The public finances continue to be battered by economic shocks as this week’s chart on the past five years of red ink illustrates.

The monthly public sector finances for March 2023 released on Tuesday 25 April contained the first cut of the government’s financial result for 2022/23, with our chart this week illustrating trends over the past five years in receipts, expenditure and the deficit.

As our chart highlights, tax and other receipts increased from £813bn in 2018/19 to £827bn in 2019/20, before falling to £793bn during the first year of the pandemic. They recovered to £920bn in 2021/22 before rising with inflation to a provisional estimate of £1,016bn for the year ended 31 March 2023.

Total managed expenditure (TME) increased from £857bn in 2018/19 to £888bn in 2019/20, before exceeding £1trn for the first time in 2020/21 as the pandemic caused expenditure to rise significantly. TME fell in 2021/22 to £1,041bn as pandemic-released spending was scaled back, before rising this year to £1,155bn as inflation, higher interest rates and energy support packages more than offset the pandemic related spending that was not repeated in 2022/23.

The deficit of £44bn in 2018/19 was the lowest it had been since the financial crisis, following an extended period of spending restraint over a decade. The purse strings were loosened a little in 2019/20 as previous government plans to eliminate the deficit were abandoned, with the deficit rising to £61bn. The huge cost of the pandemic saw the deficit rise to £313bn in 2020/21 as the borrowing rose to meet the huge costs of dealing with the pandemic, before falling back to £121bn in 2021/22.

There were hopes that the situation would improve further, with the government in October 2021 budgeting for a deficit of £83bn. Unfortunately, rampant inflation and the energy crisis following Russia’s invasion of Ukraine mean that the government does not currently expect to reduce the deficit to below £50bn until 2027/28 at the earliest. And that is with what some commentators believe are unrealistic assumptions about the government’s ability to reduce spending on public services beyond the cuts already delivered.

Provisional receipts in 2022/23 were 25% higher than the outturn for 2018/19, which in the absence of economic growth has principally been driven by inflation of around 15% over that period combined with an increase in the level of taxation and other receipts from around 37% to approaching 41% of the economy. Total managed expenditure is provisionally 35% higher than in 2018/19, although this includes substantial amounts of one-off expenditures on the energy support packages and index-linked debt interest that should moderate, at least assuming inflation reduces in the coming financial year.

Not shown in the chart is what these numbers mean for public sector net debt, which has increased by £753bn over the past five years from £1,757bn at 1 April 2018 to a provisional £2,530bn at 31 March 2023. This comprises £678bn in borrowing to fund the deficits shown in the chart, and £75bn to fund lending by government and working capital requirements.

Our chart this week may be well presented, but it is not a pretty picture.

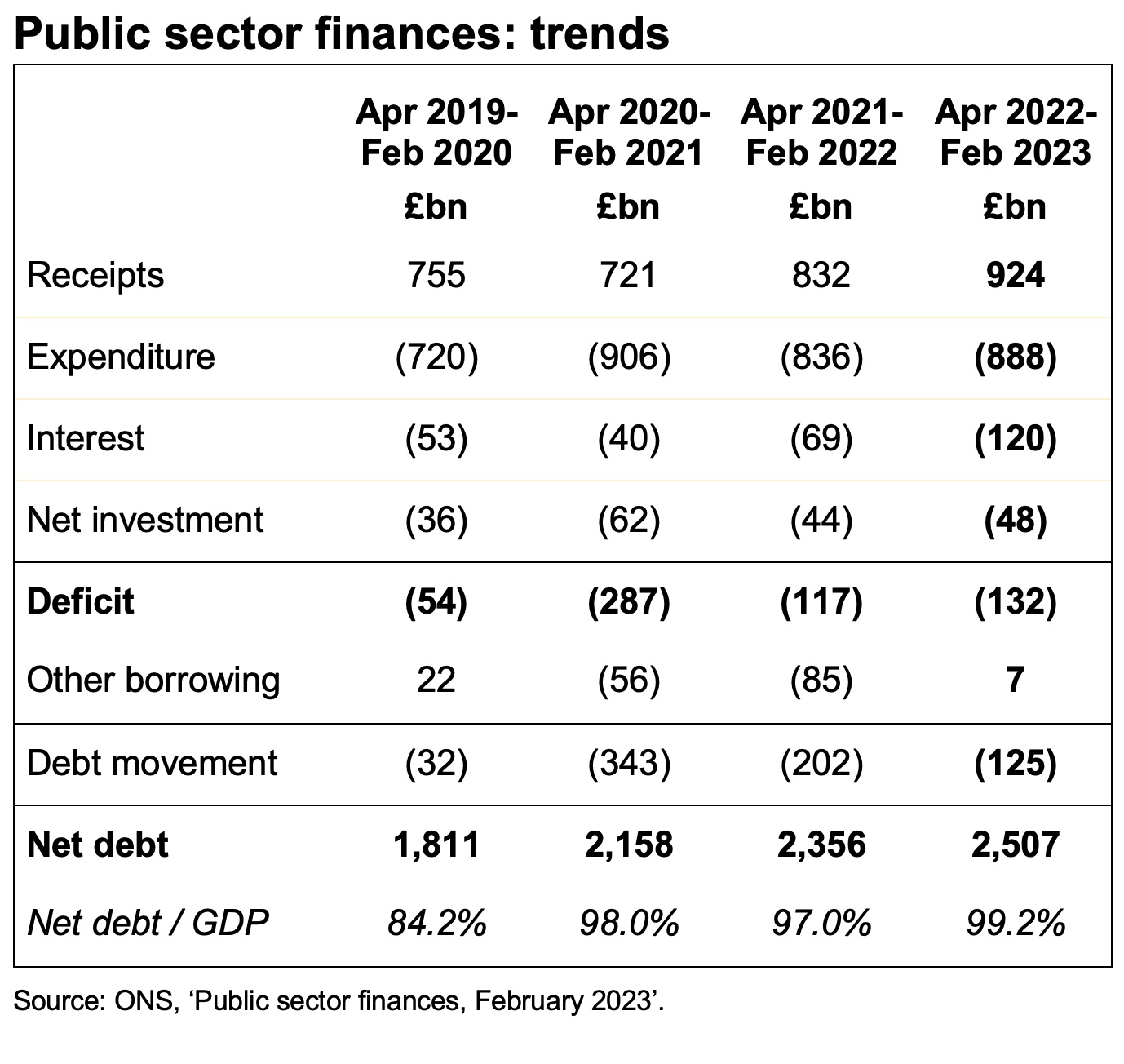

February fiscal deficit hits £17bn, while the cumulative deficit for 11 months of £132bn doesn’t include backdated public sector pay awards.

The monthly public sector finances for February 2023 released on Tuesday 21 March 2023 reported a provisional deficit for the month of £17bn, which is a return to red after a surplus of £8bn last month in January 2023.

The deficit was £10bn more than the £7bn deficit reported for the same month last year (February 2022), as higher interest costs, higher inflation on index-linked debt, and the cost of the energy price guarantee for households and businesses incurred during the month drove up the need to borrow.

The cumulative deficit for the first 11 months of the financial year was £132bn, which is £15bn more than in the same period last year but £155bn lower than in 2020/21 during the first stages of the pandemic. It was £78bn more than the deficit of £54bn reported for the first 11 months of 2019/20, the most recent pre-pandemic pre-cost-of-living-crisis comparative period.

The reported deficit does not reflect backdated public sector pay settlements that have been or are expected to be agreed in March 2023, although the numbers are broadly in line with the £152bn estimated deficit for the full year in the Office for Budget Responsibility (OBR)’s revised forecasts made at the time of the Spring Budget. This was lower than their previous forecast of £177bn in November, primarily because the energy price guarantee is costing less than anticipated.

Public sector net debt was £2,507bn or 99.2% of GDP at the end of February 2023. This is £692bn higher than net debt of £1,815bn on 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic. The OBR’s latest forecast is for net debt to reach £2,546bn by March 2023 and to exceed £2.9trn by March 2028.

Tax and other receipts in the 11 months to 28 February 2023 amounted to £924bn, £91bn or 11% higher than a year previously. Higher income tax and national insurance receipts were driven by rising wages and the higher rate of national insurance for part of the year, while VAT receipts benefited from inflation in retail prices.

Expenditure excluding interest and investment for the 11 months of £888bn was £52bn or 6% higher than the same period in 2021/22, with Spending Review planned increases in spending, the effect of inflation, and the cost of energy support schemes partially offset by the furlough programmes and other pandemic spending in the comparative period not being repeated this year.

Interest charges of £120bn for the 11 months were £51bn or 73% higher than the £69bn reported for the equivalent period in 2021/22, through a combination of higher interest rates and higher inflation driving up the cost of RPI-linked debt.

Cumulative net public sector investment to February was £48bn, £4bn more than this time last year. This is much less than might be expected given the Spending Review 2021 pencilled in significant increases in capital expenditure budgets in the current year.

The increase in net debt of £125bn since the start of the financial year comprised borrowing to fund the deficit for the 11 months of £132bn, less £7bn in net cash inflows from repayments of deferred taxes, and loans made to businesses during the pandemic, less funding for student, business and other loans together with working capital requirements.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “The public finances are back in the red this month as a deficit of £17bn brings the total for the 11 months to February to £132bn, with public sector net debt in excess of £2.5trn. Although broadly in line with the OBR’s improved estimate accompanying the Spring Budget, the numbers don’t reflect the cost of backdated public sector pay settlements to be recorded in the final month of the 2022/23 financial year.

“The chancellor still needs to top up departmental budgets for pay awards in the next financial year, reducing his capacity to address inflationary cost pressures in other areas. HS2 may not be the only capital programme at risk of being scaled back or delayed as he seeks to make savings.”

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The ONS made several revisions to prior period fiscal numbers to reflect revisions to estimates. These had the effect of reducing the reported fiscal deficit for the 10 months ended 31 January 2023 by £1bn to £116bn.

Jeremy Hunt limits his tax and spending ambitions in the Spring Budget to stay within a very tight fiscal rule.

