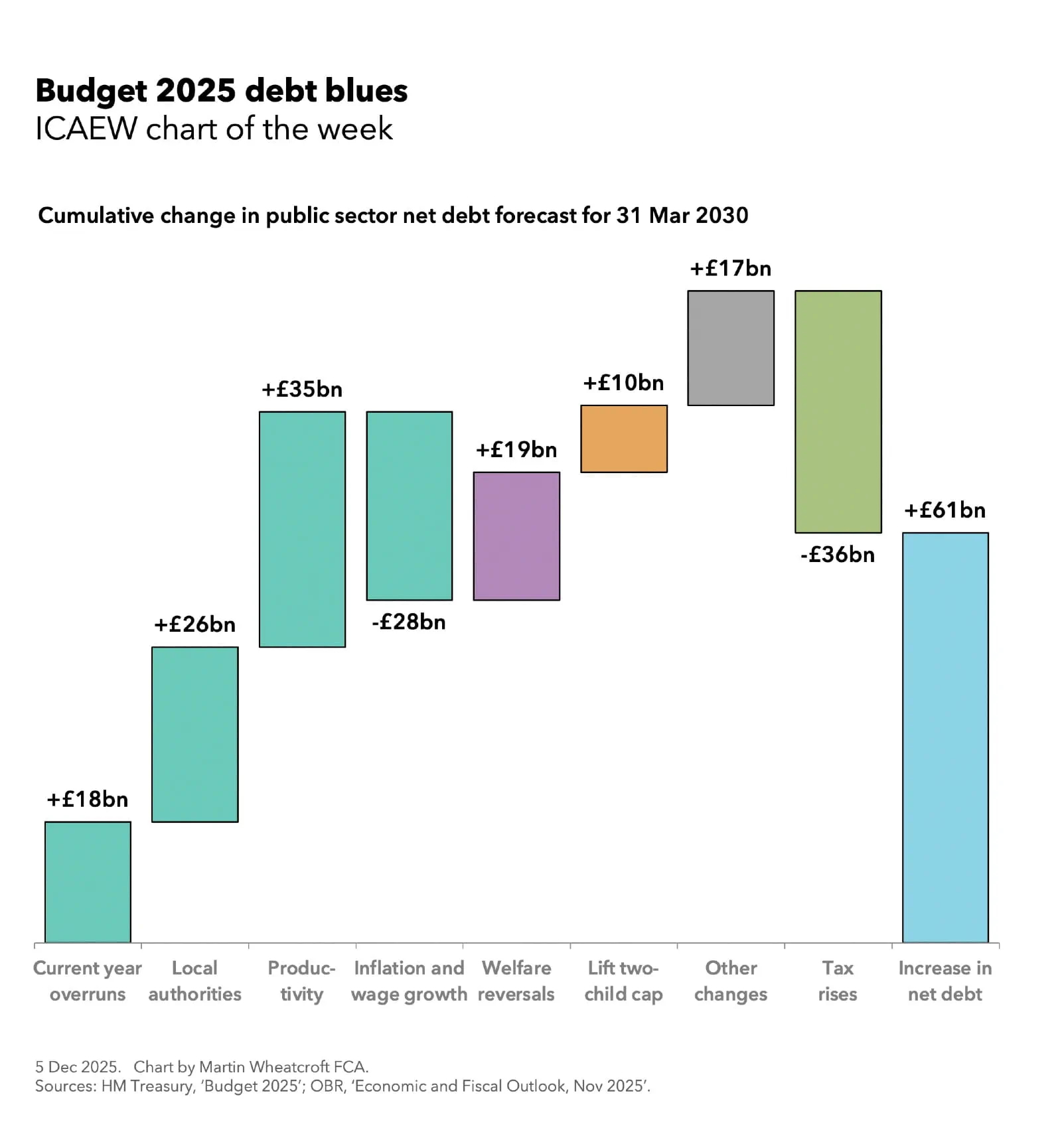

My chart for ICAEW this week illustrates how despite being a “tax-raising Budget”, the cumulative net effect of all the changes announced last week is to add £61bn to the public sector net debt forecast for 31 March 2030.

