The section in which Martin was quoted reads as follows:

Martin Wheatcroft FCA, an external adviser on public finances to ICAEW, says it is not just badly run councils – that either speculated and lost or mismanaged funds – that now face the distinct possibility of financial failure: “Many ‘normal’ local authorities are now looking vulnerable too, as they struggle to balance their budgets in the face of rising demand, rising costs and constrained funding.”

In particular, Wheatcroft says adult social care is a significant challenge for many local authorities, as an ageing population sees demand increasing each year as the number of pensioners grows. Meanwhile, the knock-on impact of the minimum wage increase of 9.8% from April will further add to the challenges facing councils in the coming financial year.

“With local authority core funding only going up 6.5% in the coming financial year, local authorities are having to look for further cuts in other already ‘cut to the bone’ public services to try and balance their books,” Wheatcroft adds.

Last month, the Department for Levelling Up, Housing and Communities released a call for views on greater capital flexibilities that would allow councils to either use capital receipts to fund operational expenditure or to treat some operational expenditure as if it were capital, without the requirement to approach the government.

The intention is to encourage local authorities to invest in ways that reduce the cost of service delivery and provide more local levers to manage financial resources. The consultation is open until the end of January.

Under the current rules, councils are restricted from using money received from asset sales or from borrowing to fund operating costs due to capital receipts being considered a ‘one-off‘, while borrowing creates a liability that has to be repaid.

Wheatcroft adds: “The government’s announcement of greater capital flexibilities may help stave off some of the problems for a while but is likely to further weaken local authority balance sheets in doing so.”

Latest public sector finance numbers reveal a challenging fiscal backdrop for both government and opposition ahead of a general election.

The monthly public sector finances for November 2023 released by the Office for National Statistics (ONS) on Thursday 21 December 2023 reported a provisional deficit for the month of £14bn and revised the year-to-date deficit up by £4bn, bringing the cumulative deficit for the first two-thirds of the financial year to £116bn, £24bn more than in the same eight-month period last year.

Alison Ring OBE FCA, ICAEW Director for Public Sector and Taxation, said: “These numbers confirm that the government’s financial difficulties are continuing to mount, with the shortfall between income and public spending reaching an unsustainable £116bn for the first two-thirds of the financial year, surpassing the £100bn milestone and providing a challenging fiscal backdrop for both the government and the opposition ahead of a general election.

“While the Prime Minister and the Chancellor continue to search for cost savings to free up capacity for further pre-election tax cuts, the opposition will be concerned about the fiscal legacy it would inherit if it were to take power.

“The deteriorating state of the UK’s public services is a big concern for all politicians given that it implies a need for substantial tax rises after the general election, irrespective of who wins.”

Month of November 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the month of November 2023 was £14bn, made up of tax and other receipts of £86bn less total managed expenditure of £100bn, up 5% and 3% respectively compared with November 2022.

This was the fourth highest November deficit on record since monthly records began in 1997, following monthly deficits of £15bn, £22bn and £15bn in November 2010, 2020, and 2022 respectively.

Public sector net debt as of 30 November 2023 was £2,671bn or 97.5% of GDP, up £30bn during the month and £132bn higher than at the start of the financial year.

Eight months to November 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the first two thirds of the financial year to November 2023 was £116bn, £24bn more than the £92bn deficit reported for the first eight months of 2022/23. This reflected a year-to-date shortfall between tax and other receipts of £682bn and total managed expenditure of £798bn, up 5% and 8% respectively compared with April to November 2022.

Inflation benefited tax receipts for the first eight months compared with the same period in the previous year, with income tax up 10% to £156bn and VAT up 8% to £134bn. Corporation tax receipts were up 10% to £62bn, partly reflecting the increase in the corporation tax rate from 19% to 25% from 1 April 2023, while national insurance receipts were down by 3% to £114bn because of the abolition of the short-lived health and social care levy last year. Stamp duty on properties was down by 27% to £9bn and the total for all other taxes was up just 3% to £132bn, much less than inflation, as economic activity slowed. Non-tax receipts were up 11% to £75bn, primarily driven by higher investment income.

Total managed expenditure of £798bn in the eight months to November 2023 can be analysed between current expenditure excluding interest of £676bn, up £41bn or 6% over the same period in the previous year, interest of £90bn, up £7bn or 8%, and net investment of £32bn, up £10bn or 45%.

The increase of £41bn in current expenditure excluding interest was driven by a £21bn increase in pension and other welfare benefits (including cost-of-living payments), £14bn in higher central government pay and £7bn in additional central government procurement spending, less £1bn in net other changes.

The rise in interest costs for the eight months of £7bn to £90bn comprises a £20bn or 43% increase to £67bn for interest not linked to inflation as the Bank of England base rate rose, partially offset by an £13bn or 37% fall to £23bn for interest accrued on index-linked debt from lower inflation than last year.

The £10bn increase in net investment spending to £32bn in the first eight months of the current year reflects high construction cost inflation amongst other factors that saw a £13bn or 21% increase in gross investment to £75bn, less a £3bn or 8% increase in depreciation to £43bn.

The cumulative deficit of £116bn for the first two-thirds of the financial year is £8bn below the Office for Budget Responsibility (OBR)’s official forecast of £124bn for the full financial year as compiled in November 2023 for the Autumn Statement. The deficit for the last third of the financial year is normally much smaller than for the first two-thirds because of self assessment tax returns arriving in January that boost tax receipts.

Balance sheet metrics

Public sector net debt was £2,671bn at the end of November 2023, equivalent to 97.5% of GDP.

The debt movement since the start of the financial year was £131bn, comprising borrowing to fund the deficit for the eight months of £116bn plus £15bn in net cash outflows to fund lending to students, businesses and others net of loan repayments and working capital movements.

Public sector net debt is £856bn more than the £1,815bn reported for 31 March 2020 at the start of the pandemic and £2,133bn more than the £538bn number as of 31 March 2007 before the financial crisis, reflecting the huge sums borrowed over the last couple of decades.

Public sector net worth, the new balance sheet metric launched by the ONS this year, was -£715bn on 30 November 2023, comprising £1,565bn in non-financial assets and £1,054bn in non-liquid financial assets minus £2,671bn of net debt (£303bn liquid financial assets – £2,974bn public sector gross debt) and other liabilities of £663bn. This is a £100bn deterioration from the -£615bn reported for 31 March 2023.

Revisions

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The latest release saw the ONS revise the reported deficit for the seven months to October 2023 up by £4bn from £98bn to £102bn as estimates of tax receipts and expenditure were updated for better data, while the debt to GDP ratio at the end of October 2023 was revised down by 1.2 percentage points from 97.8% to 96.6% as a consequence of updated estimates of GDP.

The ONS also revised up its estimates for the deficit for the financial years to March 2023 and 2022 respectively, by £3bn to £131bn for 2022/23 and by £2bn to £124bn for 2021/22.

My chart for ICAEW this week takes a look at how UK public debt has exploded since the financial crisis to more than quintuple from £0.6trn in March 2008 to a projected £3.1trn in March 2029.

