My chart this week is on Germany, where a new ‘traffic light’ coalition government headed by Chancellor-designate Olaf Scholtz is poised to take charge of Europe’s most prosperous nation.

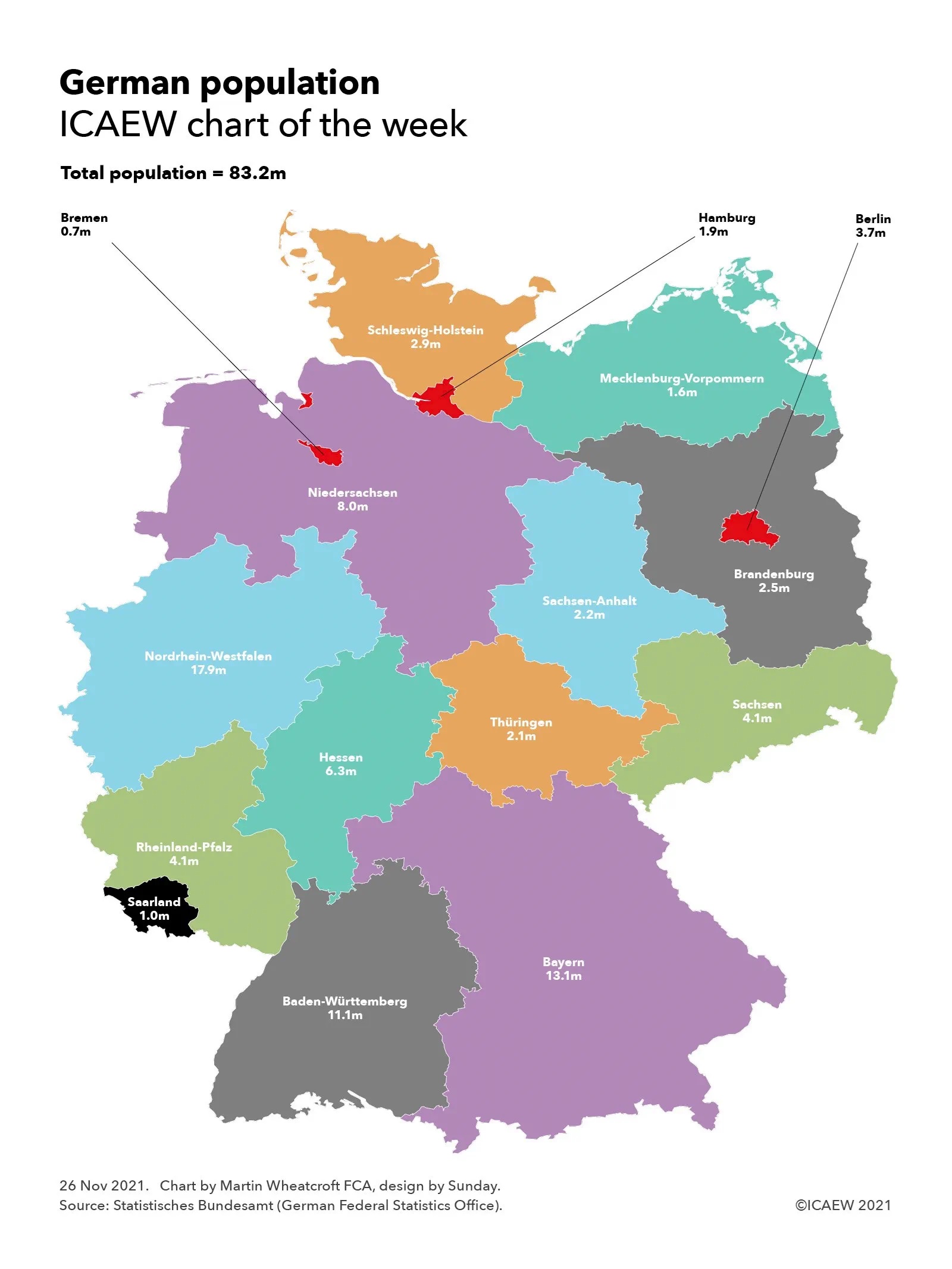

With a population of 83.2m and a €3.4tn (£2.9tn) economy, Germany is the largest member of the European Union and the fourth biggest national economy in the world after the USA, China and Japan.

The formal agreement of a red-green-yellow ‘traffic light’ coalition between the centre-left Social Democratic Party (SPD), the Green Party and the liberal Free Democratic Party (FDP) means that Angela Merkel can finally retire as Chancellor to be replaced by SPD-leader Olaf Scholz, the current Vice-Chancellor and Finance Minister in the outgoing ‘Grand Coalition’.

According to the coalition agreement, which is still subject to ratification by the three parties, Olaf Scholtz will become the new Chancellor with the SPD filling six of the 15 federal ministries, the Green party filling five ministries and the FDP filling four. Green co-leaders Annalena Baerbock and Robert Habeck are expected to become Foreign Minister and Economy & Climate Change Minister respectively, while FDP leader Christian Lindner is expected to become Finance Minister.