While my chart for ICAEW last week looked at the impact of Budget 2025 on 2029/30, the fourth year of the fiscal forecast used for the Chancellor’s fiscal rules, this week’s focus is on the cumulative effect of the changes made between now and 31 March 2030.

The first four bars of our step chart analyse the OBR’s forecast revisions, starting with extra borrowing to fund the expected budget overrun in the current financial year (2025/26) of £18bn (technically a £21bn higher deficit less a £3bn opening adjustment). This is followed by more borrowing to fund higher local authority spending of £26bn over four years (an average of £6.5bn a year) and to cover cumulative lower receipts of £35bn from downgrading the productivity growth assumption (£2bn a year rising to £16bn by 2029/30). This is then offset by £28bn over four years from the impact of inflation and wage growth on receipts exceeding the impact of inflation and other cost pressures on public spending.

Borrowing over the next four years is then increased by £19bn (just under £5bn a year on average) to cover the government’s welfare reversals over the summer – the restoration of the winter fuel allowance to many pensioners and the decision not to proceed with eligibility restrictions for disability benefits that were needed to make the Spring Statement add up.

The decision to lift the two-child benefit cap adds another £10bn (£2.5bn a year on average) to projected debt over the next four years, while other policy measures and working capital movements are expected to add £17bn (£11bn and £6bn respectively) on top of that.

A £36bn net reduction in debt from higher tax receipts net of indirect effects over the next four years (zero in 2026/27, £4bn in 2027/28, £10bn in 2028/29, and £22bn in 2029/30) reduces the cumulative impact to £61bn, with the £3,391bn forecast for 31 March 2030 at the time of the Spring Statement back in March 2025 being revised up to £3,452bn in the Autumn Budget 2025.

Perhaps the most surprising aspect of this analysis is the £26bn revision to the forecast for local government spending. While not as large as the well-publicised impact of productivity downgrades on the OBR’s fiscal forecast, it highlights some fundamental bookkeeping issues in how the government manages the public finances. A monthly financial consolidation process that excludes local government, schools and many other public bodies means the Office for National Statistics (ONS) and HM Treasury rely on forecasts and estimates instead of actual data when reporting the monthly public sector finances, exacerbated by the use of the four different accounting frameworks across the public sector and the local audit crisis in England that has created a large backlog in local authority audited financial statements.

The OBR states: “Recent substantial revisions to LA borrowing estimates and outturns, which reflect ongoing challenges in obtaining timely and high-quality estimates particularly for expenditure by local authorities. The ONS, the Ministry of Housing, Communities and Local Government, the Treasury and the OBR have formed a joint Local Government Financial Information Taskforce to investigate and address these concerns, with the overall objective of improving the flow of data to the ONS and the accuracy of our forecast.”

Meanwhile, the backloading of tax rises means that although the forecast is for a current budget surplus in 2029/30 and for a reduced overall deficit in that year, the summer welfare reversals, lifting of the two-child benefit cap, and other policy changes all require more borrowing before the tax rises kick in.

The 2025 Budget provides very mixed messages about the UK public finances’ prospects. There is more borrowing over the next three years before tax rises fully kick-in, while at the same time there are significant risks that mean the government could be back here again next year or the year after to ask for more money.

If ever a Chancellor could really do with some good economic news, it is probably in the coming year.

My chart this week for ICAEW looks at how the Chancellor used tax rises to refill and increase her budget headroom after forecast revisions and spending increases eliminated the projected current budget surplus for 2029/30.

The chart shows how the projected current budget surplus of £10bn in 2029/30 was reduced by £6bn of Office for Budget Responsibility (OBR) forecast revisions, by £5bn of spending increases announced in the Autumn Budget, and by £1bn from the freezing of fuel duties for yet another year.

Together these reduced the Chancellor’s headroom against her primary fiscal rule (to be in a current budget surplus by the fourth year of the fiscal forecast) from £10bn to minus £2bn – in effect breaching her fiscal rule before taking account of tax rises.

The Chancellor has then restored – and increased – her fiscal headroom to £22bn through a long list of tax rises that are anticipated to generate £24bn more in receipts in 2029/30.

Forecast revisions

The rumoured forecast downgrade from the OBR of £6bn in 2029/30 turned out to be much less significant than expected.