As illustrated by our chart this week, the sums borrowed by the government since the financial crisis of a decade and half ago have been truly astonishing.

In March 2008, the official measure of net debt for the UK public sector was less than £0.6trn. During the financial crisis, government borrowing totalled £0.7trn over a four-year period, causing public sector net debt to more than double to £1.3bn in March 2012.

The eight austerity years saw government cut spending on public services to a significant degree but still borrow a further £0.5trn to see net debt reach £1.8trn in March 2020 – arguably not mending the roof while the sun was shining. This was then followed by an exceptional amount of borrowing during four years of pandemic and energy crisis (including the current financial year) that is expected to see net debt increase by a total of £0.9trn to reach £2.7trn in March 2024.

The Autumn Statement 2023 on Wednesday 22 November saw the Chancellor set out his latest plan for the UK public finances over the next five financial years. This includes a further £0.4trn of borrowing, with public sector net debt projected to amount to £3.1trn in March 2029 – more than quintuple the net amount owed by the UK state 21 years earlier in March 2008.

This assumes that the government can stick to its borrowing plans – many commentators have suggested that planned cuts in spending on public services are unrealistic, meaning more borrowing if taxes are not to rise.

The £2.5trn increase in debt between 2008 and 2029 comprises £2.2trn in borrowing to fund 21 years of deficits (the annual shortfall between receipts and spending) and £0.3trn in other borrowing to fund government lending (such as student loans) and working capital requirements.

As a share of the economy, the increase is less dramatic but still significant – rising from a net debt to GDP ratio of 35.6% in March 2008, to 74.3% in March 2012, to 85.2% in March 2020, to an anticipated 97.9% in March 2024. However, the good news is that net debt / GDP is expected to fall to 94.1% in March 2029 as inflation and economic growth offset the additional borrowing.

The worry for this (or any alternative) government is that while borrowing levels in the OBR’s forecast spreadsheet for the next five years appear manageable and are (just) within the current fiscal rules, the numbers assume that we don’t enter another recession or other economic crisis in that time. Otherwise, we could see debt exploding again.

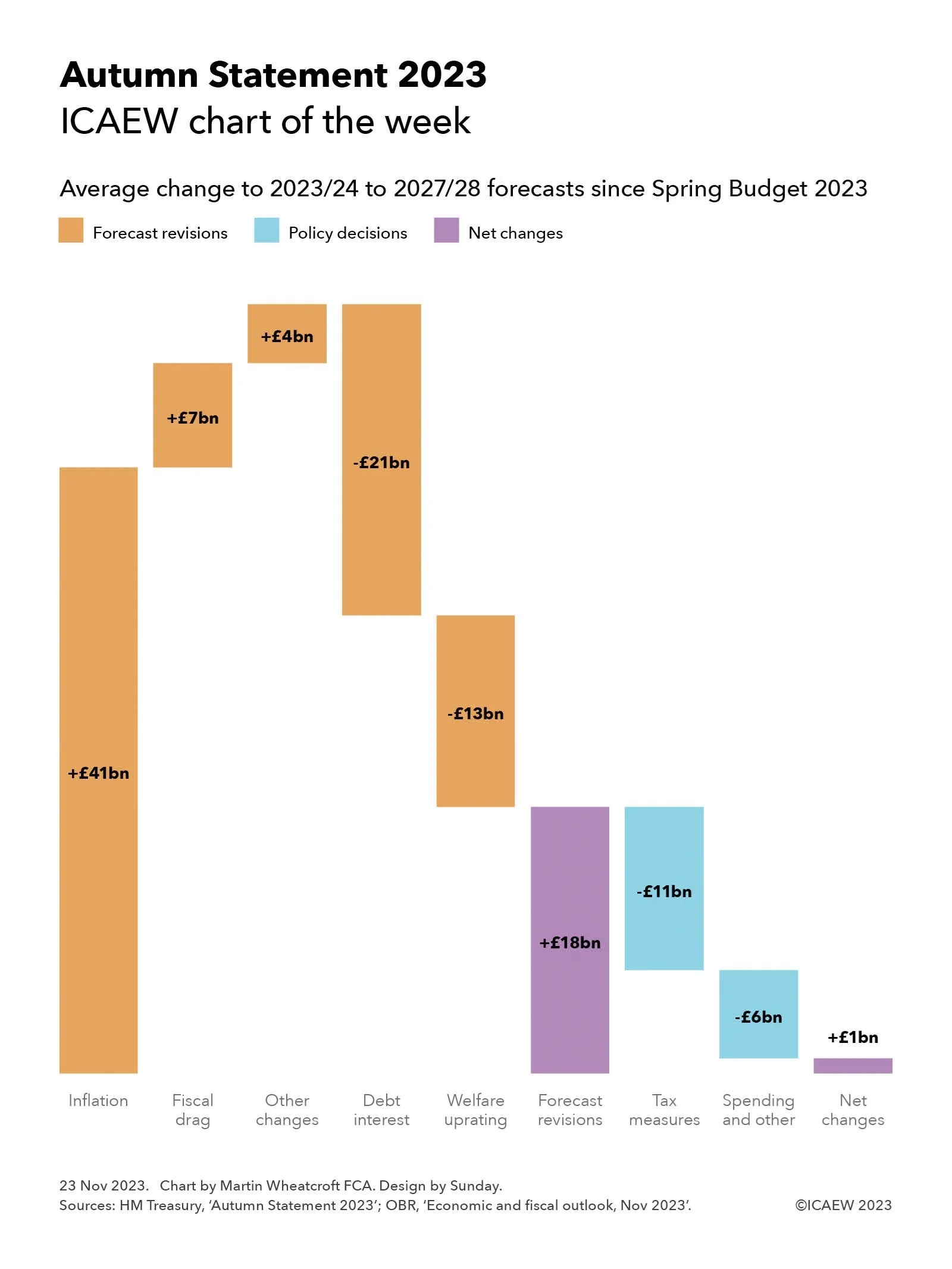

My chart for ICAEW this week illustrates how Chancellor Jeremy Hunt used almost all of the available upside from inflation and fiscal drag to fund his tax measures and a series of business growth initiatives.

The Autumn Statement 2023 on Wednesday 22 November featured a surprise tax cut to national insurance and a perhaps less surprising decision to make full expensing of business capital expenditure permanent.

As my chart illustrates, the forecasts for the deficit over the next five years benefited by £41bn a year on average in higher receipts from inflation, £7bn a year on average in additional ‘fiscal drag’ as higher inflation erodes the value of frozen tax allowances more quickly, and a net £4bn in other upward forecast revisions. These improvements to the forecasts were offset by an average of £21bn a year in higher debt interest and £13bn from the expected inflation-driven uprating of the state pension and welfare benefits, to arrive at a net improvement of £18bn a year on average over the five financial years from 2023/24 to 2027/28 before policy decisions.