The Spring Budget 2023 for the government’s financial year of 1 April 2023 to 31 March 2024 was presented by the Chancellor of the Exchequer to Parliament on Wednesday 15 March 2023, accompanied by medium-term economic and fiscal forecasts from the Office for Budget Responsibility (OBR) covering the period up to 2027/28.

The fiscal numbers in the Budget are based on the National Accounts prepared in accordance with statistical standards. They differ in material respects from the financial performance and position that will eventually be reported in the Whole of Government Accounts prepared in accordance with International Financial Reporting Standards (IFRS).

A (slightly) lower fiscal deficit in 2023/24

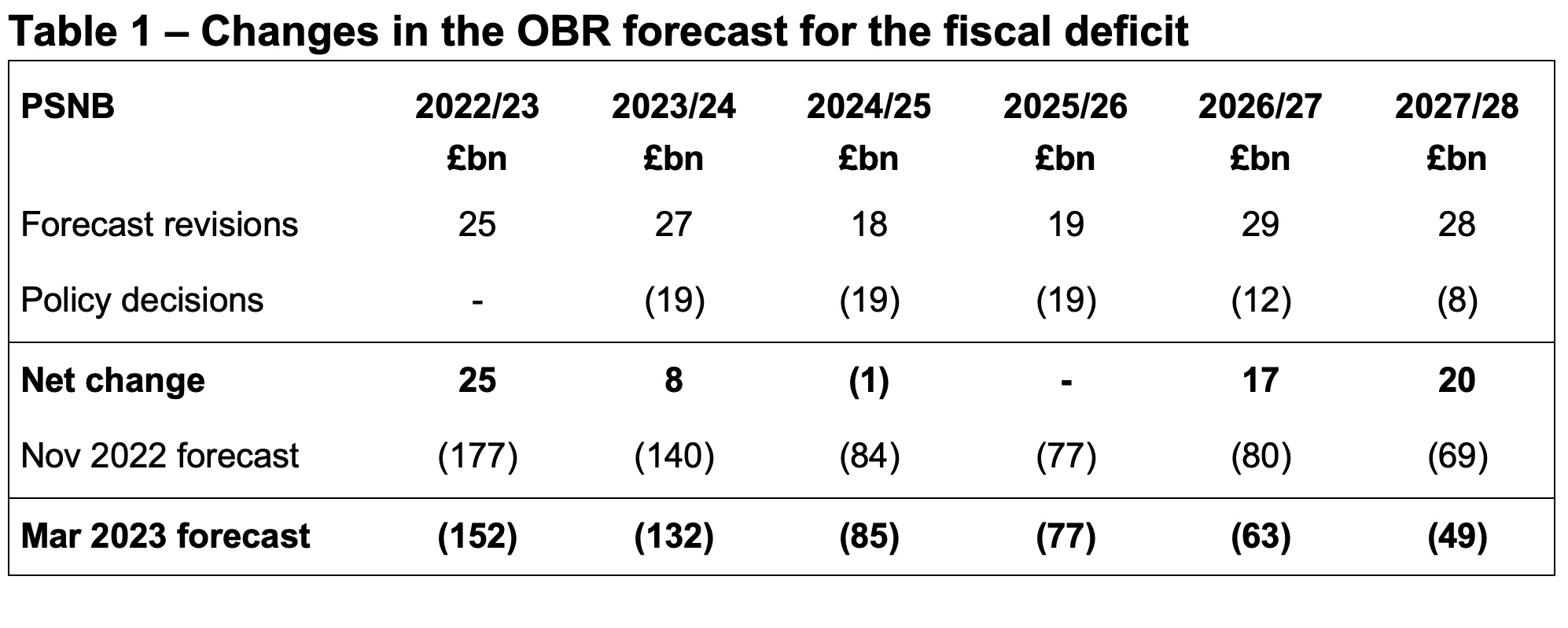

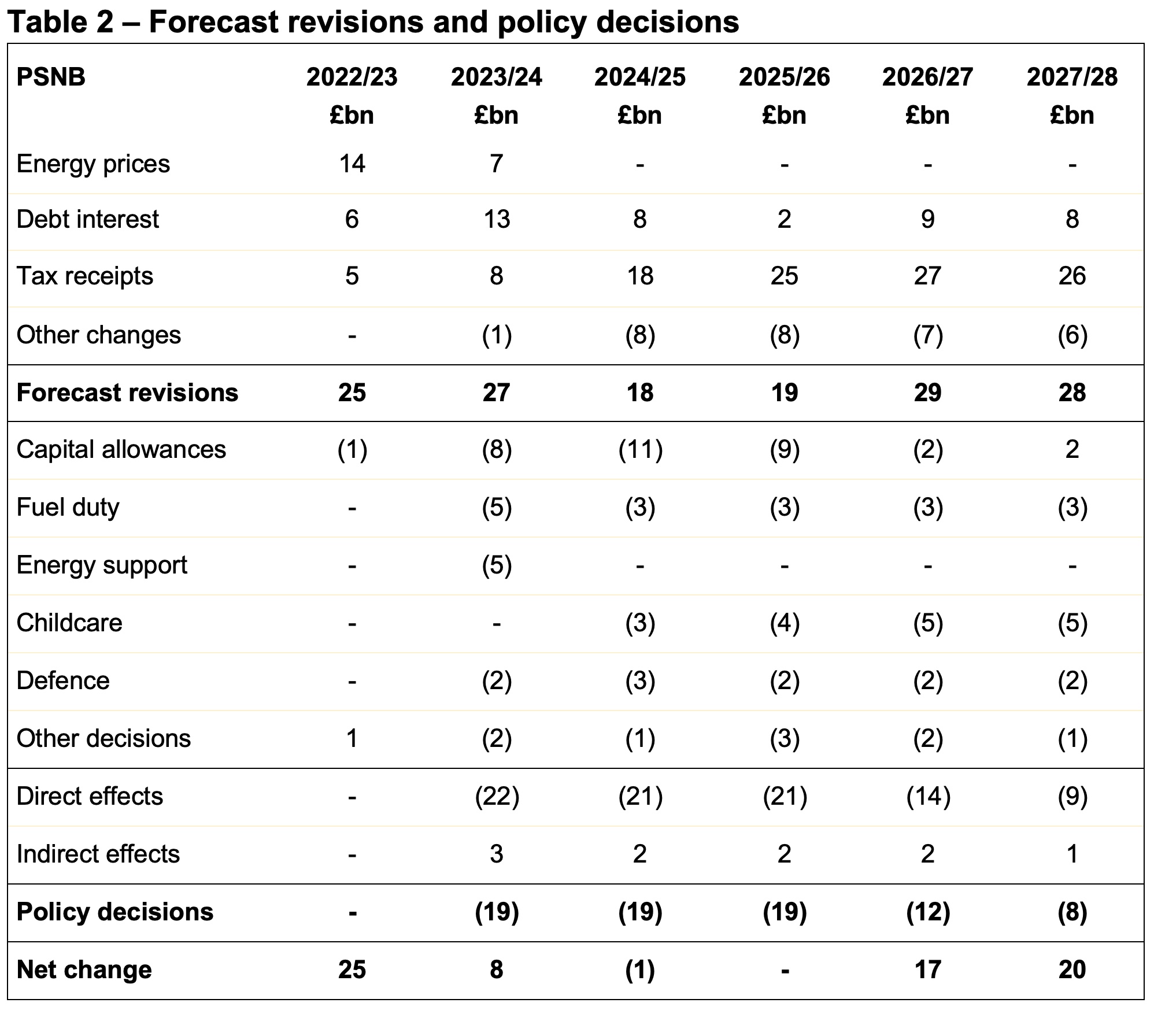

Table 1 shows the Spring Budget estimate for the deficit in 2023/24 is £132bn, £8bn lower than the £140bn forecast in November 2022. Positive revisions to the forecast added £27bn to the bottom line, before £19bn from tax and spending decisions made by the Chancellor.

Forecast revisions in 2023/24 comprised £13bn in lower debt interest, £7bn less in energy support and £8bn in higher tax receipts, less £1bn other changes. The cost of tax and spending decisions in 2023/24 was estimated to be £8bn in lower corporation tax receipts from the full expensing of capital expenditure, £5bn from freezing fuel duties, £5bn from extending the energy price guarantee and other energy support measures, £2bn more for defence and security and £2bn from other decisions, less £3bn in indirect effects of those policy decisions on tax receipts and welfare spending.

Total receipts in 2023/24 are now expected to be £1,057bn (£2bn higher than previously forecast) and total managed expenditure is now anticipated to be £1,189bn (£10bn lower).

The forecast for the deficit in 2024/25 was up £1bn at £85bn and was unchanged in 2025/26 at £77bn, with upward revisions of £18bn and £19bn respectively offset by an estimated £19bn net cost of tax and spending decisions. The latter includes £3bn in 2024/25 and £4bn in 2025/26 for expanded childcare eligibility.

The final two years of the forecast were better by £17bn in 2026/27 (down to a fiscal deficit of £63bn) and by £20bn in 2027/28 (down to £49bn), although several commentators have pointed out this is on the basis of unrealistic spending assumptions that do not take account of significant pressures on public services.

In addition to forecasts for the next five years, the OBR also revised its estimate for the deficit in the current financial year ending 31 March 2023 to £152bn, £25bn lower than November’s estimate of £177bn. This is £53bn more than the OBR’s March 2022 estimate of £99bn and £69bn more than the November 2021 Budget estimate of £83m.

Table 2 provides a breakdown of the forecast changes by year, showing how lower debt interest and higher tax receipts flowing through the forecast period have provided the Chancellor with capacity to extend energy support, incentivise business investment, freeze fuel duty for yet another year (and extend the temporary 5p cut) and increase spending in specific areas.