The OBR cut its receipts forecast for 2029/30 by £16bn a year because of weaker assumed productivity growth. But this was more than offset by a £30bn increase from higher nominal wages and prices, driven by both inflation and real wage growth, to add £14bn to receipts in that year – an increase not a decrease to the receipts side of the forecast.

This was offset by £20bn in higher current spending, of which £6bn was from higher uprating of welfare benefits and growth in claimants and caseloads, £6bn from government policy reversals on the winter fuel allowance and disability benefits, £4bn in higher debt interest, £2bn in higher local government spending, and £2bn in other changes.

The resulting deterioration of £6bn in the projected current budget surplus for 2029/30 was £14bn smaller than the £22bn deterioration anticipated by the Institute for Fiscal Studies (IFS) in its pre-Budget forecast (as used in our chart of the week on the Autumn Budget hole). The principal driver was £22bn in incremental receipts from higher inflation and higher real wage growth less £6bn in higher spending for similar reasons.

Because departmental budgets for 2026/27, 2027/28 and 2028/29 set out in the Spending Review earlier this year have not been increased for this higher level of inflation, the risk is that future Budgets will need to top up the amounts allocated to departments to deal with cost pressures that are likely to arise.

Spending increases

Current spending is projected to increase by £5bn in 2029/30, comprising £3bn to cover the annual cost of abolishing the two-child benefit cap, £1bn in higher debt interest, and £1bn in net other changes in non-interest current spending.

The OBR also announced that it had reduced its underspend assumption for departmental budgets during the latest spending review period (2026/27 to 2028/29 for current spending) by an average of £4bn a year to reflect the increased pressures on budgets from higher inflation. There was no similar adjustment to 2029/30 current spending as it is not covered by the spending review, but there is a risk that a similar adjustment may be needed by the time of the 2027 spending review.

Fuel duty freeze

Freezing fuel duties has become a consistent feature of Budgets since 2011, with the effect of reducing annual tax receipts in real terms by just under £1bn a year.

Given the current Chancellor has chosen to continue this practice in two successive Budgets, it is disappointing that fiscal forecasts have not reflected the anticipated £3bn additional reduction in tax receipts in 2029/30 if fuel duty is frozen again in the next three Budgets.

Tax rises

The Chancellor announced a total of £27bn in tax rises in the Budget (£26bn if the fuel duty freeze effective tax cut is netted off), but this is expected to generate £24bn in incremental tax receipts once behavioural responses and other indirect economic effects are adjusted for.

These tax rises are expected to generate the following amounts per year by 2029/30:

£8bn from extending the freezing of personal allowances (more ‘fiscal drag’).

£5bn from restricting the use of salary-sacrifice schemes to make pension contributions.

£2bn from increased income tax rates on property, savings and dividends.

£1.5bn from changes to writing-down allowances.

Just under £1.5bn from a mileage-based charge on electric cars.

Just over £1bn from gambling duty reform.

Just under £1bn from capital gains tax on employee ownership trusts.

Just under £0.5bn from a high value council tax surcharge.

Around £4.5bn from other tax measures.

£2bn from improved tax compliance and collection.

Higher headroom

The Chancellor chose to increase headroom against her principal (current budget) fiscal rule from £10bn last year to £22bn and to increase headroom in her secondary (debt) fiscal rule from £15bn to £24bn.

These are both positive in that they provide a much bigger cushion against potential forecast downgrades in the spring or autumn next year, reducing the risk of another round of significant tax rises in the Chancellor’s third Budget in 2026. It also helps that she is likely to gain around £15bn of extra headroom as the main fiscal rule moves to being tested in the third year of the forecast, which comes with a margin of permitted current budget deficit up to a maximum of GDP.

However, significant downside risks remain, so this outcome is far from assured. The Chancellor still faces the challenge of reviving a weak economy and delivering substantial efficiency savings if she is to keep public spending under control in the absence of more fundamental reform. That task is made harder by the risk of bailouts for local authorities and universities, and by continued pressure on the welfare budget.

The cumulative budget overrun has widened from £7bn to £10bn in seven months, reveals latest data from the Office for National Statistics.

The monthly public sector finances release, published by the Office for National Statistics (ONS) on 21 November 2025, reported a provisional shortfall between receipts and public spending of £17bn in October and a cumulative deficit of £117bn for the seven months then ended.