In theory, these upward forecast revisions should be absorbed by more spending on public services as higher inflation feeds through into salaries and procurement costs. However, the Chancellor has chosen to (in effect) sharply cut public spending and use almost all of the upward revisions to fund tax measures and business growth initiatives instead. These amounted to £11bn a year on average in tax changes and £6bn a year on average in spending increases and other changes to reduce the net impact to just £1bn a year on average over the five-year period.

The resulting net change of £1bn on average in forecasts for the deficit is to reduce the forecast deficit by £8bn for the current year (from £132bn to £124bn) and by £1bn for 2024/25 (to £85bn), with no net change in 2025/26 (at £77bn), an increase of £5bn in 2027/28 (to £68bn), and no net change for 2027/28 (at £49bn).

The main tax changes announced were the cuts in national insurance for employees by 2 percentage points from 12% to 10% and by 1 percentage point for the self-employed from 9% to 8%, reducing tax receipts by an average of £9bn over five years. This is combined with the effect of making full expensing permanent of £4bn – this change mainly affects the later years of the forecast (£11bn in 2027/28), although ironically the average is a better proxy for the long-term cost of this change, which the OBR estimates is around £3bn a year.

Other tax changes offset this to a small extent.

Spending and other changes of £6bn a year on average comprise incremental spending of £7bn a year plus £2bn higher debt interest to fund that spending, less £3bn in positive economic effects from that spending and from the tax measures above.

Although the cumulative fiscal deficit over five years has been revised down by £4bn, the OBR has revised its forecast for public sector net debt as of 31 March 2028 up by £94bn from to £3,004bn. This principally reflects changes in the planned profile of quantitative tightening and higher lending to students and businesses.

The big gamble the Chancellor appears to be making by choosing to opt for tax cuts now is that the OBR and Bank of England’s pessimistic forecasts for the economy are not realised – enabling him to find extra money in future fiscal events to cover the effect of inflation on public service spending. Otherwise, while it may be possible to cut public spending by as much as the Autumn Statement suggests, it is difficult to see how he can do so without a further deterioration in the quality of public services given he is not providing any additional investment in technology, people and process transformation to deliver sustainable efficiency gains.

Monthly public sector finances for October saw spending continue to exceed receipts by a large margin, even if by less than was predicted earlier in the year.

The Office for National Statistics (ONS) released the month public sector finances for October on Tuesday 21 November 2023. It reported a provisional deficit for the month of October of £15bn, bringing the cumulative deficit for the first seven months of the year to £98bn, £22bn more than in the same period last year.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “Although it is positive that the cumulative deficit to October of £98bn is less than the £115bn predicted by the OBR, cash going out continues to exceed cash coming in by a very large margin. Public sector net debt has now exceeded £2.6 trillion for the first time, which is a staggering new record.

“Tomorrow’s Autumn Statement will see the OBR revise and roll forward its forecast, giving the Chancellor so-called headroom to cut taxes or increase spending. But in reality there is no headroom when the public finances continue to be on an unsustainable path without a long-term fiscal strategy to fix them.”

Month of October 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the month of October 2023 was £15bn, made up of tax and other receipts of £85bn less total managed expenditure of £100bn, up 3% and 6% respectively compared with October 2022.

This was the second highest October deficit on record since monthly records began in 1993, following a monthly deficit of £18bn in October 2020 at the height of the pandemic.

Public sector net debt as of 31 October 2023 was £2,644bn or 97.8% of GDP, the first time it has exceeded £2.6trn – only eight months after it first reached £2.5trn.

Seven months to October 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the seven months to October 2023 was £98bn, £22bn more than the £76bn deficit reported for the first seven months of 2022/23. This reflected a widening gap between tax and other receipts for the seven months of £595bn and total managed expenditure of £693bn, up 5% and 8% respectively compared with April to October 2022.

Inflation benefited tax receipts for the first seven months compared with the first half of the previous year, with income tax up 10% to £137bn and VAT up 9% to £117bn. Corporation tax receipts were up 12% to £55bn, partly reflecting the increase in the corporation tax rate from 19% to 25% from 1 April 2023, while national insurance receipts were down by 4% to £99bn because of the abolition of the short-lived health and social care levy last year. Stamp duty on properties was down by 27% to £8bn and the total for all other taxes was up just 3% to £115bn, much less than inflation as economic activity slowed. Non-tax receipts were up 10% to £63bn, primarily driven by higher investment income.

Total managed expenditure of £693bn in the seven months to October 2023 can be analysed between current expenditure excluding interest of £587bn, up £39bn or 7% over the same period in the previous year, interest of £76bn, up £4bn or 5%, and net investment of £30bn, up £9bn or 44%.

The increase of £39bn in current expenditure excluding interest was driven by a £20bn increase in pension and other welfare (including cost-of-living payments), £12bn in higher central government pay, £6bn in additional central government procurement spending, plus £1bn in net other changes.

The rise in interest costs for the seven months of £4bn to £76bn comprises a £18bn or 53% increase to £52bn for interest not linked to inflation as the Bank of England base rate rose, mostly offset by an £14bn or 37% fall to £24bn for interest accrued on index-linked debt from lower inflation than last year.The £9bn increase in net investment spending to £30bn in the first seven months of the current year reflects high construction cost inflation amongst other factors that saw a £11bn or 17% increase in gross investment to £65bn, less a £2bn or 6% increase in depreciation to £35bn.

The cumulative deficit of £98bn is £17bn lower than the Office for Budget Responsibility (OBR)’s official forecast of £115bn for the first seven months of 2023/24 as compiled in March 2023. The OBR is expected to revise its forecast for the full year deficit down from £132bn in tomorrow’s Autumn Statement, but it is still on track to be more than double the £50bn projection for 2023/24 set out in the official forecast from a year earlier (March 2022).

Balance sheet metrics

Public sector net debt was £2,644bn at the end of October 2023, equivalent to 97.8% of GDP.

The debt movement since the start of the financial year was £105bn, comprising borrowing to fund the deficit for the seven months of £98bn plus £7bn in net cash outflows to fund lending to students, businesses and others net of loan repayments together with working capital movements.

Public sector net debt is £829bn more than the £1,815bn reported for 31 March 2020 at the start of the pandemic and £2,106bn more than the £538bn number as of 31 March 2007 before the financial crisis, reflecting the huge sums borrowed over the last couple of decades.

Public sector net worth, the new balance sheet metric launched by the ONS this year, was -£716bn on 31 October 2023, comprising £1,565bn in non-financial assets, £1,029bn in non-liquid financial assets, £2,644bn of net debt (£305bn in liquid financial assets less public sector gross debt of £2,949bn) and other liabilities of £666bn. This is a £102bn deterioration from the -£614bn reported for 31 March 2023.

Revisions

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The latest release saw the ONS revise the reported deficit for the six months to September 2023 up by £1.7bn as estimates of tax receipts and expenditure were updated for better data, while the debt to GDP ratio at the end of September 2023 was revised down by 1.4 percentage points from 97.8% to 96.4% as a consequence of updated estimates of GDP.

