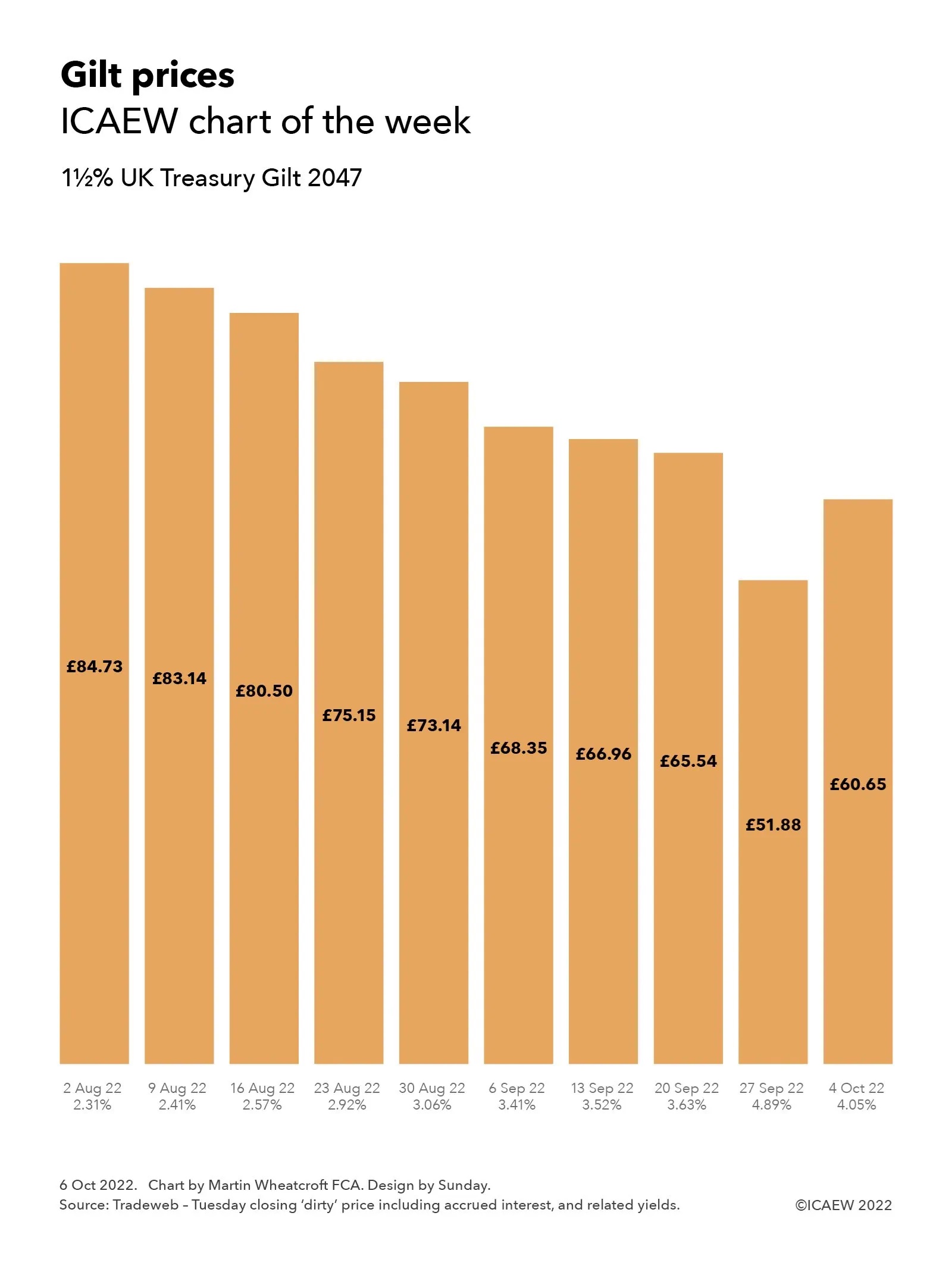

Our chart this week looks at how the price of the 1½% UK Treasury Gilt 2047 has changed over a nine-week period, falling from £84.73 for a £100 gilt on 2 August to £51.88 on 27 September, before recovering to £60.65 on 4 October.

Recent events in the government bond markets have been featuring on the front pages since the mini-Budget. As our chart illustrates, gilt prices – that had already been falling as interest rates increased – dived to their lowest level for many years following the Chancellor’s announcement of unfunded tax cuts at the same time as an unprecedented intervention in energy markets.

The chart is based on the Tuesday closing price of a long-dated gilt, the 1½% UK Treasury Gilt 2047 (GB00BDCHBW80), which is due to mature on 22 July 2047. Originally a 30-year gilt issued in 2016, 2017 and 2018 at a weighted average price of £93.90 and a weighted average accepted yield of 1.8%, there are around 249m £100 gilts with a total nominal value of £24.9bn traded on the London Stock Exchange.

Debt investors that purchased at that price would have made a tidy profit if they had sold when the price peaked at £125.41 on 9 March 2020 (when the yield was 0.51%) but the price has fallen over the last couple of years as interest rates have risen, dropping to £84.73 at the close of business on Tuesday 2 August, providing a yield of 2.31% to a debt investor intending to hold this gilt over the remaining 25 years until it matures.

Worsening inflation expectations since then have caused the yields demanded by investors to rise, resulting in the price falling by 14% over a four-week period to £83.14 on 9 August, £80.50 on 16 August, £75.15 on 23 August and £73.14 on 30 August, as the yield rose to 2.41%, 2.57%, 2.92% and 3.06% respectively. The slide continued in September as the price fell by a further 10% to £68.35 on 6 September, £66.96 on 13 September and £65.54 on 20 September as the yield rose to 3.41%, 3.52% and 3.63%, bring the cumulative fall since the first Tuesday in August to 23%.

The price plunged to £51.88 in the wake of the mini-Budget, causing the yield to spike to 4.89%, a 21% fall in one week that brought the cumulative fall over eight weeks to 39%. The Bank of England’s intervention managed to stabilise the gilt market, with the price increasing by 17% to £60.65 over the week to Tuesday 4 October. This has brought the yield back down to 4.05% and reduces the cumulative fall in price over nine weeks between 2 August and 4 October to 28%.

The turmoil in the gilt markets has shone a light on the risks associated with investing in what is often described as a ‘very safe’ investment in gilt-edged government securities issued by one of the world’s largest economies. While the creditworthiness of the British government remains unquestioned, recent events have demonstrated just how quickly debt markets can move in response to changing economic conditions and prospects.

Whether you are invested in bonds directly, or indirectly through your pension, recent events have confirmed, in an all-too-dramatic way, the truism that stock prices can – and do – go down as well as up.