Martin Wheatcroft, external adviser on public finances to ICAEW, says: “The monthly public finances continue to disappoint, with the cumulative budget overrun widening from £7bn in the last release to £10bn for the seven months to October.

“While only slightly worse than expected, there were no rays of sunshine in these numbers for a beleaguered Chancellor trying to navigate her way through a series of political, economic and fiscal minefields surrounding the Autumn Budget.”

There was a £17bn shortfall between provisional receipts of £96bn and total public spending of £113bn in October 2025. This was £2bn better than the £19bn deficit incurred in October last year (£89bn receipts less £108bn total spending), but £3bn more than the budget of £14bn for the month.

Current spending of £108bn and net investment of £5bn in October were both in line with the £108bn and £5bn monthly averages incurred respectively during the first six months of the financial year.

October’s semi-annual advance tax payments meant that public sector net debt fell by £12bn during the month (from £2,917bn on 30 September to £2,905bn on 31 October 2025), with a net inflow of £29bn from working capital movements and lending activities more than offsetting the £17bn absorbed by the deficit.

The provisional £117bn deficit for the seven months to October 2025 was £9bn or 8% more than in the same seven months last year, and £10bn more than the £107bn that was budgeted. The £10bn overrun can be analysed as a £15bn adverse variance on the current budget deficit, offset by a £5bn underspend on net investment.

Table 1 highlights how year-to-date receipts of £672bn were 7% higher than the same period last year, with income tax up 8% from a combination of inflation and fiscal drag from frozen tax allowances. National insurance was up 19% as a result of the increase in employer national insurance from April 2025 onwards, and VAT receipts were up 4%, broadly in line with consumer price inflation.

Compared to last year, the 8% increase in spending to £756bn in the first seven months to October 2025 has principally been driven by public sector pay rises, higher supplier costs, the uprating of welfare benefits and higher debt interest.

Debt interest of £88bn was £9bn higher than for the first seven months of 2024/25, comprising a £7bn increase in indexation on inflation-linked debt as inflation rose again in 2025 and a £2bn increase in interest on variable and fixed-interest debt. The latter reflects a higher level of debt compared with a year ago, offset by a lower Bank of England base rate.

Net investment of £33bn in the first seven months of 2025/26 was £2bn or 6% higher than the same period last year. This comprised capital expenditure of £55bn (up by £2bn or 4%) and capital transfers (capital grants, research and development funding and student loan write-offs) of £20bn (up £2bn or 11%), less depreciation of £42bn (up by £2bn or 5%).

The deficit is budgeted to be £118bn for the full year ending 31 March 2026, comprising £107bn in the first seven months of the year to October 2025 and £11bn in the remaining five months.

The latter comprises budgeted deficits of £9bn and £11bn in November and December 2025, a forecast surplus of £23bn in January, and deficits of £1bn and £13bn in February and March 2026.

Table 2 summarises how the government borrowed £95bn in the first seven months of the financial year to take public sector net debt to a provisional £2,905bn on 31 October 2025. This comprised £117bn in public sector net borrowing (PSNB) to fund the deficit, less a £22bn net inflow from working capital movements and government lending.

The table also illustrates how the debt to GDP ratio increased by 1.0 percentage points from 93.5% of GDP at the start of the financial year to 94.5% on 31 October 2025. Incremental borrowing of £95bn, equivalent to 3.2% of GDP, was partly offset by 2.2 percentage points from the ‘inflating away’ effect of inflation and economic growth on GDP, the denominator in the net debt to GDP ratio.

Table 2: Public sector net debt and net debt/GDP

7 months to Oct

2025/26 £bn

2024/25 £bn

PSNB

117

108

Other borrowing

(22)

10

Net change

95

98

Opening net debt

2,810

2,686

Closing net debt

2,905

2,784

PSNB/GDP

4.0%

3.8%

Other/GDP

(0.8%)

(0.4%)

Inflating away

(2.2%)

(3.1%)

Net change

1.0%

0.3%

Opening net debt/GDP

93.5%

94.4%

Closing net debt/GDP

94.5%

94.7%

Public sector net debt on 31 October 2025 of £2,905bn comprised gross debt of £3,352bn, less cash and other liquid financial assets of £447bn.