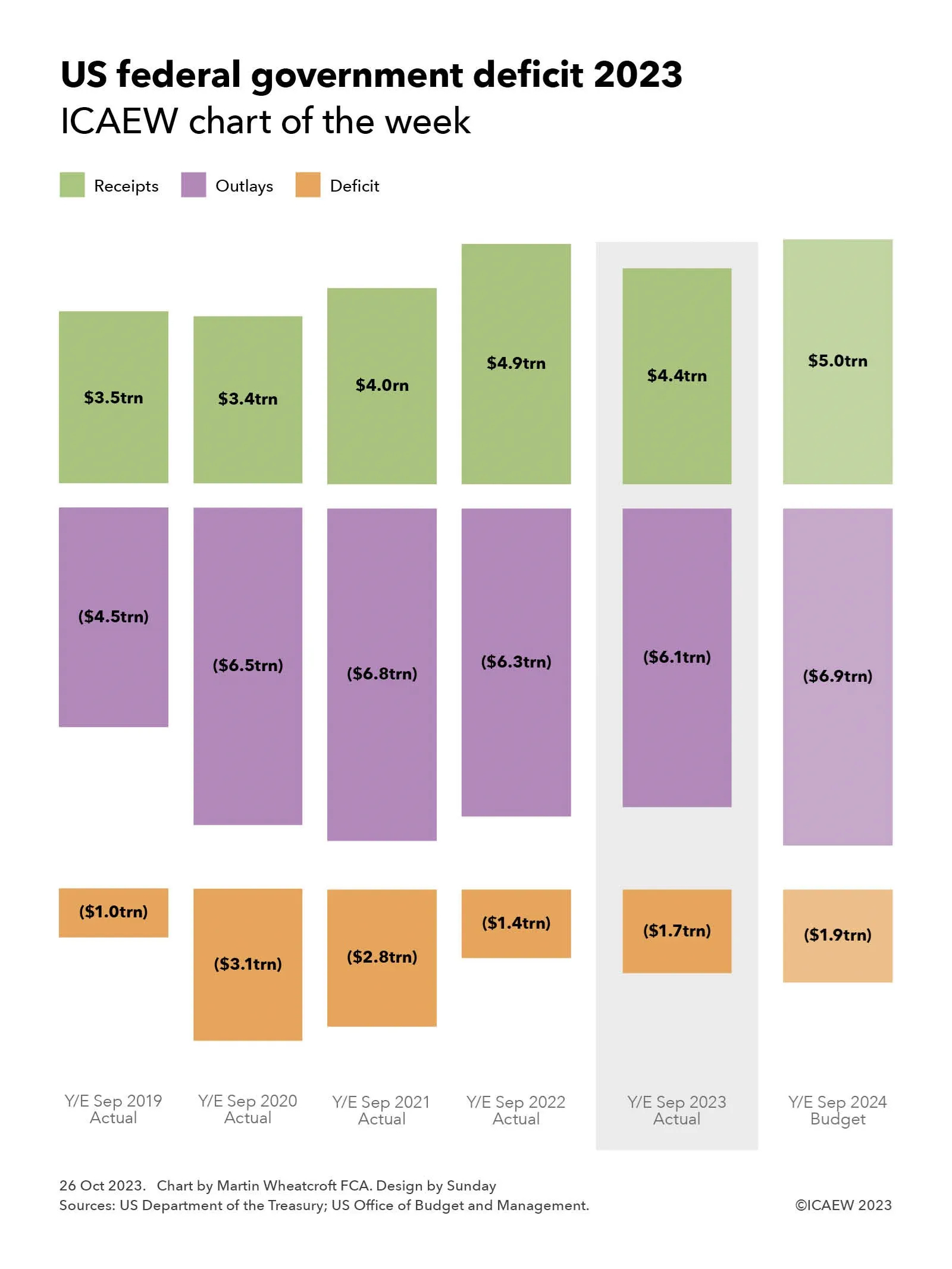

My chart this week looks at the federal deficit of $1.7trn reported by the US government for its recently completed financial year ended 30 September 2023.

The US Department of Treasury published on 20 October 2023 its final monthly treasury statement for the US government’s financial year ended 30 September 2023 (FY2023), enabling our chart this week to look at the actual numbers over the past five years and the budget for the new financial year that started on 1 October.

Our chart illustrates how the deficit increased significantly from the $1.0trn reported for FY2019 ($3.5trn receipts less $4.5trn outlays) to $3.1trn in FY2020 ($3.4trn-6.5trn) and $2.8trn in FY2021 ($4.0trn-$6.8trn) at the height of the pandemic, before falling to $1.4trn in FY2022 ($4.9trn-$6.3trn) as the US economy recovered. The deficit by $0.3trn increased to $1.7trn in FY2023 ($4.4trn-$6.1trn) and is budgeted to increase by a further $0.2trn to $1.9trn in FY2024 ($5.0trn forecast receipts-$6.9trn forecast outlays).

Not shown in the chart is the excess of financial liabilities over financial assets, which increased by $1.7trn from $22.3trn on 30 September 2022 to $24.0trn on 30 September 2023. This differs from ‘debt held by the public’ (the headline measure of federal debt), which increased by $2.0trn from $24.3trn to $26.3trn, more than the federal deficit because of movements in other financial assets and liabilities.

Receipts in FY2023 of $4,439bn comprised $2,176bn in individual income taxes, £1,614bn in social security and retirement contributions, $420bn in corporation income taxes, $80bn in customs duties, $76bn in excise taxes, £34bn in estate and gift taxes and $39bn in other receipts. Outlays for same period of $6,134bn comprised $1,737bn on health and Medicare, $1,354bn on social security, $821bn on defence, $774bn in welfare benefits, $659bn in interest, $302bn for veteran services and benefits, $127bn on transportation, $100bn on commerce, and $260bn on other outlays.

The latter includes the administration of justice, agriculture, community and regional development, education, training, employment and social services, energy, general government, general science, space and technology, international affairs, natural resources and environment, and undistributed offsetting receipts.

These amounts are different from the accruals-based US GAAP federal government financial statements for FY2023 that are expected to be published next April, which will show a much larger accounting loss than the federal deficit reported here. For example, the FY2022 net operating cost (ie accounting loss) of $4.2trn was $2.8trn higher than the federal deficit of $1.4trn for last year, of which the largest difference of $2.6trn related to accruals for federal employee and veteran benefits.

These amounts appear astronomical, especially to those of us living in smaller (and unfortunately) less prosperous countries than the 335m people who live in the US, with its estimated GDP of $26.3trn in FY2023 – equivalent to around $6,600 per person per month.

Federal receipts and outlays in FY2023 represented 17% and 23% of GDP respectively or on a per capita basis were approximately $1,105 and $1,525 per person per month. The federal deficit was therefore equivalent to 6% of GDP or $420 per person per month.

The excess of financial liabilities over financial assets and debt held by the public were 91% and 100% of GDP respectively, equivalent to an amount owed of around $71,500 or $78,500 per person, depending on which measure is used.

Deficit marginally better than had been expected according to the latest figures from the ONS, but costly public sector problems emerge.

