Borrowing to fund the deficit in the first four months of the financial year of £60bn was in line with expectations.

The monthly public sector finances release for July 2025 published by the Office for National Statistics (ONS) on 21 August reported a provisional shortfall between receipts and total public spending of £60bn for the four months ended 31 July 2025. This is in line with budget and £7bn more than in the same period last year.

Martin Wheatcroft, External Adviser on Public Finances to ICAEW, says: “This month’s ‘not bad’ result may provide a small amount of relief to a Chancellor under significant pressure.

“The monthly deficit for July was slightly better than expected, while the cumulative result for the first third of the financial year was almost exactly in line with the Office for Budget Responsibility’s prediction at the time of the Spring Statement 2025.

“Unfortunately, this does not change the dismal outlook for the public finances and the rising costs of public services, welfare provision and debt interest that means the Chancellor is again having to work out how she can ask Parliament to authorise higher levels of taxation.”

Month of July 2025

Receipts of £108.8bn in July 2025 were £9.2bn or 9% higher than in July 2024 and also higher than the £92.6bn average for the first three months of the financial year, principally as a result of a boost from income tax self-assessment collections in the month.

Meanwhile, current spending including depreciation of £105.5bn in July was £6.0bn or 6% more than in the same month a year previously. This was slightly lower than the £108.0bn monthly average incurred during April to June 2025.

The result was a current budget surplus for the month of £3.3bn, a £3.2bn improvement over the current budget surplus of £0.1bn in the same month last year.

Net investment of £4.4bn in July 2025 was £0.9bn more than the £3.5bn incurred in July 2024 and slightly higher than the £4.2bn average incurred during the three months to June 2025.

The provisional fiscal deficit for July 2025 was therefore £1.1bn, £1.0bn less than the £2.1bn budget for the month and a £2.3bn improvement over the £3.4bn deficit in July 2024.

Four months to July 2025

Table 1 highlights how year-to-date receipts of £387bn were up 7% on last year’s equivalents, with income tax receipts up 8% from a combination of inflation and fiscal drag from frozen tax allowances, and national insurance receipts up 19% as a consequence of the increase in employer national insurance that was implemented in April 2025.

Meanwhile, the 8% increase over last year in current spending including depreciation to £430bn in the first four months to July 2025 was primarily as a consequence of public sector pay rises, higher supplier costs, and the uprating of welfare benefits.

This included a £6bn or 13% increase in debt interest to £53bn, which comprised a £5bn increase in indexation on inflation-linked debt as inflation resurged and a £1bn increase in interest on variable and fixed-interest debt. The latter was primarily the result of a higher level of debt compared with a year ago partially offset by a lower Bank of England base rate.

The resulting current budget deficit of £43bn to July 2025 was 16% higher than for the same four months last year.

Net investment of £17bn in the first four months of 2025/26 was £1bn or 6% higher than the same period last year. Capital expenditure of £30bn was up by £1bn and capital transfers (capital grants, research and development funding, and student loan write-offs) of £11bn were up by £2bn, less depreciation of £24bn that was up by £2bn compared with the same four month period a year prior.

The consequence is a provisional deficit for the first third of the 2025/26 financial year of £60bn, which is £7bn or 13% more than in the same four month period last year. Despite being almost exactly in line with budget (only £0.1bn higher) this is the third-highest April-to-July deficit since monthly records began in 1993 (after 2020/21 and 2021/22 during the pandemic).