Despite running the most powerful country in Europe, the new coalition is only responsible for the federal government. As the chart illustrates, Germany has sixteen Bundesländer or federal states, comprising Nordrhein-Westfalen (North Rhine Westphalia) with 17.9m people, Bayern (Bavaria) with 13.1m, Baden-Württemberg with 11.1m, Niedersachsen (Lower Saxony) with 8.0m, Hessen with 6.3m, Rheinland-Pfalz (Rhineland Palatinate) and Sachsen (Saxony) each with 4.1m, the city-state of Berlin with 3.7m, Schleswig-Holstein with 2.9m, Brandenburg with 2.5m, Sachsen-Anhalt (Saxony-Anhalt) with 2.2m, Thüringen with 2.1m, the city-state of Hamburg with 1.9m, Mecklenburg-Vorpommern with 1.6m, Saarland with 1.0m and the city-state of Bremen with 0.7m.

The state governments are also run by coalitions. The now federal opposition Union parties (the Christian Democratic Union and the Bavarian Christian Social Union) lead two- or three-party coalitions in seven states, the SPD lead in seven states, the Greens in one state and Der Linke (the Left) in one state. With a proportional voting system at state and federal levels, coalition government is a way of life in Germany, with parties that are in government in one state being in opposition to each other in others.

Despite being the first three-party coalition at a federal level, with the more complicated negotiations that entails, the coalition agreement has been reached fairly ‘speedily’ by German standards – taking just over two months compared with the six months taken to agree the ‘Grand Coalition’ between the Union parties and the SPD following the last election in September 2017.

The inclusion of the Greens puts climate change at the top of the new government’s priorities, bringing forward the end of coal from 2038 to 2030 for example, while the inclusion of the fiscally prudent FDP will mean limited scope for new government borrowing. Other plans include raising the minimum wage, more defence spending, and legalising cannabis,

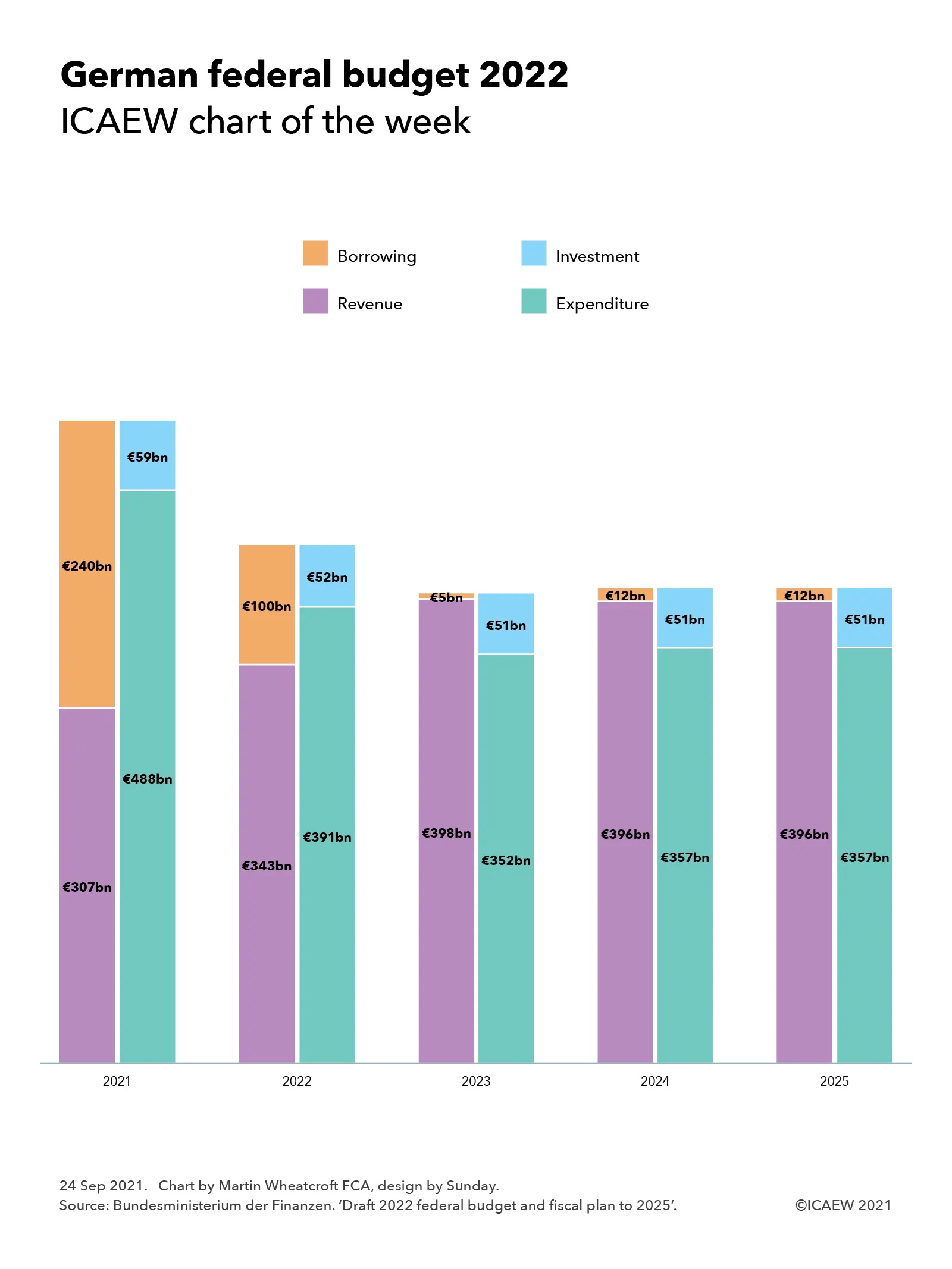

To read about the federal budget see my previous ICAEW chart of the week: German federal budget 2022.