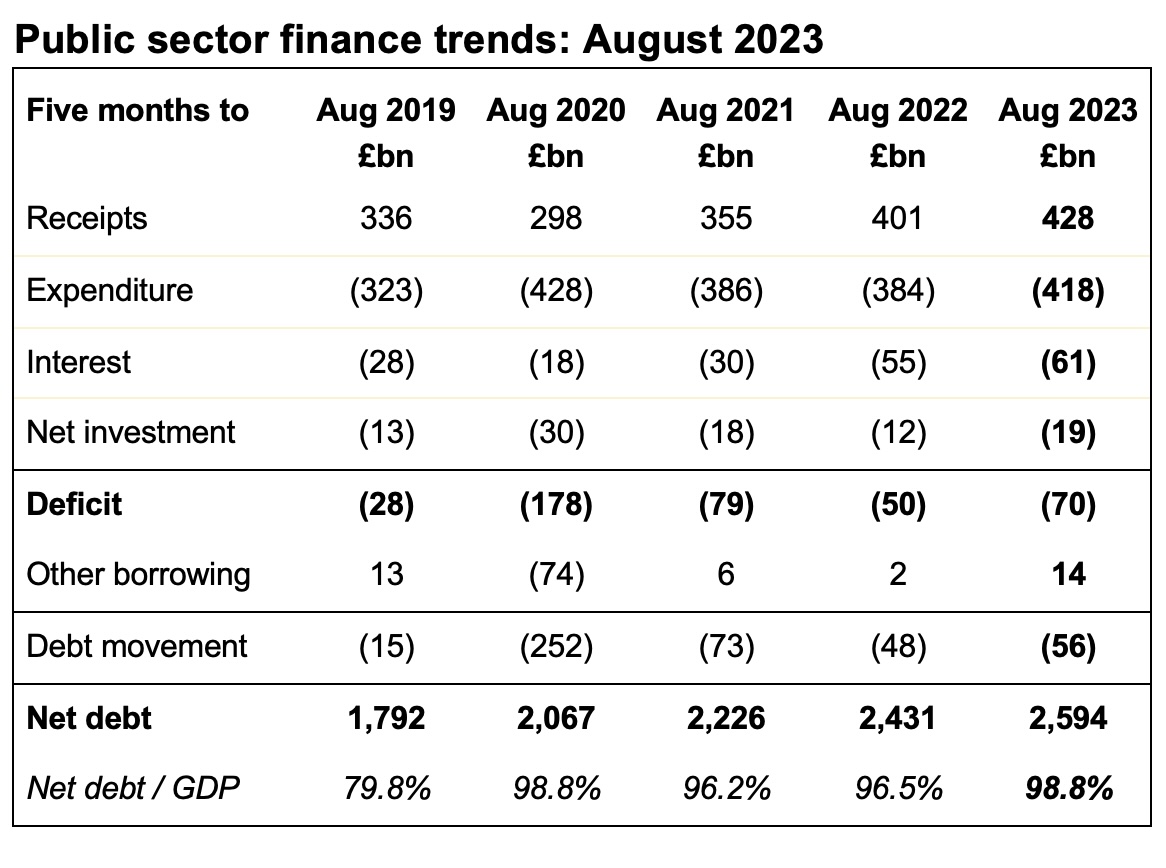

The monthly public sector finances for August 2023 were released by the Office for National Statistics (ONS) on Thursday 21 September 2023. These reported a provisional deficit for the fifth month of the 2023/24 financial year of £12bn, bringing the total deficit for the five months to £70bn, £19bn more than in the same period in the previous year.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “While August’s deficit was marginally better than expected, problems costly to the public sector continue to emerge, from crumbling concrete in public buildings to Birmingham Council’s recent bankruptcy, and are likely to weigh on the Chancellor’s mind as he considers November’s Autumn Statement.

“Both main parties are rightly cautious about making new public spending commitments in the current economic environment, including whether or not to extend the state pension triple lock into the next parliament. Whether they can hold this position as they enter into the party conference season remains to be seen.”

Month of August 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the month of August 2023 was just under £12bn, being tax and other receipts of £84bn less total managed expenditure of £96bn – up 5% and 8% respectively compared with August 2022.

This was the fourth highest August deficit on record since monthly records began in 1993, following the deficits of £14bn in August 2021 and £24bn in August 2020 during the pandemic and £12bn in August 2009 during the financial crisis.

Five months to August 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the five months to August 2023 was £70bn, £20bn more than the £50bn deficit reported for the first five months of 2022/23. This reflected a widening gap between tax and other receipts for the five months of £428bn and total managed expenditure of £498bn, up 7% and 10% respectively compared with April to August 2022.

Inflation benefited tax receipts for the first five months compared with the previous year, with income tax and VAT receipts both up 12% to £104bn and £84bn respectively. However, corporation tax was only up 13% to £37bn despite the increase in the corporation tax rate from 19% to 25% from 1 April 2023, and national insurance receipts were down by 3% to £71bn because of the abolition of the short-lived health and social care levy last year. Stamp duty on properties was down by £2bn or 29% to £6bn and the total for all other taxes was up just 3% to £82bn as economic activity slowed. Non-tax receipts were up 12% to £44bn, primarily driven by higher investment income.

Total managed expenditure of £428bn in the five months to August can be analysed between current expenditure excluding interest of £418bn (up £34bn or 9% over the same period in the previous year), interest of £61bn (up £6bn or 11%), and net investment of £19bn (up £7bn or 57%).

The increase of £34bn in current expenditure excluding interest compared with the prior year has been driven by a £14bn increase in benefit payments, £9bn in higher central government staff costs, £5bn in additional central government procurement spending and £5bn in energy support scheme costs, plus £1bn in net other changes.

The rise in interest costs of £6bn to £61bn reflects a £14bn increase in interest on non-inflation linked debt to £38bn as the Bank of England base rate rose, offset by an £8bn fall in the interest payable on index-linked debt to £23bn as inflation is running at a lower level than it was for the same period last year.

The £7bn increase in net investment spending to £15bn in the first five months of the current year reflects high construction cost inflation among other factors that saw an £8bn or 23% increase in gross investment to £44bn, less a £1bn increase in depreciation to £25bn.

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The latest release saw the ONS revise the reported deficit for the four months to July 2023 up by £2bn as estimates of tax receipts and expenditure were updated for better data, and it also reduced the reported deficit for the 2022/23 financial year by £1bn to £128bn for methodology changes in addition to new data.

The methodology changes also saw small revisions in the reported deficits for previous periods back to 1999, most notably reductions of £1bn to the deficits in 2019/20 and 2020/21 and an increase of £2bn in the reported deficit for 2021/22.

Balance sheet metrics

Public sector net debt was £2,594bn at the end of August 2023, equivalent to 98.8% of GDP.

The debt movement since the start of the financial year was £56bn, comprising borrowing to fund the deficit for the five months of £70bn less £14bn in net cash inflows as loan repayments and positive working capital movements exceeded cash outflows for lending to students, business and others.

Public sector net debt is £779bn or 43% higher than it was on 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic.