Public sector net financial liabilities were £2,583bn, which included public sector net debt plus other financial liabilities of £715bn, less illiquid financial assets of £1,037bn. Public sector negative net worth was £926bn, comprising net financial liabilities less non-financial assets of £1,657bn.

Caution is needed with respect to the numbers published by the ONS, which are repeatedly revised as estimates are refined and gaps in the underlying data are filled. This includes local government, where the numbers are only updated in arrears and are based on budget or high-level estimates in the absence of monthly data collection.

This month was no different, with the ONS revising previously reported numbers for six months to September 2025 and for previous financial years. However, on this occasion, the changes made did not affect the aggregate totals when rounded to the nearest billion pounds.

Regular updates to economic statistics resulted in an upward revision to nominal GDP and a consequential 0.2 percentage point reduction in the ratio of public sector net debt to GDP from 95.3% to 95.1% as of 30 September 2025.

The Chancellor used tax rises to start repairing the public finances but spending pressures could derail his hopes for a pre-election tax giveaway in 2023 or 2024. Wednesday’s Autumn Budget and Spending Review saw total public spending settle permanently above a trillion pounds a year, as additional spending increases more than offset the end of temporary COVID-19 interventions.

A ‘Boris Budget’ – full of fizz and capital spending announcements

Despite Rishi Sunak’s avowed commitment to a small state and low taxes, the Autumn Budget reality featured both higher taxes and higher spending, and the Spending Review focused on addressing the many pressures bearing down on public services.

The Chancellor benefited from a faster rebound in the economy due to the vaccination programme, as well as being helped by the time lag between inflation benefiting the revenue line and when it starts to feed through into public spending. Combined with the health and social care levy and other tax rises, this provided him with the budgetary capacity to increase spending on health, reverse previously announced cuts in departmental spending, and still reduce borrowing.

This led the Resolution Foundation to label this a ‘Boris Budget’, reflecting the reputedly more generous instincts of Prime Minister Boris Johnson as compared with his Chancellor.

The Office for Budget Responsibility (OBR)’s high-level analysis was that the Chancellor used around half the £50bn net benefit from forecast revisions and tax rises in 2022-23 to increase spending, with the balance reducing the deficit from £107bn to £83bn. However, the Institute for Fiscal Studies (IFS) points out that, apart from health and social care, the additional spending mostly reversed planned cuts made during the November 2020 and March 2021 Budgets that were always going to be difficult to achieve in practice.

The good news from better economic forecasts, including the OBR’s revision of its estimate of the permanent scarring effect on the economy from 3% to 2%, was offset by concerns over the impact of inflation on living standards and the impact of the ending of the temporary uplift in universal credit on those on low incomes.

Higher inflation will also put public sector budgets under pressure as higher wage settlements and supplier costs start to eat into the spending increases awarded as part of the Spending Review. Clearing backlogs built up over the course of the pandemic will absorb further amounts, while there is also a risk that construction worker shortages and rising construction costs will make it difficult to deliver on the capital programmes announced in such a flurry over the weekend before the Budget announcement.

Unemployment – the dog that didn’t bark

One of the key reasons for the better economic situation than was expected at the start of the pandemic is that unemployment has not gone up significantly. The contribution of the furlough schemes and business support has been hugely significant to this outcome, not only by supporting workers and businesses during successive lockdowns but more importantly preserving businesses and the jobs for workers to return to as pandemic restrictions have been lifted.

Unemployment may still increase following the ending of the furlough schemes in September, but any increase is likely to be significantly smaller than the potential more than doubling in unemployment rates that some had anticipated at the start of the first lockdown.

Modest tax reforms overshadowed by higher tax rates, fiscal drag and a major ‘tax’ cut

Perhaps the most radical ‘tax’ change announced in the Autumn Budget was not a formal tax at all. The reduction in the universal credit taper rate from 63% to 55% is in effect a significant tax cut on those on the lowest incomes, even if it still leaves poorer households on higher effective marginal rates than those earning over £150,000 a year. It also does not make up for the removal of the temporary £20 a week boost to universal credit that has already started to hit many of the poorest households this month.

Higher inflation benefits the public finances by increasing fiscal drag as tax allowances reduce in value in real terms, bringing more people into the scope of income tax or onto higher tax bands. This is a hidden tax increase that brings in more for the government without it needing to increase headline rates.