Receipts and expenditure development

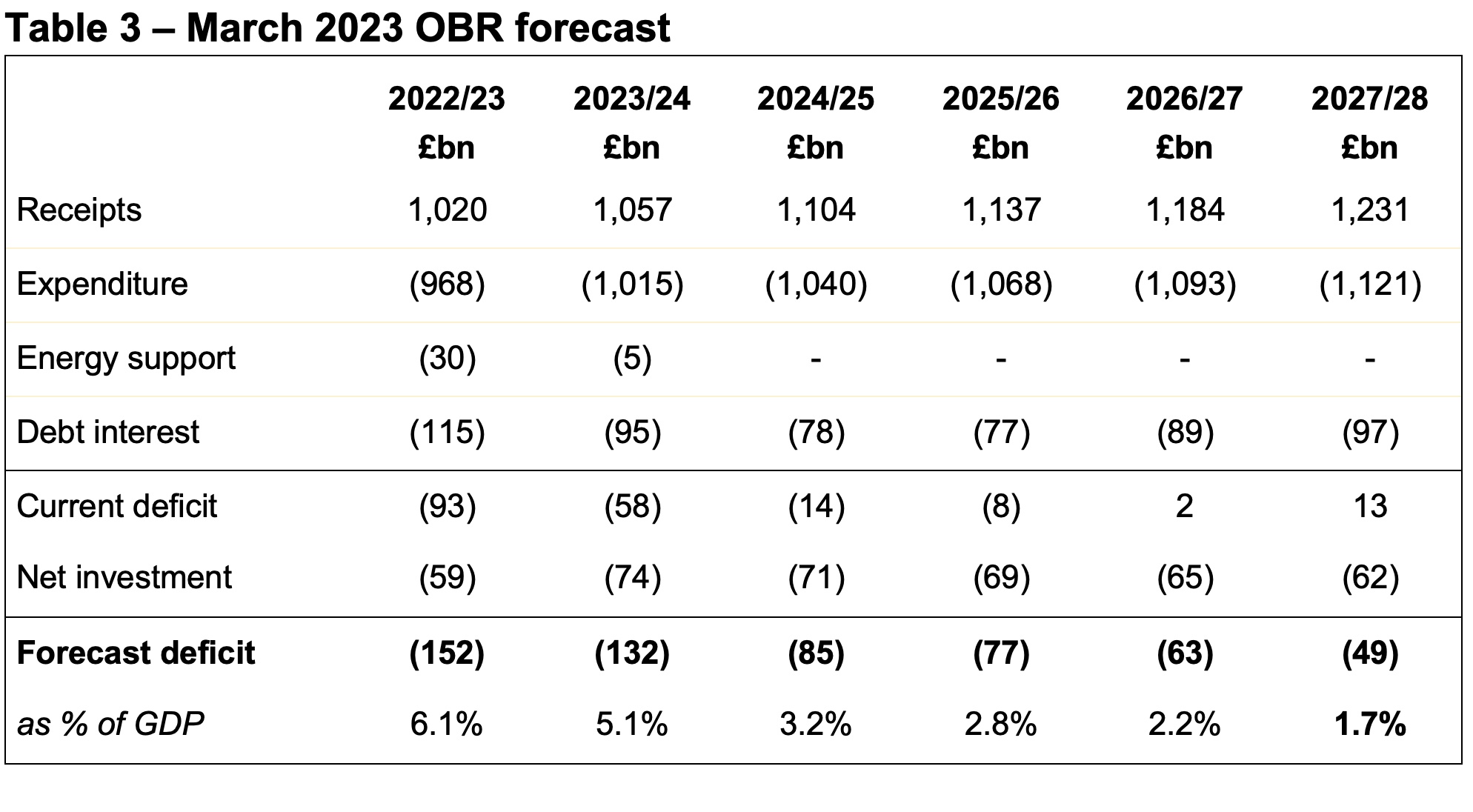

As illustrated by Table 3, receipts are expected to rise from £1,020bn in the current financial year to £1,231bn in 2027/28, while expenditure excluding energy support and interest is expected to rise from £968bn in 2022/23 to £1,121bn in 2027/28..

Interest costs are expected to fall from £115bn this year to £77bn in 2025/26 as interest rates and inflation moderate, before rising to £97bn in 2027/28 based on a growing level of debt.

Net investment is expected to increase in 2023/24 as an £8bn one-off credit from changes in student loan terms in 2022/23 reverses, before declining gradually as capital expenditure budgets flatline and depreciation grows. Public sector gross investment is planned to be £134bn, £134bn, £133bn, £132bn and £132bn over the five years to 2027/28, in effect a cut in real terms over the forecast period.

The government’s secondary fiscal target is to keep the fiscal deficit below 3% of GDP by the end of the forecast period. Based on the March 2023 forecasts, it has headroom of 1.3% of GDP, or £39bn, against this target.

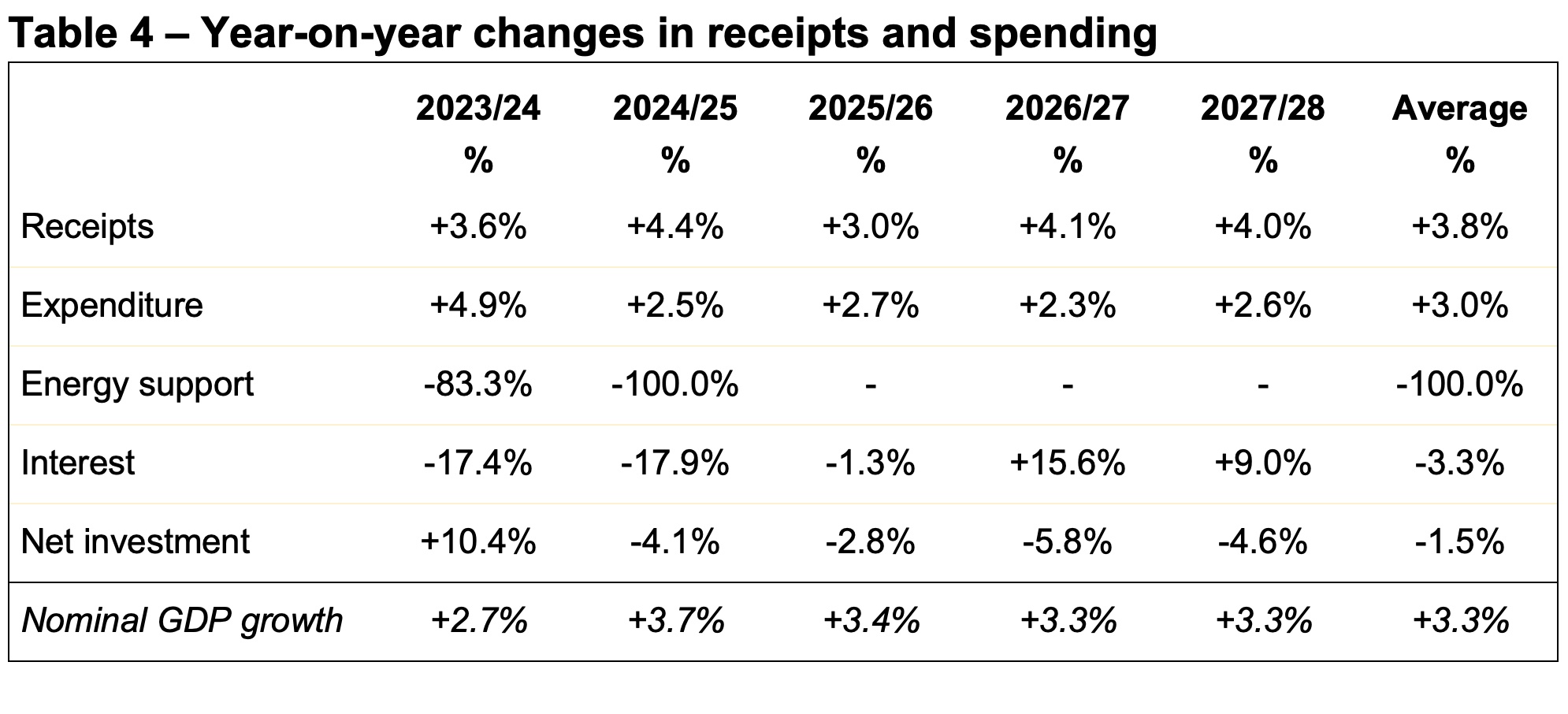

Table 4 provides a summary of the year-on-year changes in receipts and spending, together with the forecast for the increase in the size of the economy, including inflation. This highlights how tax and other receipts are expected to increase faster than the overall rate of growth in the overall size of the economy, while the government plans to constrain the average rise in expenditure excluding energy support and interest to 3.0% including inflation.

The former is principally a result of ‘fiscal drag’ as tax allowances are frozen, bringing in proportionately more in tax as incomes rise with inflation. The latter reflects what is generally considered to be unrealistic plans to constrain public spending in the context of an expected 9% rise in the number of pensioners over the five-year period (that will add to pensions, welfare, health and social care spending), pressure on public sector pay and the deteriorating quality of public services.

Average nominal GDP growth over the five years of 3.3% combines average real-terms economic growth of 1.7% a year and inflation of 1.6%, the latter using the GDP deflator, a ‘whole economy’ measure of inflation. This is different to consumer price inflation, which is forecast to fall to 4.1% in 2023/24 and average 1.4% over the five years to 2027/28.