Public sector net worth, the new balance sheet metric launched by the Office for National Statistics this year, was -£618bn on 31 August 2023, comprising £1,604bn in non-financial assets, £1,038bn in non-liquid financial assets, £2,594bn of net debt (£339bn in liquid financial assets less public sector gross debt of £2,933bn) and other liabilities of £667bn. This is a £61bn deterioration from the -£557bn reported for 31 March 2023.

This new measure seeks to capture more assets and liabilities than the narrowly focused public sector net debt measure traditionally used to assess the financial position of the UK public sector. However, it excludes unfunded employee pension liabilities that amounted to over £2trn at 31 March 2021 according to the Whole of Government Accounts, although they are expected to be much lower today as discount rates have risen significantly since then.

Higher self-assessment tax receipts and end of energy support payments help improve what is otherwise a disappointing set of numbers.

The monthly public sector finances for July 2023 were released by the Office for National Statistics (ONS) on Tuesday 22 August 2023. These reported a provisional deficit for the fourth month of the 2023/24 financial year of £4bn, bringing the total deficit for the four months to £57bn, £14bn more than in the first third of the previous year.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “These numbers reflect a mixed set of results for the first four months of the financial year, as higher self assessment tax receipts and the end of energy price guarantee support payments led to an improved fiscal situation in July. But debt remains on track to hit £2.7trn by the end of the year, up from £1.8trn before the pandemic, adding to the scale of the challenge facing the government and taxpayers in repairing the public finances.

“Stubbornly high core inflation and the prospect of further interest rate rises will concern the Chancellor as he bears down on public spending in the hope of freeing up the money he needs to both pay for the state pension triple-lock and find room for pre-election tax cuts.”

Month of July 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the month of July 2023 was £4bn, being tax and other receipts of £93bn less total managed expenditure of £97bn, up 5% and 9% respectively compared with July 2022.

This was the fifth-highest July deficit on record since monthly records began in 1993, despite being a £3bn improvement over July 2022, driven by higher self assessment tax receipts and the end of payments under the energy price guarantee.

Four months to July 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the four months to July 2023 was £57bn, £14bn more than the £43bn deficit reported for the first third of the previous financial year (April to July 2022). This reflected a widening gap between tax and other receipts for the four months of £343bn and total managed expenditure of £400bn, up 7% and 10% respectively compared with April to July 2022.

Inflation benefited tax receipts for the four months, with income tax up 13% to £85bn and VAT up 9% to £65bn. The rise in corporation tax, up 17% to £30bn, reflected both inflation and the increase in the corporation tax rate to 25% from 1 April 2023. However, national insurance receipts were down by 3% to £57bn because of the abolition of the short-lived health and social care levy last year, while the total for all other taxes was down by 1% to £69bn as economic activity slowed. Other receipts were up 17% to £37bn, driven by higher investment income.

Total managed expenditure of £400bn in the four months to July can be analysed between current expenditure excluding interest of £334bn (up £26bn or 8% over the same period in the previous year), interest of £51bn (up £7bn or 16%), and net investment of £15bn (up £4bn or just over a third).

The increase of £26bn in current expenditure excluding interest compared with the prior year has been driven by £11bn from the uprating of benefit payments, £8bn in higher central government staff costs, £3bn in central government procurement and £5bn in energy support scheme costs, less £1bn in net other changes.

The rise in interest costs of £7bn to £51bn reflects a fall in the interest payable on index-linked debt of £6bn from £30bn to £24bn as inflation has moderated compared with the same period last year, combined with a £13bn increase in interest on non-inflation linked debt from £14bn to £27bn as the Bank of England base rate rose.

The £4bn increase in net investment spending to £15bn in the first four months of the current year reflects high construction cost inflation among other factors that saw a £5bn or 17% increase in gross investment to £35bn, less a £1bn increase in depreciation to £20bn.

Public sector finance trends: July 2023

Four months to

Jul 2019 (£bn)

Jul 2020 (£bn)

Jul 2021 (£bn)

Jul 2022 (£bn)

Jul 2023 (£bn)

Receipts

270

234

282

320

343

Expenditure

(259)

(348)

(310)

(308)

(334)

Interest

(24)

(15)

(23)

(44)

(51)

Net investment

(10)

(26)

(13)

(11)

(15)

Deficit

(23)

(155)

(64)

(43)

(57)

Other borrowing

4

(66)

(22)

5

10

Debt movement

(19)

(221)

(86)

(38)

(47)

Net debt

1,796

2,036

2,239

2,420

2,579

Net debt / GDP

80.1%

96.9%

97.7%

96.6%

98.5%

Source: ONS, ‘Public sector finances, July 2023’.

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled. The latest release saw the ONS revise the reported deficit for the three months to June 2023 down by £2bn as estimates of tax receipts and expenditure were updated for better data, as well as reduce the reported deficit for the 2022/23 financial year by £1bn from £132bn to £131bn for similar reasons. The ONS also revised its estimates of GDP for more recent economic data, resulting in a lower reported net debt / GDP ratio.

Balance sheet metrics

Public sector net debt was £2,579bn at the end of July 2023, equivalent to 98.5% of GDP.

The debt movement since the start of the financial year was £47bn, comprising borrowing to fund the deficit for the four months of £57bn plus £10bn in net cash inflows as loan repayments and positive working capital movements exceeded cash outflows for lending to students, business and others.

Public sector net debt is £764bn or 42% higher than it was on 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic.

Public sector net worth, the new balance sheet metric launched by the Office for National Statistics this year, was -£631bn on 31 July 2023, comprising £1,604bn in non-financial assets, £1,011bn in non-liquid financial assets and £336bn in liquid financial assets less public sector gross debt of £2,915bn and other liabilities of £667bn. This is a £54bn deterioration from the -£577bn reported for 31 March 2023.

This new measure seeks to capture more assets and liabilities than the narrowly focused public sector net debt measure traditionally used to assess the financial position of the UK public sector. However, it excludes unfunded employee pension liabilities that amounted to more than £2trn at 31 March 2021 according to the Whole of Government Accounts, although they are expected to be much lower today as discount rates have risen significantly since then.