Of course, the government did that as well. The headline rates of employee national insurance, employer national insurance and dividend tax were increased by 1.25% in the coming year, even if in subsequent years the health and social care levy will appear on payslips and PAYE statements as a separate tax in its own right.

Modest reforms to business rates (principally more frequent revaluations), alcohol duties, and air passenger duties were relatively light touch compared with the previously announced health and social care levy and the planned 6% increase in the main corporation tax rate, even if banks saw a reduction of 5% in the bank levy on corporate profits to offset some of that increase.

More money for health and the criminal justice system, but less for the armed forces

The Spending Review saw extra money for health (funded by the new health and social care levy) where demographic pressures continue to drive demand in addition to dealing with the costs of the pandemic and the backlog of treatments that have built up.

The criminal justice system also received a substantial settlement (4.1% on average over three years), but this will not be sufficient to restore spending to the level before austerity. Indeed, the IFS has calculated that with the exception of the Department for Health & Social Care, the Home Office and the Department for Education, all other departments will continue to spend less in real terms than they did in 2009-10.

One surprise in the detail was the flat current spending settlement for the Ministry of Defence over the coming three years, implying a further cut in spending in real terms on the armed forces, which are expected to contract even further than they have done already. While equipment spending is up as part of a ‘more drones, fewer soldiers’ policy, this is one area where additional settlements in the next couple of Budgets appear more likely than not.

Higher levels of capital investment targeted at boosting regional economic growth

A big credit to the Chancellor is that despite the many challenges facing the public finances following the pandemic he has not scaled back the government’s capital investment programme. While it is the case that his two immediate predecessors pencilled in the substantial increases that we are now seeing, it is the current Chancellor who is delivering on them. There are significant boosts in investment in economic infrastructure, housing, research & development and digitising government amongst other areas.

Open questions remain in areas such as transport, where the long-awaited Integrated Rail Plan was not published with the Spending Review as expected. However, the £7bn pre-announced for regional rail upgrades demonstrates how much can be done with a bigger pot of money for investment.

The step-change in the level in capital budgets – from £70bn in 2019-20 to £107bn in 2022-23 is remarkable. The one concern will be whether the relatively flat capital budget allocations in subsequent years will mean investment starts to fall in real terms again, possibly ‘pulling the plug’ on the economic benefits of investment just as the economy recovers from the pandemic.

New fiscal rules: a cautious approach to repairing the public finances

The Chancellor announced two new fiscal rules: a current budget balance target and a declining debt to GDP ratio; although they were accompanied by subsidiary rules, including a 3% of GDP cap on investment spending and a commitment to return overseas development assistance to 0.7% of GDP once budget balance is achieved.

In effect, they provide a fiscally conservative framework of generating sufficient tax revenues to cover day-to-day spending, while allowing a certain amount of borrowing for investment. While debt should still grow – and is expected to reach over £2.5tn during the forecast period, the debt to GDP ratio should start to fall as the economy grows over time.

These changes confirm that George Osborne’s ambition to eliminate the fiscal deficit completely has been abandoned, replaced by a Gordon Brown-style current budget balance target. This is calculated under the statistics-based National Accounts fiscal framework, which for example excludes the long-term cost of public sector pensions; the government is still planning to continue to lose money on an accounting basis under IFRS.

The forward-looking current-budget balance accompanies the Chancellor’s other principal fiscal rule with is to reduce the ratio of public sector net debt to GDP, although again this uses a target based on fiscal measures that do not include other liabilities in the public sector balance sheet.

Even there, the Chancellor adopted a non-GASP (non-Generally Accepted Statistical Practice) measure to target (public sector net debt excluding the Bank of England) that excludes some central bank liabilities, which rather strangely means that money used to finance premiums paid to private investors for gilts purchased by the Bank of England is excluded from the formal fiscal targets.

Irrespective of the precise KPIs used in the fiscal rules, the overall approach is one of repairing the public finances gradually over time. Higher rates of economic growth would enable that to be accelerated, but the government has as yet been unable to identify how to get back onto the pre-financial crisis levels of productivity improvements that would be required to make this possible. In the meantime, the fiscal rules provide a framework in which tax rises to fund public spending are more likely, in particular to fund increases in the health, social care and the state pension costs driven by more people living longer.