Public sector net debt

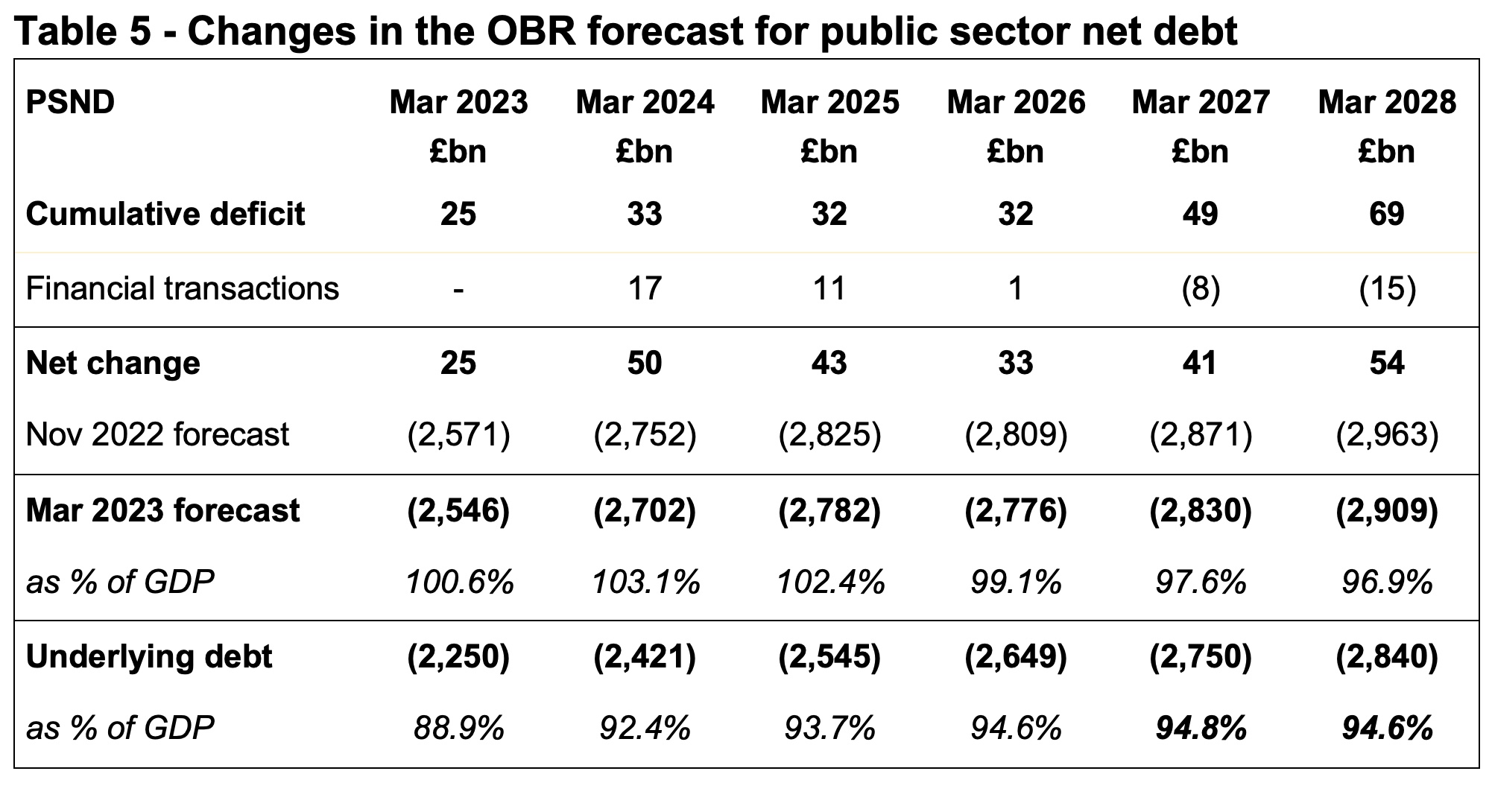

Lower deficits over the forecast period translate into lower borrowing requirements, reducing forecasts for public sector net debt from just under £3.0trn to £2.9trn. This is partly increased or offset by changes in the forecasts for financial and other transactions and working capital movements.

Table 5 shows how forecast public sector net debt is now expected to reach £2,909bn by March 2028, £54bn less than was forecast in November. Although an improvement, debt at the end of the forecast period is expected to be £1,089bn higher than £1,820bn reported for March 2020 before the pandemic, reflecting the large amounts borrowed during the pandemic, in addition to borrowing planned over the next five years.

The government’s primary fiscal target is based on ‘underlying debt’, a non-generally accepted statistical practice measure that excludes the Bank of England and hence quantitative easing balances. Underlying debt needs to be falling as a proportion of GDP between the fourth and fifth year of the forecast period.

The forecast gives the Chancellor just £6.5bn in headroom against this target, with underlying debt / GDP expected to fall from 94.8% to 94.6% between March 2027 and March 2028.

Fiscal rules limit ambitions for tax and spending

Following the disastrous ‘mini-Budget’ of his predecessor Kwasi Kwarteng, the Chancellor’s principal goal has been to stabilise the public finances to provide confidence to debt markets. To do this he has prioritised meeting his fiscal rules over incentivising business investment, cutting taxes and increasing defence spending. He has also adopted what are generally considered to be unrealistic assumptions about public spending in the later years of the forecast to keep within his self-imposed fiscal rules.

This has led to the Chancellor announcing ‘ambitions’ to extend the full expensing of capital expenditure beyond three years and to increase defence and security spending to 2.5% of GDP, as well as continuing to plan for increases in fuel duties each year despite the repeated practice of cancelling these rises.

Because these are ambitions and not plans, they are not incorporated into the forecasts enabling fiscal targets to be met. The OBR reports that continuing to cancel fuel duty rises each year would reduce the headroom to just £2.8bn, while converting the Chancellor’s ambitions to extend full expensing beyond three years and to increase defence spending to 2.5% of GDP into formal plans would cause him to breach his primary fiscal rule.

Conclusion

The overall fiscal position remains weak, with public finances vulnerable to potential economic shocks.

The Chancellor has followed the practice of many of his predecessors in increasing planned borrowing when fiscal forecasts worsen, as occurred in November 2022, only to then use upsides from improvements in subsequent forecasts to fund new tax and spending commitments. This ratchets up borrowing and debt as forecasts fluctuate and creates instability in both tax policy and public spending plans.

The consequence is a relatively unchanged fiscal position for the financial year commencing 1 April 2023 and the two subsequent financial years, as tax and spending decisions offset forecast upsides. And although there is an anticipated improvement in the projected fiscal position in the final two years of the OBR’s five-year forecast (after the next general election), the likelihood is that it will be offset in due course by the reality of pressures on public service and welfare budgets.

There is a reason why the first Budget following a general election typically sees taxes rise and the Spring Budget 2023 suggests that this pattern is likely to be repeated, irrespective of whichever party wins power.

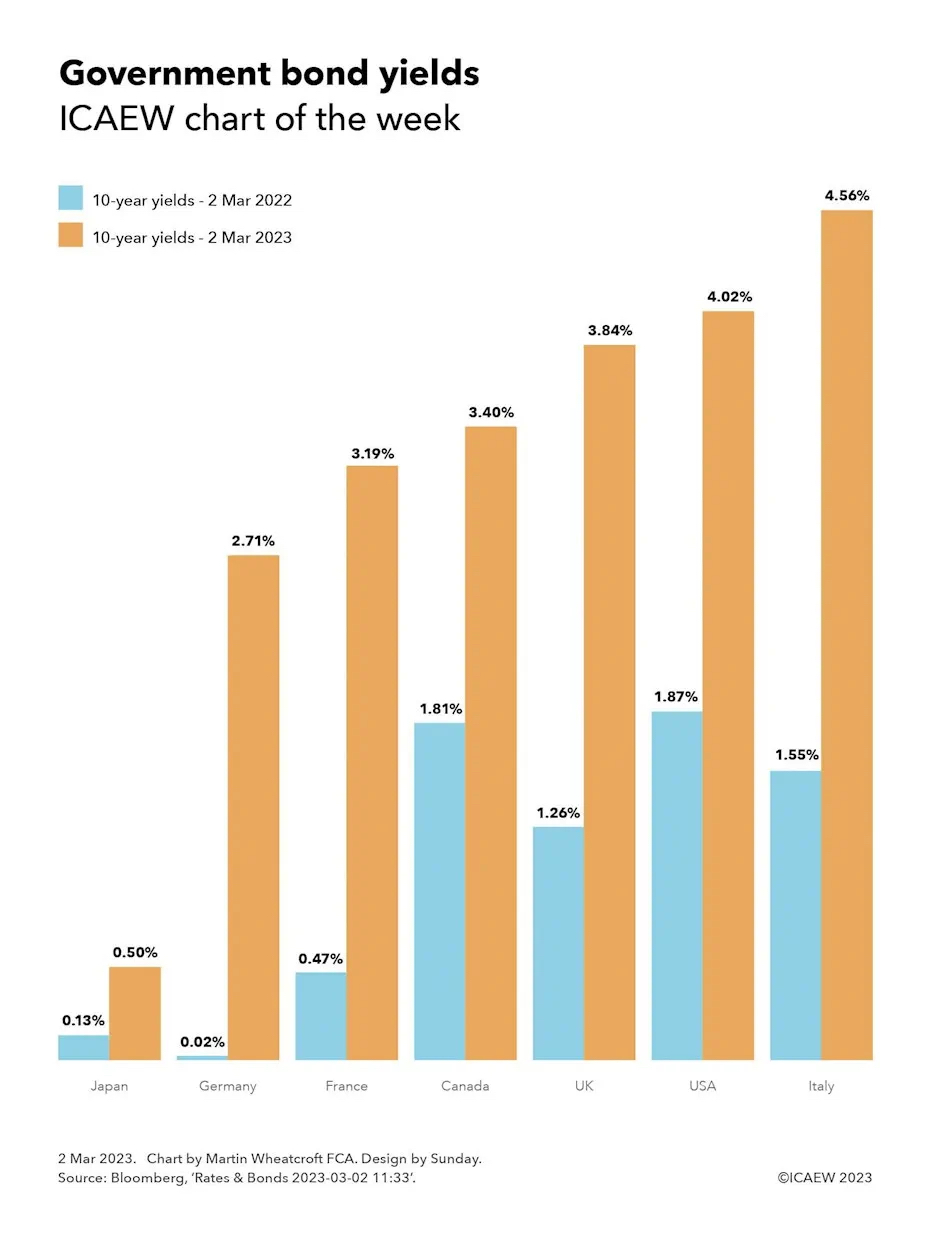

My chart this week looks at what a difference one year has made to the cost at which governments around the world can borrow.

The past year has seen a dramatic change in economic fundamentals around the world as inflation has surged and growth has stuttered. One of the most dramatic changes has been to the cost of new government borrowing, with the yields payable by governments to sovereign debt investors increasing significantly from where they were a year ago.