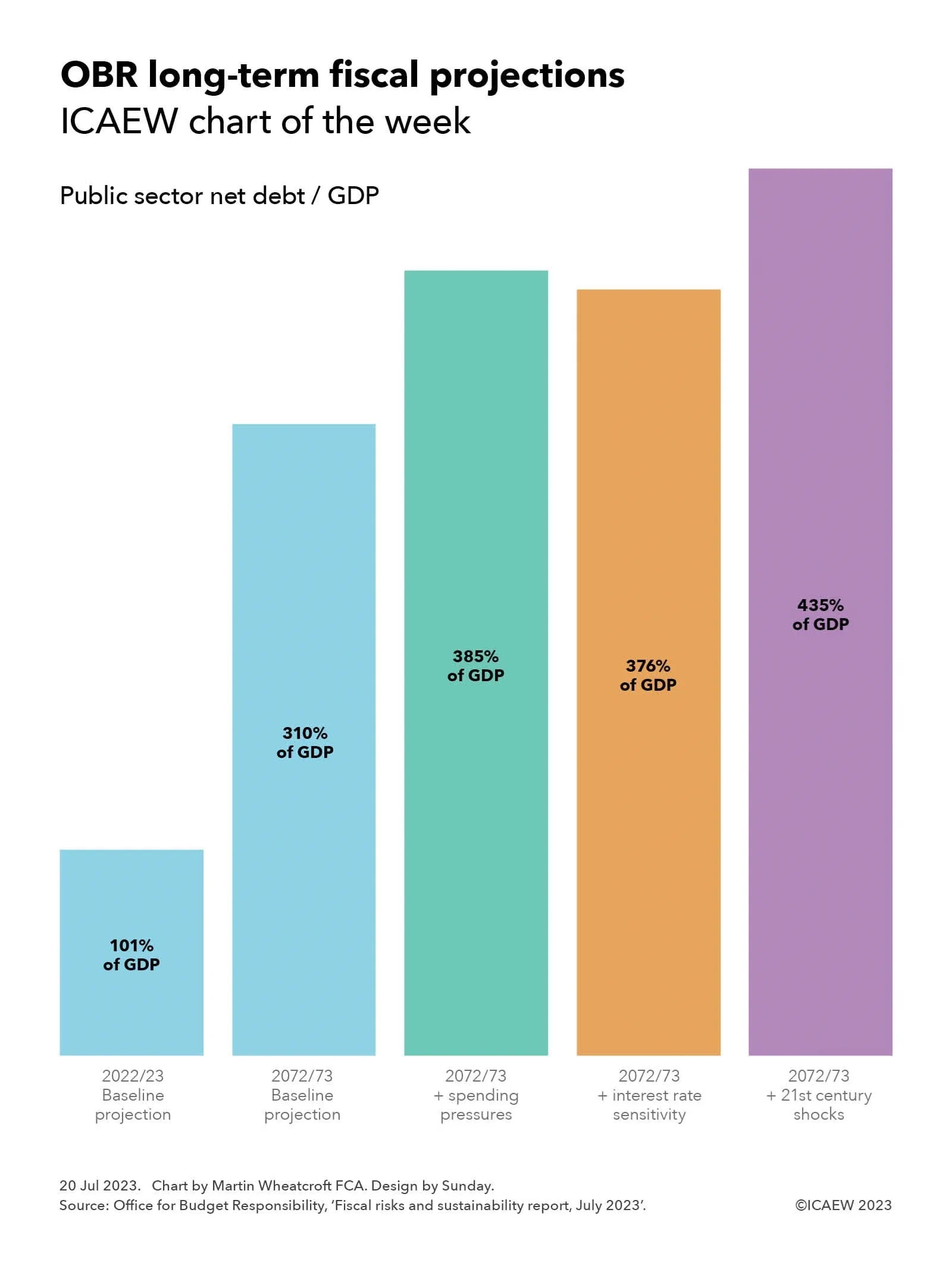

The OBR’s July 2023 fiscal risks and sustainability report indicates that, without higher taxes, public sector net debt as a share of GDP could triple or more over the next 50 years.

The Office for Budget Responsibility (OBR) published its latest fiscal risks and sustainability report on 13 July 2023, providing its analysis of the key risks confronting the UK public finances and long-term fiscal projections for the next 50 years.

This is a sobering report, suggesting that public sector net debt as a share of economic activity as measured by GDP could more than triple between March 2023 and March 2073 – and perhaps go even higher in certain circumstances. The OBR concludes that the public finances are on an unsustainable path.

As illustrated by this week’s chart, the OBR’s baseline projection suggests that the ratio of public sector net debt to GDP could rise from 101% of GDP in 2022/23 to 310% of GDP in 2072/73. The OBR also presented three alternate scenarios: the first is based on higher levels of spending, which could result in the ratio reaching 385% of GDP; one involves higher interest rates, where the ratio might reach 376% of GDP; and a further scenario assuming additional economic shocks, where the ratio might hit 435% of GDP.

The projections are based on the government’s current medium-term fiscal plans as set out in the March 2023 Spring Budget, extrapolated into the future based on existing trends. The starting point is the already high level of public debt that has built up over the past 15 years, together with the current government’s plan to cut spending on public services over the next five years.

The OBR has then overlayed its view of economic growth over the next half century and expected changes in patterns of public spending. This reflects a substantial rise in spending on pensions, health and social care as the proportion of the population in retirement rises, among other drivers that include the financial costs and benefits of delivering net zero. Other key assumptions relate to productivity, demographics (births, deaths and net migration), interest rates and inflation.

The one thing the OBR hasn’t been able to do is to include probable but not enacted tax changes in its projections, with increases in public spending assumed to be financed by higher levels of borrowing instead of the tax rises that future governments are in reality going to opt for.

The projections therefore reflect borrowing that compounds over time to result in some very large headline debt numbers in March 2073, rather than the 1.5% of GDP rise in the tax burden each decade that would, according to the OBR, maintain the debt to GDP ratio at close to its current level.

The fiscal projections calculated by the OBR highlight just how difficult a position the UK’s public finances are in and the major fiscal challenges that will face the incoming government – whoever that may be – after the next general election.