Table 1: Summary receipts and spending

| 4 months to July | 2025/26 £bn | 2024/25 £bn | Change % |

| Income tax | 100 | 93 | +8% |

| VAT | 70 | 67 | +4% |

| National insurance | 64 | 54 | +19% |

| Corporation tax | 35 | 32 | +9% |

| Other taxes | 76 | 74 | +3% |

| Other receipts | 42 | 41 | +2% |

| Current receipts | 387 | 361 | +7% |

| Public services | (239) | (221) | +8% |

| Welfare | (103) | (97) | +6% |

| Subsidies | (11) | (11) | – |

| Debt interest | (53) | (47) | +13% |

| Depreciation | (24) | (22) | +9% |

| Current spending | (430) | (398) | +8% |

| Current deficit | (43) | (37) | +16% |

| Net investment | (17) | (16) | +6% |

| Deficit | (60) | (53) | +13% |

Borrowing and debt

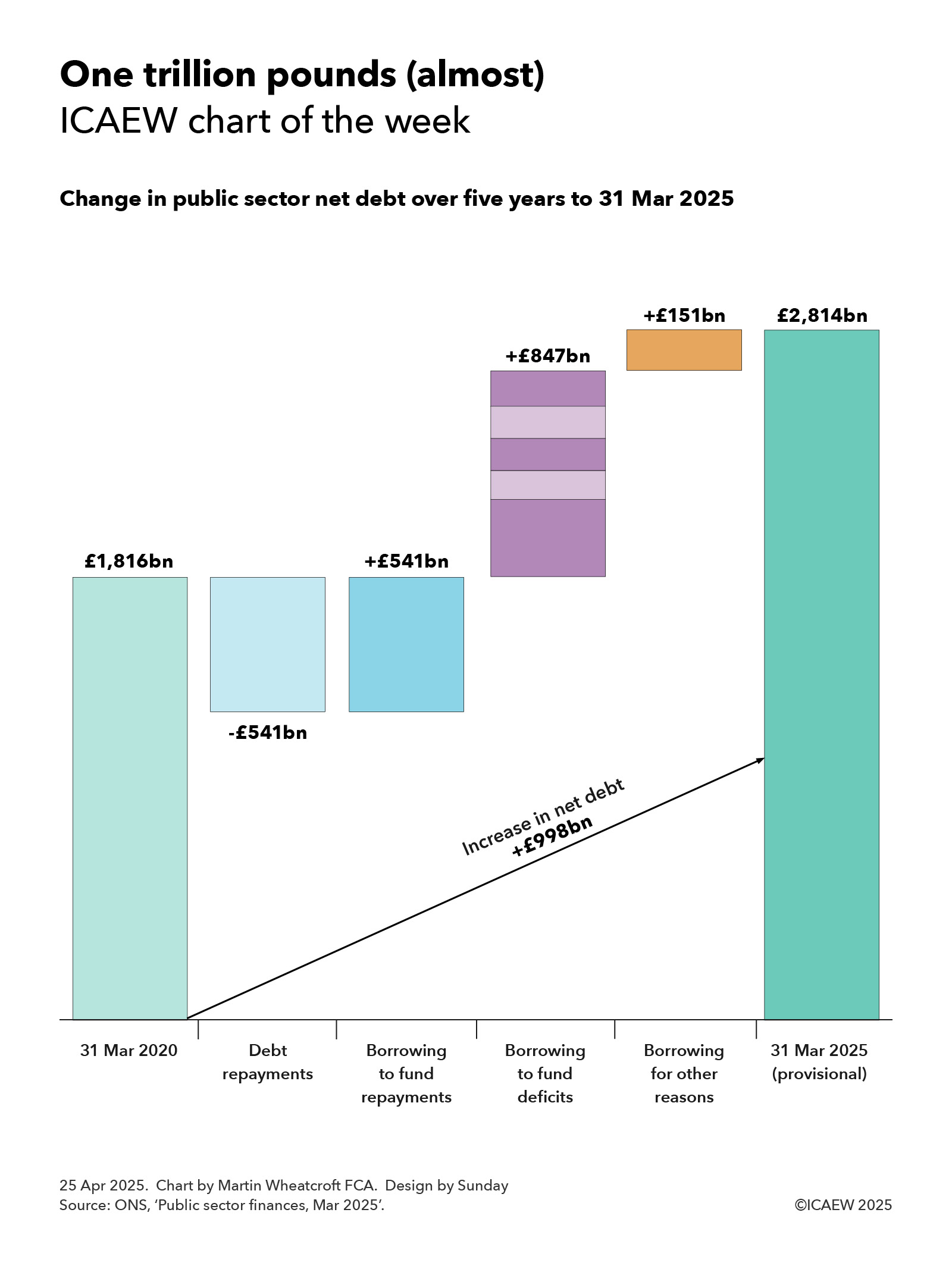

Table 2 summarises how the government borrowed £81bn in the first third of the financial year to take public sector net debt to a provisional £2,891bn on 31 July 2025. This comprised £60bn in public sector net borrowing (PSNB) to fund the deficit and £21bn to fund government lending activities and working capital movements.

The table also illustrates how the debt to GDP ratio increased from 94.8% of GDP at the start of the financial year to 96.1% on 31 July 2025, with the incremental borrowing partly offset by the ‘inflating away’ effect of inflation and economic growth adding to GDP, the denominator in the net debt to GDP ratio.

Table 2: Public sector net debt and net debt/GDP

| 4 months to July | 2025/26 £bn | 2024/25 £bn |

| PSNB | 60 | 53 |

| Other borrowing | 21 | (1) |

| Net change | 81 | 52 |

| Opening net debt | 2,810 | 2,686 |

| Closing net debt | 2,891 | 2,738 |

| PSNB/GDP | 2.1% | 1.9% |

| Other/GDP | 0.7% | – |

| Inflating away | (1.5%) | (1.9%) |

| Net change | 1.3% | – |

| Opening net debt/GDP | 94.8% | 95.6% |

| Closing net debt/GDP | 96.1% | 95.6% |

Public sector net debt on 31 July 2025 of £2,891bn comprised gross debt of £3,309bn less cash and other liquid financial assets of £418bn.

Public sector net financial liabilities were £2,525bn, comprising net debt of £2,891bn plus other financial liabilities of £707bn less illiquid financial assets of £1,073bn. Public sector negative net worth was £899bn, being net financial liabilities of £2,525bn less non-financial assets of £1,626bn.

Revisions

Caution is needed with respect to the numbers published by the ONS, which are repeatedly revised as estimates are refined and gaps in the underlying data are filled. This includes local government, where the numbers are only updated in arrears and are based on budget or high-level estimates in the absence of monthly data collection.

The latest release saw the ONS revise the previously reported deficit for the three months to June 2025 up by £1bn. The ONS also revised up its estimate of GDP in the first quarter of the financial year, resulting in a 0.4 reduction in the opening debt to GDP ratio on 1 April 2025 from 95.2% to 94.8% and the debt to GDP ratio for 30 June 2025 from 96.2% to 95.8%.