As our chart of the week illustrates, Japan has seen yields on 10-year government bonds increase from 0.13% on 2 Mar 2023 to 0.50% on 2 Mar 2023, a far cry from the negative yields it has obtained over much of the last decade when (in effect) investors were paying the government of Japan for the privilege of lending it money. The change for Germany has been even more marked, from a position a year ago where it could borrow over 10 years for almost nothing (0.02%) to today where if it wanted to raise new funds it would pay an interest rate of 2.71% over 10 years.

The other members of the G7 have also seen the effective interest rate payable on 10-year government bonds rise, with France going from 0.47% a year ago to 3.19% today, Canada from 1.81% to 3.40%, the UK from 1.26% to 3.84%, the USA from 1.87% to 4.02%, and Italy from 1.55% to 4.56%.

Yields from 10-year government bonds are seen as a benchmark rate for most countries, as although governments can and do borrow for much longer periods – with market data often available for 20-year and 30-year bonds as well – most countries have average maturities of much shorter periods. The UK is an outlier in this respect with an average debt maturity on government securities of just over 15 years (before taking account of quantitative easing), in contrast with the more typical average maturity of seven years for Italian government debt.

Although the amount payable on new debt has risen significantly, this should in theory feed in to overall cost of government borrowing gradually as it will take time for existing government bonds to mature and be refinanced. For some time to come the overall cost of borrowing will continue to benefit from medium- and long-term government bonds that were issued at the ultra-low borrowing rates experienced over the last decade or so.

However, in practice not all government borrowing is at fixed rates, with many governments (including the UK) issuing inflation-linked debt, adding to their interest costs as inflation has surged. In addition, some government debt is short term or pays a variable rate of interest, while quantitative easing has seen central banks swap a substantial proportion of fixed-rate government bonds into variable-rate central bank deposits, increasing governments’ exposure to changes in short-term interest rates.

Either way, the rapid rise in the interest rates payable on sovereign debt marks a significant shift in the fiscal calculus for most governments when combined with much higher levels of debt in most developed countries. Lots more pounds, euros, dollars and yen will need to be diverted to servicing debt, making for hard choices for finance ministers as they work out their budgets for coming years.

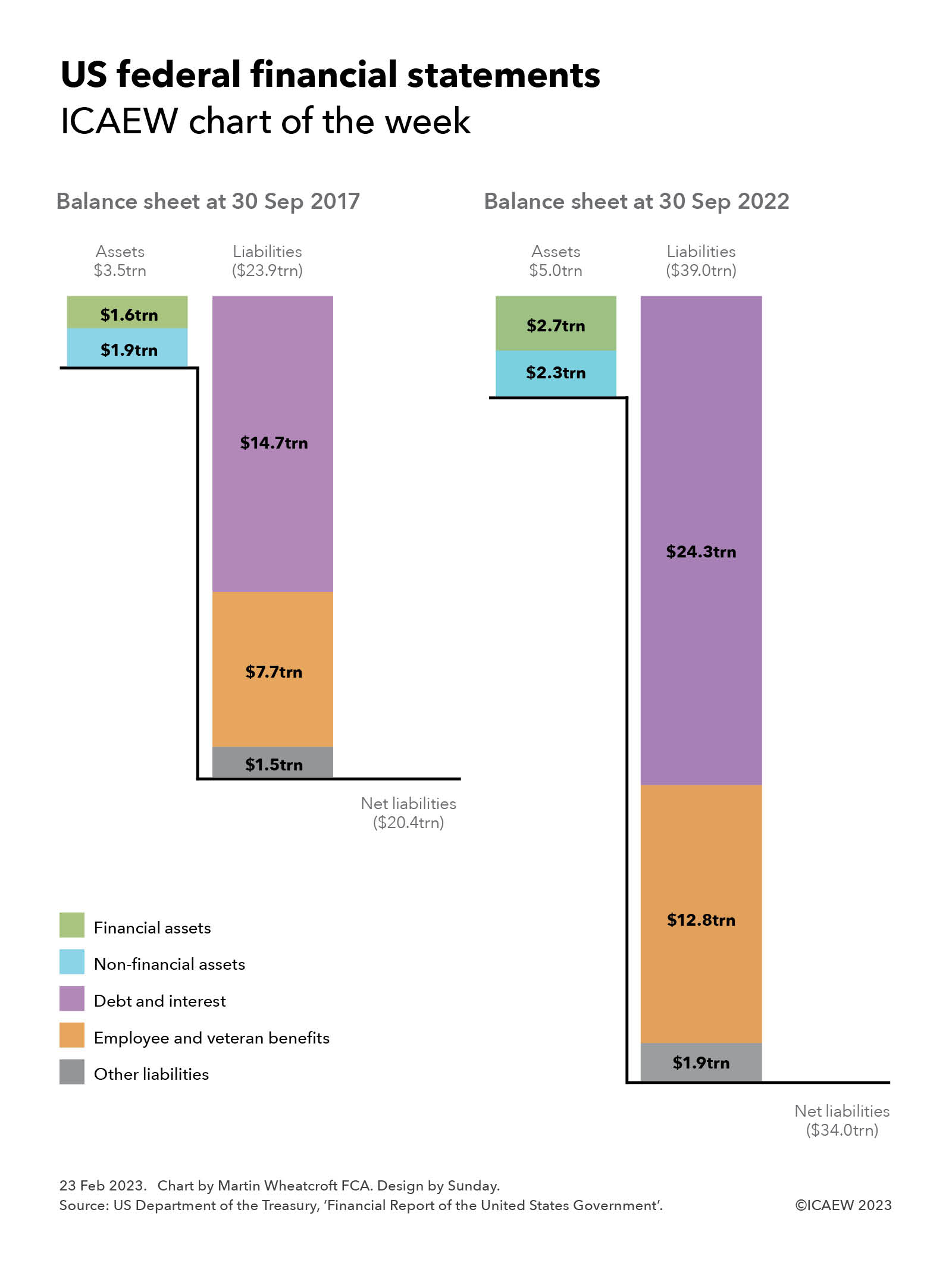

My 250th chart of the week for ICAEW takes a look at the recently published Financial Report of the United States Government for the year ended 30 September 2022 and how net liabilities have increased by 67% to $34trn over the past five years.

This week’s chart takes a dive into the latest financial statements of the United States Government for the year ended 30 September 2022 that were published on 16 February 2023, illustrating how the consolidated balance sheet of the executive, legislative and judicial branches has changed over the last five years.

The federal government reported net liabilities of $20.4trn at 30 September 2017, comprising $3.5trn in assets ($1.9trn non-financial and $1.6trn financial) less $23.9trn in liabilities ($14.7trn debt and interest, $7.7trn employee and veteran benefits and $1.5trn other liabilities).

By 30 September 2022, net liabilities had increased by 67%, from $13.6trn to $34.0trn, comprising $5.0trn in assets ($2.3trn non-financial and $2.7trn financial) less $39.0trn in liabilities ($24.3trn debt and interest, $12.8trn employee and veteran benefits and $1.9trn other liabilities).

The increase in net liabilities is a consequence of net accounting losses of $1.2trn, $1.4trn, $3.8trn, $3.1trn and $4.2trn for the five financial years up to 30 September 2022. These amounts are calculated in accordance with US generally accepted accounting principles (US GAAP) as adapted for government by Federal Financial Accounting Standards (FFAS) issued by the Federal Accounting Standards Advisory Board (FASAB). They differ from cash budget deficits (outlays less receipts) of $0.8trn, $1.0trn, $3.1trn, $2.8trn and $1.4trn over the same period.

Revenue in the year ended 30 September 2022 of $4.9trn comprised $4.0trn from individual income taxes and tax withholdings, $0.4trn in corporate income taxes and $0.5trn in other taxes and receipts. The net cost of government operations amounted to $9.1trn, comprising $7.4trn in gross costs less $0.5trn in fees and charges plus $2.2trn from changes in assumptions. The latter primarily relate to employee and veteran benefit obligations that are on the balance sheet in the US GAAP numbers.

The scale of the negative balance sheet and continued deficit financing highlight just how dependent the US federal government is on its ability to borrow money as needed to meet its financial obligations as they fall due, and why the current challenge in raising its self-imposed debt ceiling is starting to concern markets.

This is the 250th ICAEW chart of the week, a milestone that has crept up on us as we seek to share insights into the economy and public finances that we hope are of interest to ICAEW members and all our other readers. Many thanks for your continued interest and we look forward to providing you with many more nuggets in the future.