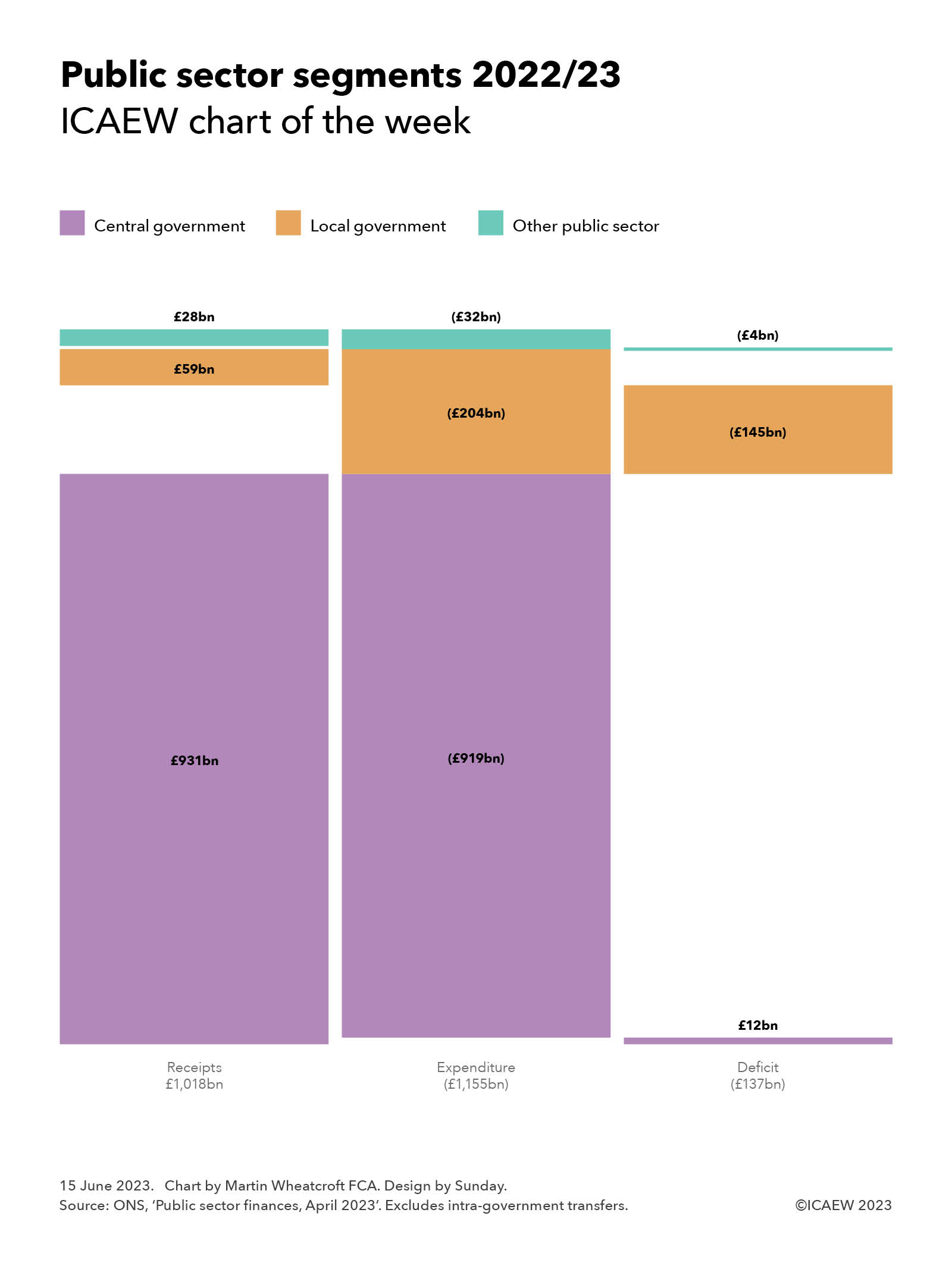

Our chart this week illustrates just how centralised the UK is by looking at the disparity between receipts and expenditure between central and local government.

Most people living in the UK would be surprised to discover just how big a gap there is between the council taxes and other income received by local councils, police and fire authorities, and the amount that they spend on public services.

Our chart of the week illustrates this disparity by looking at public sector segments in 2022/23 and how receipts and expenditure match up, before taking account of intra-government transfers.

Fiscal reporting in the National Accounts is broken down into five segments, of which the two largest are central government and local government. The former includes UK government departments, the devolved administrations in Scotland, Wales and Northern Ireland, and several hundred government agencies and other public bodies. Local government principally consists of local authorities across the UK, the Greater London Authority and regional combined authorities in England, police and fire authorities in England and Wales, and local public transport bodies (the largest of which is Transport for London). The other three segments are public corporations (comprising publicly owned businesses plus social housing), funded pension schemes (mostly local authority schemes as central government schemes are generally unfunded), and the Bank of England.

The latest provisional numbers for the financial year ended 31 March 2023 reported that the UK public sector generated £1,018bn in receipts and incurred expenditure of £1,155bn, giving rise to a deficit of £137bn – a shortfall that has been funded by central government borrowing.

Central government raised £931bn in 2022/23 and spent £919bn, a net £12bn surplus before intra-government transfers. Local government received £59bn and spent £204bn, a shortfall of £145bn. And the three remaining fiscal segments together generated £28bn in receipts, and recorded £32bn in expenditure, a net shortfall of £4bn.

By excluding transfers in this way, the chart highlights just how centralised the UK state is, with local government dependent on central government largesse to pay for 69% of its spending in 2022/23.

Local authorities received £41bn in council taxes and £18bn in non-tax receipts, with intra-government transfers amounting to £141bn, comprising £127bn in revenue grants and £14bn in capital grants. Transfers included a redistribution of £25bn in business rates, which although collected by local authorities are national taxes whose disposition is determined by central government. The rest came from a combination of block grants, subsidies, and specific grants (some of which councils need to bid for) as part of a complex and complicated web of funding arrangements for local authorities that makes them highly dependent on the decisions of government ministers.

After transfers there was a reported deficit of £137bn in central government and £4bn in local government, while £8bn in net transfers converted a £4bn shortfall between receipts and expenditure in the three other segments into a net £4bn surplus.

The big picture is of the most centralised state among medium and large economies in the developed world, with local authorities almost entirely dependent on the largesse of central government to fund the essential public services they deliver.

Distributing power to the devolved administrations in Scotland, Wales and Northern Ireland has started to see a share of national taxes dispersed (such as income tax in Scotland and Wales) and some limited tax-raising powers. This contrasts with the debate about devolution in England, which has primarily focused on structures with the partial creation of a regional tier of local government in the form of combined authorities, rather than on more fundamental questions of whether this very centralised system of funding for local authorities needs reform.

![Exploding debt

Step chart showing how UK public sector net has changed between March 2008 and the projected position in March 2029.

[debt bars shaded orange, changes shaded in purple]

March 2008: £0.6trn

Financial crisis: +£0.7trn

March 2012: £1.3trn

Austerity years: +£0.5trn

March 2020: £1.8trn

Pandemic / energy crisis: +£0.9trn

March 2024: £2.7trn

[bar colours shaded by 50% to indicate the following are projected numbers]

Latest plan: +£0.4trn

March 2029: £3.1trn

30 Nov 2023.

Chart by Martin Wheatcroft FCA. Design by Sunday.

Source: OBR, 'Public finances databank - Nov 2023'.](https://martinwheatcroft.com/wp-content/uploads/2023/11/icaewchart286debt.jpg)

![Public sector finance trends: October 2023

Table showing receipts, expenditure, interest, net investment, deficit, other borrowing and debt movement for the seven months to October 2023 plus net debt and net debt / GDP at 31 October 2023.

Receipts: £466bn (Oct 2019), £425bn (Oct 2020), £500bn (Oct 2021), £565bn (Oct 2022), £595bn (Oct 2023)

Expenditure: (£457bn), (£582bn), (£536bn), (£548bn), (£587bn)

Interest: (£38bn), (£26bn), (£41bn), (£72bn), (£76bn)

Net investment: (£20bn), (£42bn), (£28bn), (£21bn), (£30bn)

[line above subtotal]

Deficit: (£49bn), (£225bn), (£105bn), (£76bn), (£98bn)

Other borrowing: £5bn, (£61bn), (£61bn), £5bn, (£7bn)

[line above total]

Debt movement: (£44bn), (£286bn), (£166bn), (£71bn), (£105bn)

[line below total]

Net debt: £1,821bn, £2,101bn, £2,319bn, £2,454bn, £2,644bn.

Net debt / GDP: 82.1%, 99.3%, 97.5%, 95.5%, 97.8%](https://martinwheatcroft.com/wp-content/uploads/2023/11/2023-10-Trends.jpg)