls for immediate tax cuts are likely to remain unanswered. We are asking the Chancellor to take urgent action to eliminate the backlog at HMRC that is inhibiting business growth, and to make improving the resilience of the UK economy and the public finances a priority.”

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The ONS made several revisions to prior period fiscal numbers to reflect revisions to estimates. These had the effect of reducing the reported fiscal deficit for the nine months ended 31 December 2022 by £6bn to £122bn and reducing the reported fiscal deficit for the year to 31 March 2022 by £1bn to £122bn.

For further information, read the public sector finances release for January 2023.