There are many risks to the Chancellor keeping to his fiscal rules over the forecast period, especially as there is relatively little headroom within the current forecasts according to the OBR and the IFS. There are also risks from recessions over a longer period.

A weaker but more transparent public balance sheet

The pandemic has seen the liability side of the public balance sheet rise significantly, with £2.2tn rising to £2.5tn in debt adding to similar amounts of liabilities for public sector pensions and other obligations including nuclear decommissioning and clinical negligence.

Higher gearing in a balance sheet already in negative territory increases the exposure of the public finances to changes in interest rates and inflation, providing a higher risk profile for the public finances. For example, the OBR has estimated that a 1% increase in interest rates would add £25bn to interest costs each year – approaching more than twice the amount raised by the health and social care levy.

One positive aspect of the Autumn Budget and Spending Review announcement was a greater amount of balance sheet analysis, providing improved insights into how the government is managing the public balance sheet and into the risks facing the public finances. This includes much more granular detail on contingent liabilities.

Pre-election tax cuts have been promised, but will they happen?

The Chancellor was very clear in telling his backbenchers and the country that he would like to cut taxes before the next election, demonstrating his and the government’s commitment to lowering taxes.

For many commentators, this seemed a contradictory statement to make at the same time as presenting a fiscal event where the government is in the process of raising taxes to their highest level since the 1950s.

In practice, the Chancellor has some capacity to cut taxes based on the current forecasts and he will be hoping that the post-pandemic recovery is better than anticipated, enabling him to be even more generous.

However, as our recent article on the long-term pressures facing the public finances highlighted, the prospects of reversing the entirety of recent tax increases are remote. Long-term fiscal pressures continue to imply higher taxes will be needed absent much stronger economic growth than is anticipated, while there are plenty of economic storm clouds on the horizon including a potential cost-of-living crisis this winter.

More tax, more investment, more spending, less borrowing. ICAEW’s Public Sector experts examine the Spending Review and Autumn Budget 2021 announcements. The centre piece of the Spending Review and Autumn Budget 2021 was the already announced major tax and spending increase from the health and social levy, while a series of pre-announcements of (mostly) capital investment programmes obscured some relatively tough spending settlements for departmental current budgets.

As expected, the Office for Budget Responsibility revised its forecasts for economic growth upwards, reducing its estimate of the permanent scarring effect on the economy from 3% to 2%. The revised forecasts were a big contributor in reducing the forecast deficit for the 2022/23 financial year commencing in April by £24bn from £107bn to £83bn.

The reduction in the expected deficit next year was after absorbing £10bn from the effects of higher inflation on debt interest costs and an extra £27bn allocated to the Spending Review in 2022/23 over and above the £15bn provided by the health and social care levy. However, there is no supplementary pot for COVID-19 measures from April 2022 onwards, leaving departments to absorb any further costs arising from within their budget allocations.

By folding COVID-19 funding into the Spending Review for 2022/23 to 2024/25 in this way, the Chancellor was able to report real-terms increases in resource as well as capital departmental budgets. However, spending pressures remain intense and many departments are likely to need to find cuts in specific areas if they are to meet demands on public services, catch up on backlogs built up during the pandemic as well as cover the cost of what are likely to be higher public sector wage settlements than have been seen for many years.

Total departmental resource expenditure (RDEL) in the Spending Review increased from a March 2021 forecast of £393bn, £410bn and £427bn for 2022/23, 2023/24 and 2024/25 to £435bn, £443bn and £454bn respectively. The changes comprise £15bn, £12bn and £14bn from the health and social care levy announced in September 2021 and a further £27bn, £21bn and £13bn in the Spending Review. The total compares with the £385bn allocated in the current financial year excluding £70bn allocated for COVID-related spending.

Capital investment (CDEL) in the Spending Review has been set at £107bn, £111bn and £112bn in each of the three financial years ending 31 March 2023, 2024, and 2025, pretty much in line with previous announcements from earlier in the year. This still reflects a substantial increase when compared with the £99bn estimate for the current year, the £94bn for last year, and the £70bn recorded in 2019-20.