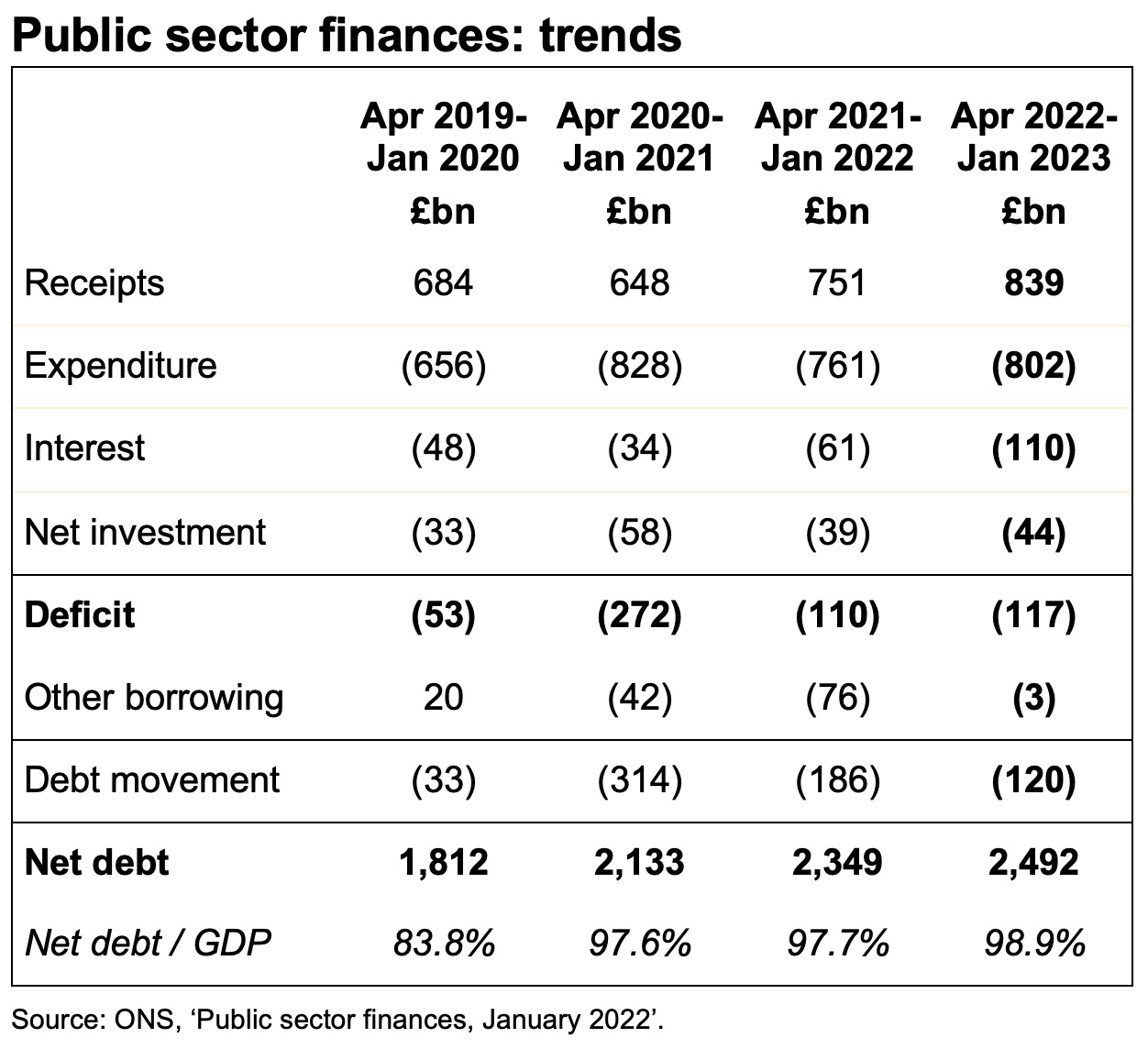

Better than expected self assessment tax receipts helped generate a small fiscal surplus of £5bn in January, reducing the year-to-date deficit to £117bn, £7bn more than the comparative period in the previous financial year.

The monthly public sector finances for January 2023 released on Tuesday 21 February 2023 reported a provisional surplus for the month of £5bn. This was a significant improvement over the deficit of £26bn reported for the previous month (December 2022), but £7bn less than the surplus reported for the same month last year (January 2022).

A surplus arose primarily because better than expected self assessment tax receipts were sufficient to offset the effect of higher interest costs, higher inflation on index-linked debt, and the cost of the energy price guarantee for households and businesses incurred during the month. January also saw the Office for National Statistics (ONS) record a £2bn charge for custom duties that the UK had failed to collect when it was a member of the EU Customs Union.

The cumulative deficit for the first 10 months of the financial year was £117bn, which is £7bn more than in the same period last year but £155bn lower than in 2020/21 during the first stages of the pandemic. It was £64bn more than the deficit of £53bn reported for the first 10 months of 2019/20, the most recent pre-pandemic pre-cost-of-living-crisis comparative period.

The deficit was £22bn below the Office for Budget Responsibility (OBR)’s revised forecast made at the time of the Autumn Statement in November, primarily because the energy price guarantee has cost less than anticipated.

Public sector net debt was £2,492bn or 98.9% of GDP at the end of January 2023, dipping below the £2.5tn reported last month because of corrections to prior month data. This is £672bn higher than net debt of £1,820bn at 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic. The OBR’s latest forecast is for net debt to reach £2,571bn by March 2023 and to approach £3trn by March 2028.

Tax and other receipts in the 10 months to 31 January 2023 amounted to £839bn, £88bn or 12% higher than a year previously. Higher income tax and national insurance receipts were driven by rising wages and the higher rate of national insurance for part of the year, while VAT receipts benefited from inflation in retail prices.

Expenditure excluding interest and investment for the ten months of £802bn was £41bn or 5% higher than the same period in 2021/22, with Spending Review planned increases in spending, the effect of inflation, and the cost of energy support schemes partially offset by the furlough programmes and other pandemic spending in the comparative period not being repeated this year.

Interest charges of £110bn for the 10 months were £49bn or 80% higher than the £61bn reported for the equivalent period in 2021/22, through a combination of higher interest rates and higher inflation driving up the cost of RPI-linked debt.

Cumulative net public sector investment to January was £44bn, £5bn more than a year previously. This is much less than might be expected given the Spending Review 2021 pencilled in significant increases in capital expenditure budgets in the current year.

The increase in net debt of £120bn since the start of the financial year comprised borrowing to fund the deficit for the 10 months of £117bn together with a further £3bn to fund student loans, lending to businesses and others, and working capital requirements, net of cash inflows from repayments of deferred taxes and loans made to businesses during the pandemic.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “With a small surplus, January’s fiscal numbers benefited from stronger self-assessment tax receipts than expected, providing some comfort to Chancellor Jeremy Hunt as he assembles his first Budget. The deficit for the current financial year is still on track to be one of the highest ever recorded, reaching £117bn for the ten months to January 2023 after energy support and interest costs more than offset the benefit of higher tax receipts.

“Although it appears that inflation has peaked, the near-term economic outlook continues to deteriorate and so calls for immediate tax cuts are likely to remain unanswered. We are asking the Chancellor to take urgent action to eliminate the backlog at HMRC that is inhibiting business growth, and to make improving the resilience of the UK economy and the public finances a priority.”

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The ONS made several revisions to prior period fiscal numbers to reflect revisions to estimates. These had the effect of reducing the reported fiscal deficit for the nine months ended 31 December 2022 by £6bn to £122bn and reducing the reported fiscal deficit for the year to 31 March 2022 by £1bn to £122bn.

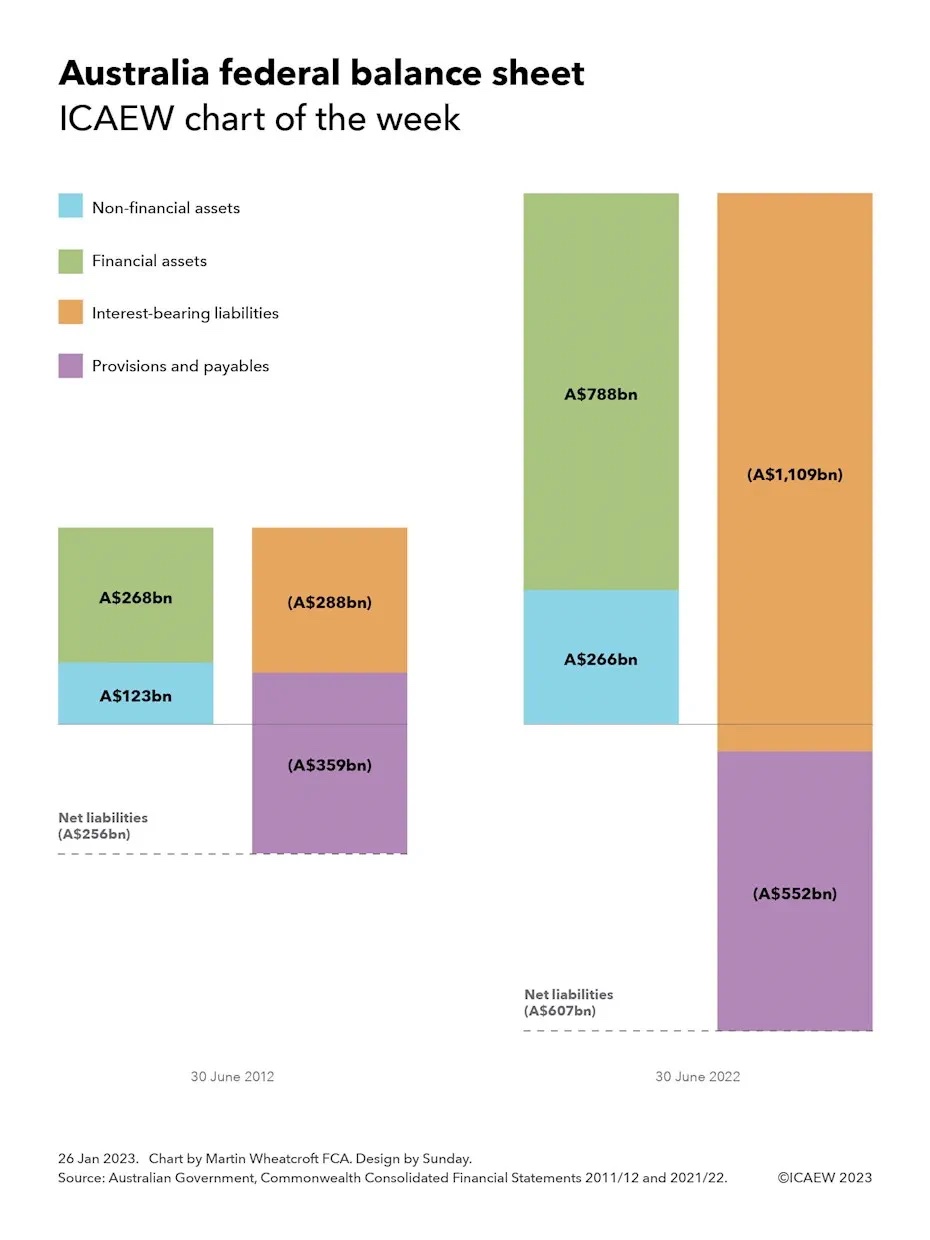

Our chart heads down under this week to take a look at how the reported financial position of Australia’s federal government has changed over the last decade.

Australia Day on 26 January provides an opportunity to take a look at the federal balance sheet for Australia. This is included in the audited consolidated financial statements of the Commonwealth of Australia that are prepared in accordance with Australian Accounting Standards, which generally align with International Financial Reporting Standards (IFRS), although AASB 1049 Whole of Government and General Government Sector Financial Reporting diverges from IFRS in some aspects. They encompass the federal level of government in Australia, excluding states, territories and local authorities.

Our chart shows how the balance sheet has grown over the last 10 years, from net liabilities of A$256bn at 30 June 2012 (£147bn at the current exchange rate of A$1.77:£1.00) to A$607bn at 30 June 2022 (£348bn).

At 30 June 2012, the balance sheet comprised non-financial assets of A$123bn and financial assets of A$268bn, less interest-bearing liabilities of A$288bn, and provisions and payables of A$359bn to give a negative net worth of $256bn. These balances had grown to non-financial assets of A$266bn and financial assets of A$788bn at 30 June 2022, less interest bearing liabilities of A$1,109bn, and provisions and payables of A$552bn.

Non-financial asset balances grew over the 10 years from 2012 to 2022 with land and buildings increasing from A$35bn to A$66bn, military equipment A$40bn to A$81bn, other plant, equipment and infrastructure $19bn to A$72bn, intangibles A$7bn to A$15bn, heritage and cultural assets A$10bn to A$13bn, and other from A$12bn to A$19bn.

Financial assets also grew, with investments and loan balances increasing from A$197bn to A$640bn, advances from A$27bn to A$70bn, receivables and accrued revenue from A$39bn to A$69bn, and cash from A$5bn to A$9bn. A substantial proportion of this growth relates to the Australia Future Fund, a sovereign wealth fund that was established in 2006 primarily to cover the costs of paying for unfunded pension obligations, together with a series of smaller funds intended to support infrastructure investment, disability insurance, medical research, indigenous communities and natural disasters.

Interest-bearing liabilities increased significantly as a consequence of the pandemic, with government securities increasing from A$268bn to A$577bn over the 10 years to June 2022, central bank and other deposits from A$3bn to A$426bn, and loans, leases and other interest bearing liabilities from A$17bn to A$106bn.

Provisions and payables grew by a lesser extent, with superannuation and other employee liabilities increasing from A$252bn to A$359bn, Australian currency on issue from A$54bn to A$102bn, payables from A$23bn to A$27bn, and provisions from A$30bn to A$64bn.

While negative net worth has increased from 17% of GDP to 24% of GDP over the 10 years, principally as a consequence of the pandemic in the last couple of years, the establishment of the Australia Future Fund, the move of federal employees from defined benefit to defined contribution pension arrangements, and active management of the balance sheet means that Australia is in a much healthier fiscal position than many other developed countries.

For the Australian Department of the Treasury at least, this should make for a happy Australia Day.

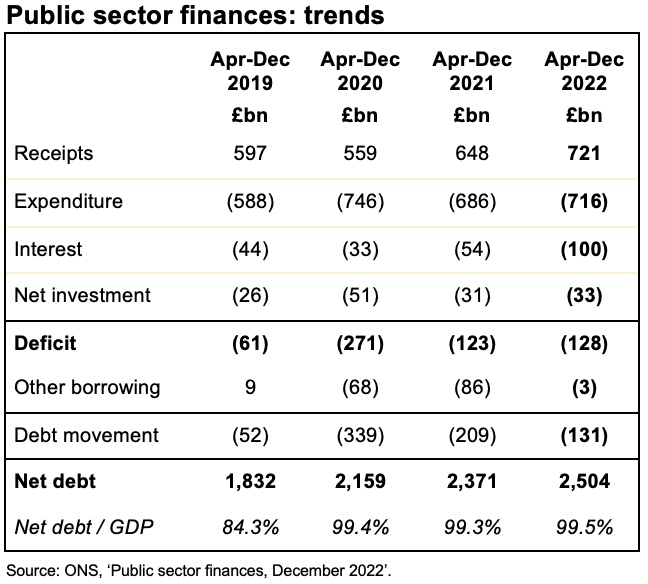

The highest December deficit on record has been driven by higher debt interest costs and the cost of energy support schemes.

The monthly public sector finances for December 2022, released on Tuesday 24 January 2023, reported a provisional deficit for the month of £27bn, the highest December deficit since records began in 1993. This was despite a mild December helping to mitigate some of the cost of energy support schemes.

The deficit for the month of £27bn was £12bn higher than the equivalent month in the previous financial year (December 2021) and £8bn more than the previous month (November 2022).

This brought the cumulative deficit for the first three quarters of the financial year to £128bn, which is £3bn below the Office for Budget Responsibility (OBR)’s revised forecast made at the time of the Autumn Statement last November. This substantially exceeds the budget of £99bn for the entire financial year to March 2023 forecast by the OBR at the time of the Spring Statement as higher interest costs, the effect of higher inflation on index-linked debt, and the cost of the energy price guarantee for households and businesses over the winter all add to public spending.

Public sector net debt was £2,504bn or 99.5% of GDP at the end of December 2022, up £131bn from £2,373bn at the end of March 2022. This is £684bn higher than net debt of £1,820bn on 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic.

The OBR’s latest forecast is for net debt to reach £2,571bn by March 2023 and to approach £3trn by March 2028, although energy prices falling faster than expected may help improve the outlook somewhat.

The cumulative deficit for the first three quarters of the financial year of £128bn was £5bn lower than this time last year and £143bn lower than in 2020/21 during the first stages of the pandemic. However, it was £67bn more than the deficit of £61bn reported for the first nine months of 2019/20, the most recent pre-pandemic pre-cost-of-living-crisis comparative period.

Tax and other receipts in the three quarters to 31 December 2022 amounted to £721bn, £73bn or 11% higher than a year previously. Higher income tax and national insurance receipts were driven by rising wages and the higher rate of national insurance, while VAT receipts benefited from inflation in retail prices. Year-to-date receipts included £3.7bn accrued for the energy profits levy ‘windfall tax’.

Expenditure excluding interest and investment for the nine months of £716bn was £30bn or 4% higher than the same period in 2021/22, with Spending Review planned increases in spending, high inflation and the cost of energy support schemes more than offsetting the furlough programmes and other pandemic spending in the comparative period not repeated this year.

Interest charges of £100bn for the three quarters were £46bn or 85% higher than the £54bn reported for the equivalent period in 2021/22, through a combination of higher interest rates and higher inflation driving up the cost of RPI-linked debt.

Cumulative net public sector investment to December was £33bn. This is £2bn more than a year previously, much less than might be expected given the Spending Review 2021 pencilled in significant increases in capital expenditure budgets in the current year.

The increase in net debt of £131bn since the start of the financial year comprised borrowing to fund the deficit for the nine months of £128bn together with a further £3bn to fund student loans, lending to businesses and others, and working capital requirements, net of cash inflows from repayments of deferred taxes and loans made to businesses during the pandemic.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “A mild December was not enough to prevent public debt from reaching £2.5tn for the first time, in a disappointing set of numbers for December 2022. However, the Chancellor will take comfort that cumulative borrowing for the first three quarters of the financial year was less than feared when the budget for 2022/23 was updated back in November. Energy prices coming down much faster than expected should also improve the outlook for the final quarter as well as the new financial year.

“The deficit is still on track to be one of the highest ever recorded in peacetime and stabilising the fiscal position is the best that Jeremy Hunt can hope for in the short term. Amid a sea of red ink, sustainable public finances remain a distant prospect for now.”

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The ONS made several revisions to prior period fiscal numbers to reflect revisions to estimates. These had the effect of reducing the reported fiscal deficit for the eight months ended 30 November 2022 by £5bn to £101bn and reducing the reported fiscal deficit for the year to 31 March 2022 by £2bn to £123bn.

The revisions in the current year principally relate to an increase of £4bn in the estimate for accrued corporation tax receipts at 30 November 2022, while the prior year numbers were updated to reflect a £0.7bn correction to reported VAT cash receipts during 2021/22 and a £1bn increase in the estimate for accrued corporation tax receipts at 31 March 2022.