Welfare spending (outside the Spending Review) is expected to increase from £247bn in 2021-22 to £254bn next year, principally a consequence of inflation more than offsetting a £2bn saving from not continuing with the £20 universal credit uplift, and a £5bn saving from suspending the triple lock.

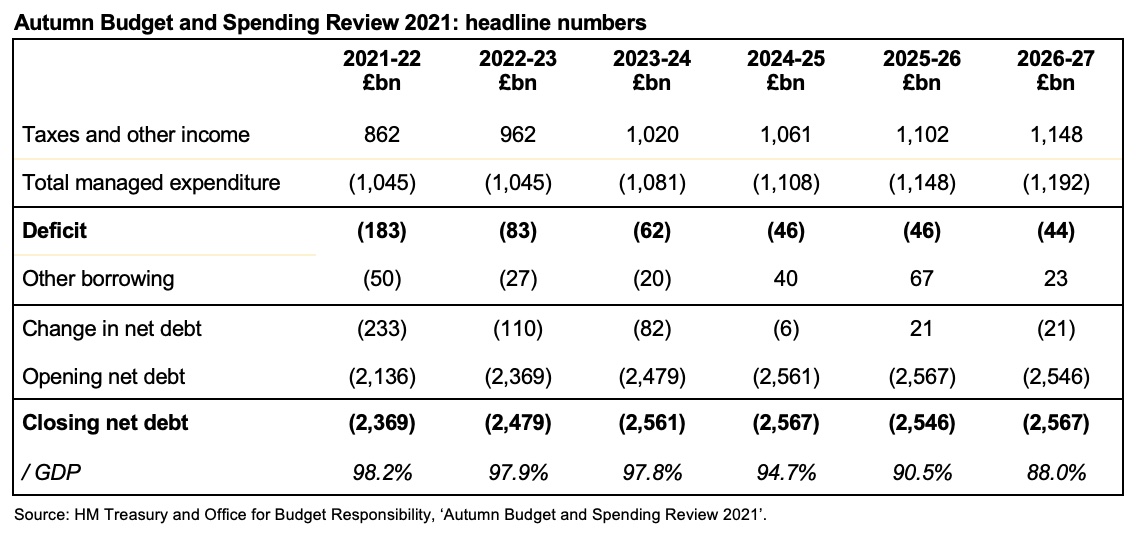

Total managed expenditure (TME) is expected to fall from £1,115bn in the last financial year to £1,045bn in both the current financial year and next year, before rising to £1,081bn in 2023/24, £1,108bn in 2024/25, £1,148bn in 2025/26 and £1,192bn in 2026/27. At the same time tax and other income is expected to increase from a pandemic-low of £795bn last year, to £862bn this year and £962bn next year, before increasing to £1,020bn, £1,061bn, £1,102bn and £1,148bn in the four following years.

The deficit is expected to fall from £320bn in 2020/21 to £183bn this year to £83bn in 2022/23, before falling to £62bn, £46bn, £46bn and £44bn in 2023-24 through 2026/27. Unlike the Chancellor’s two predecessors, the government is no longer planning to eliminate the deficit completely and instead is aiming to target a current budget surplus by 2023/24 – continuing to borrow to fund capital investment.

Public sector net debt is expected to increase from £1,793bn (84% of GDP) before the pandemic in March 2020 to £2,136bn (97%) in March 2021 to £2,369bn (98%) at the end of this financial year, before gradually rising to £2,561bn (98%) in March 2024, before stabilising in cash terms after that point but falling as a proportion of GDP to 88% by March 2027.

Despite the upbeat nature of the Budget announcement in the House of Commons, the Chancellor made some tough choices, while key announcements such as the Integrated Rail Plan and the Levelling Up White Paper were deferred into the future.

Alison Ring, Director of Public Sector and Taxation for ICAEW, commented: “The statement from the Chancellor was full of fizz, with capital investment across the country and additional funding provided for the five key Spending Review priorities of levelling up; net zero; education, jobs and skills; health; and crime and justice; partially offset by falls in COVID-19 funding.

“The tough decision to raise taxes through the health and social care levy gave the Chancellor more money to address some of the more immediate spending pressures of an ageing population, and the consequences of the pandemic. However, despite improved transparency on the government’s balance sheet, the Budget today left many questions about how he plans to get the public finances back under control over the longer-term.”