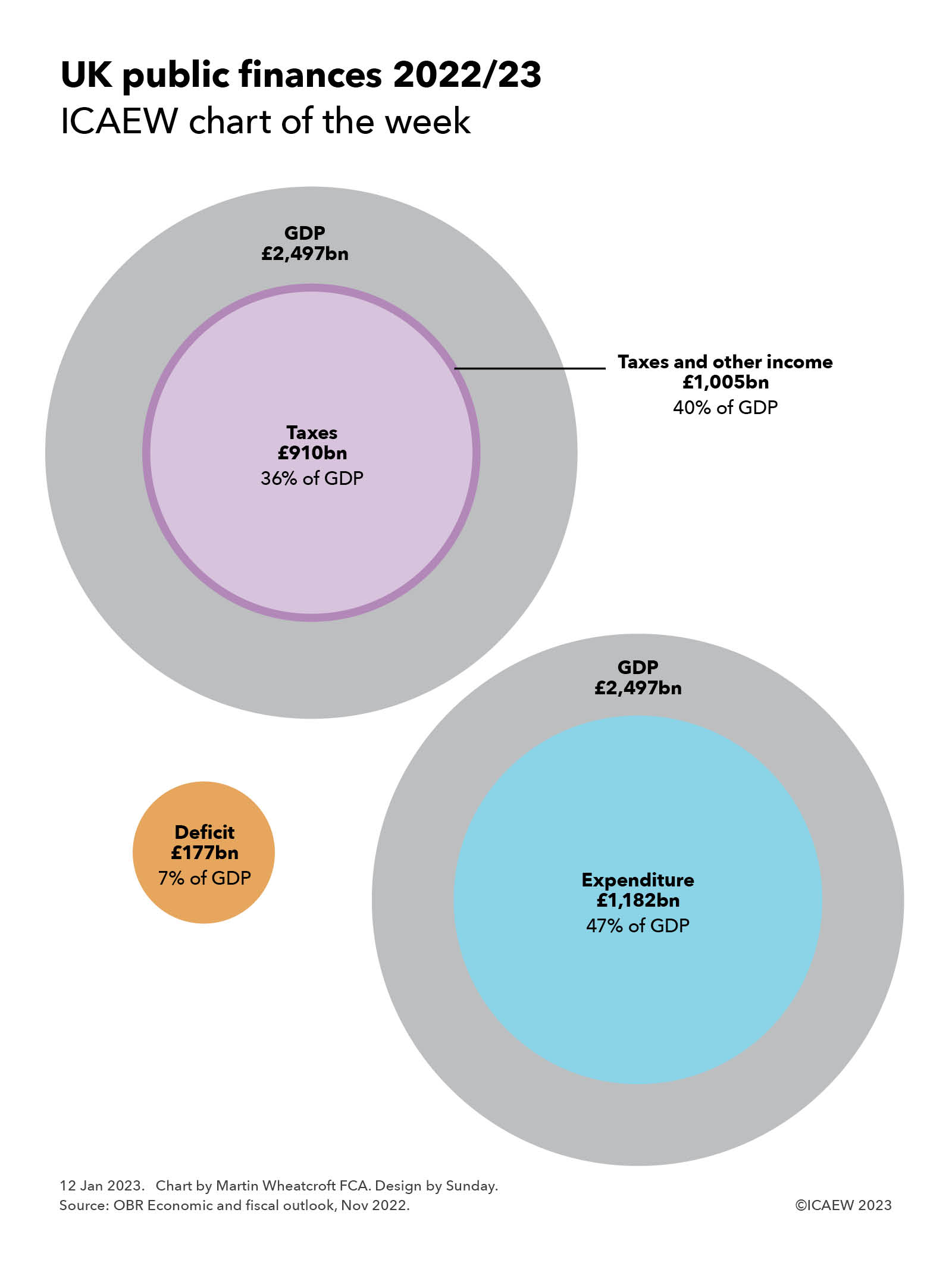

Our chart this week compares the UK public finances for the current fiscal year with the overall size of the economy, illustrating how taxes are expected to amount to 36% of GDP and expenditure 47% of GDP.

The latest official forecast from the Office for Budget Responsibility (OBR) for the current fiscal year ending 31 March 2023 is for a shortfall (or ‘deficit’) of £177bn between receipts of £1,005bn and expenditure of £1,182bn. The largest component of receipts is taxation, which is forecast to amount to £910bn.

Our chart puts these numbers into context by comparing them with the forecast for Gross Domestic Product (GDP) of £2,497bn in 2022/23, highlighting how taxes are expected to amount to 36% of GDP, receipts including other income to 40% of GDP, and expenditure to 47% of GDP, resulting in a deficit amounting to 7% of GDP.

As many commentators have noted, taxes are at a historically high level, with taxation at its highest level as a share of economic activity since 1949. This is unsurprising given the combination of many more people living longer lives and the financial commitments made by successive governments to pay for pensions, health and (to an extent) social care.

Expenditure is also at historically high levels, with energy support packages adding to recurring expenditure of around 43% or 44% of GDP. This is below the peak of 53% of GDP a couple of years ago at the height of the pandemic.

As a consequence, the shortfall between receipts and expenditure of 7% of GDP is elevated compared with the 2% to 3% of GDP ‘normal’ range, although still below the 15% of GDP seen in 2020/21 during the pandemic and 10% of GDP in 2009/10 during the financial crisis.

The increase in the corporation tax rate to 25% from April means that receipts are expected to increase to 37% of GDP over the next few years, leading to the total of taxes and other receipts rising to 41%. At the same time total expenditure is expected to stay at 47% of GDP in 2023/24 before falling back to 45% in 2024/25, 44% in 2025/26 and 2026/27, and 43% in 2027/28.

Unlike in previous generations, the government is restricted in its ability to cut other areas of spending to cover expected further rises in spending on pensions, health and social care as the number of pensioners continues to grow. Savings in the defence and security budgets are no longer possible now that spending has fallen to not much more than the NATO minimum of 2% of GDP, down from in excess of 10% back in the day, while pressures across many other areas of the public sector will make achieving the cost savings already assumed in the forecasts a significant challenge.

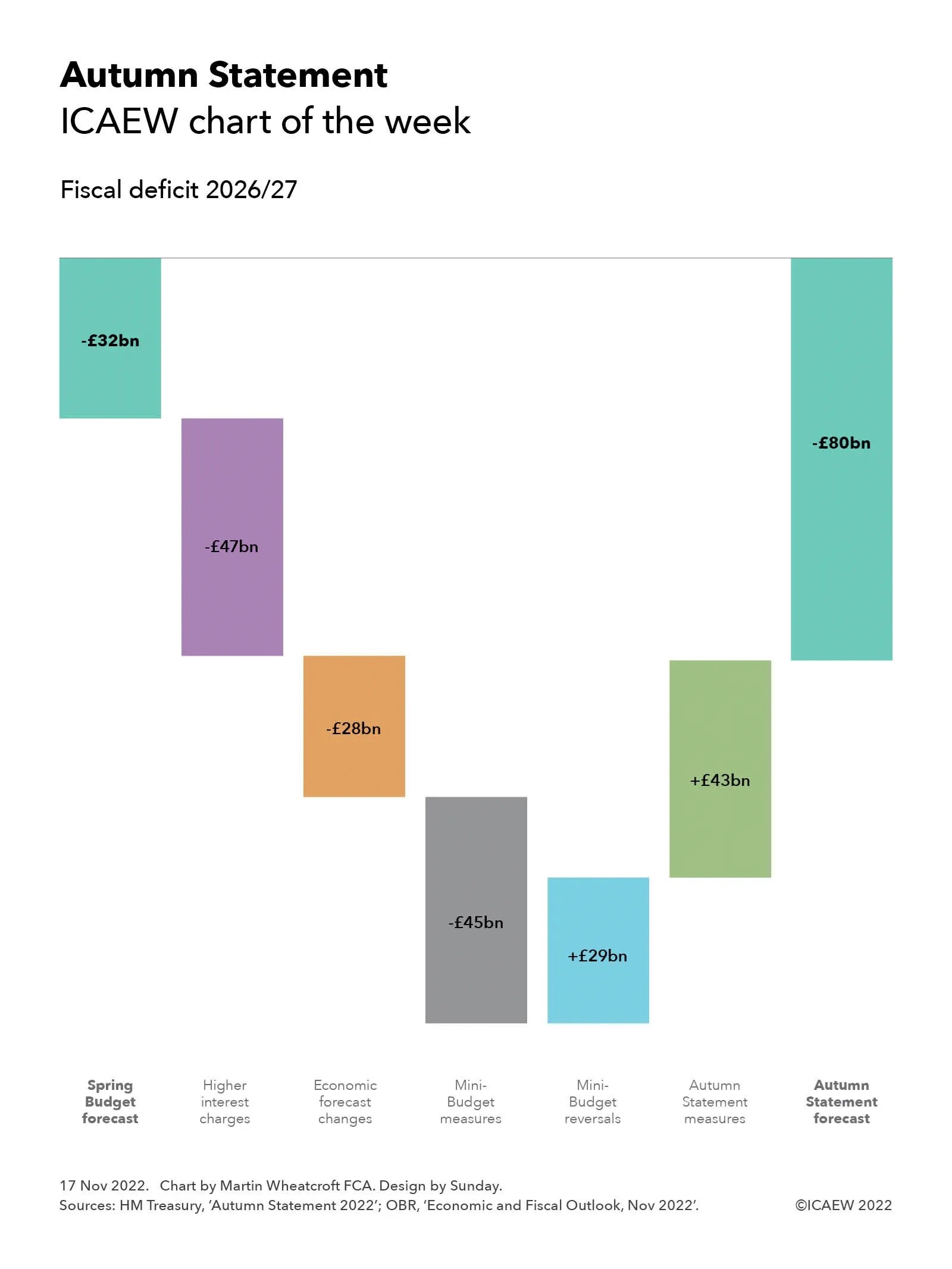

The public finances have been a rollercoaster ride over the last few months, as illustrated by this week’s chart showing how the forecast for the fiscal deficit in 2026/27 has changed since the Spring Budget.

Former Chancellor and now Prime Minister Rishi Sunak expressed some optimism back in March when he presented his Spring Budget, commenting how he remained committed to achieving a current budget surplus despite the huge amounts spent supporting individuals and businesses through the pandemic, and the support he was then offering to help with energy bills as they started to soar.

My chart this week illustrates how the fiscal situation has deteriorated significantly as rising interest rates, accelerating inflation, and an economy entering recession have adversely affected the public finances. Together with the additional energy support measures announced by then Prime Minister Liz Truss in September, the shortfall between receipts and expenditure is expected to be £270bn higher over a five-year period to 2026/27 than was forecast by the Office for Budget Responsibility back in March.

In 2026/27 itself (the year ending 31 March 2027), interest charges are expected to be £47bn higher than previously forecast, while tax receipts and other forecast changes are expected to require an extra £28bn in additional funding (of which £25bn relates to lower tax receipts).

In theory this would result in a deficit of £107bn, which is why it was surprising that then Chancellor Kwasi Kwarteng decided to announce unfunded tax cuts amounting to £45bn a year by 2026/27. Although Kwarteng was hoping his planned tax cuts would help stimulate the economy, if they hadn’t then the deficit could have risen to more than £150bn, an unsustainable level that caused financial markets to take fright – even if they and we didn’t have the official numbers at that point.

Reversals to the mini-Budget followed as Chancellor Jeremy Hunt and Prime Minister Rishi Sunak attempted to reassure markets of their fiscal credibility, with £43bn in tax and spending changes to plug some of the gap. These comprise tax rises amounting to around £23bn a year (more than offsetting the £16bn of tax cuts retained from the mini-Budget), together with £20bn in lower levels of public spending than previously planned.

Together the forecast changes and government decisions give rise to a forecast deficit of £80bn in 2026/27, significantly higher than previously forecast. This is not a comfortable place for the public finances, with the Chancellor having to abandon the government’s previous commitment to achieving a current budget surplus in addition to, as expected, deferring the point at which he expects to see the underlying debt-to-GDP ratio start to fall from three to five years into the future.

Both tax and spending measures primarily involve fiscal drag, freezing tax allowances so that more people are brought into paying tax or paying tax at higher rates, and severely constraining public spending. Although it might be theoretically possible to hold the line on both tax and spending constraint for the next five years, there are likely to be some adjustments needed in the Spring Budget as pressures on public services mount, while the most difficult decisions have been postponed until after the next general election.