Upward revisions to GDP bring the debt-to-GDP ratio down to 95.5%, but the Chancellor has a difficult Spending Review and Autumn Budget ahead as spending pressures mount.

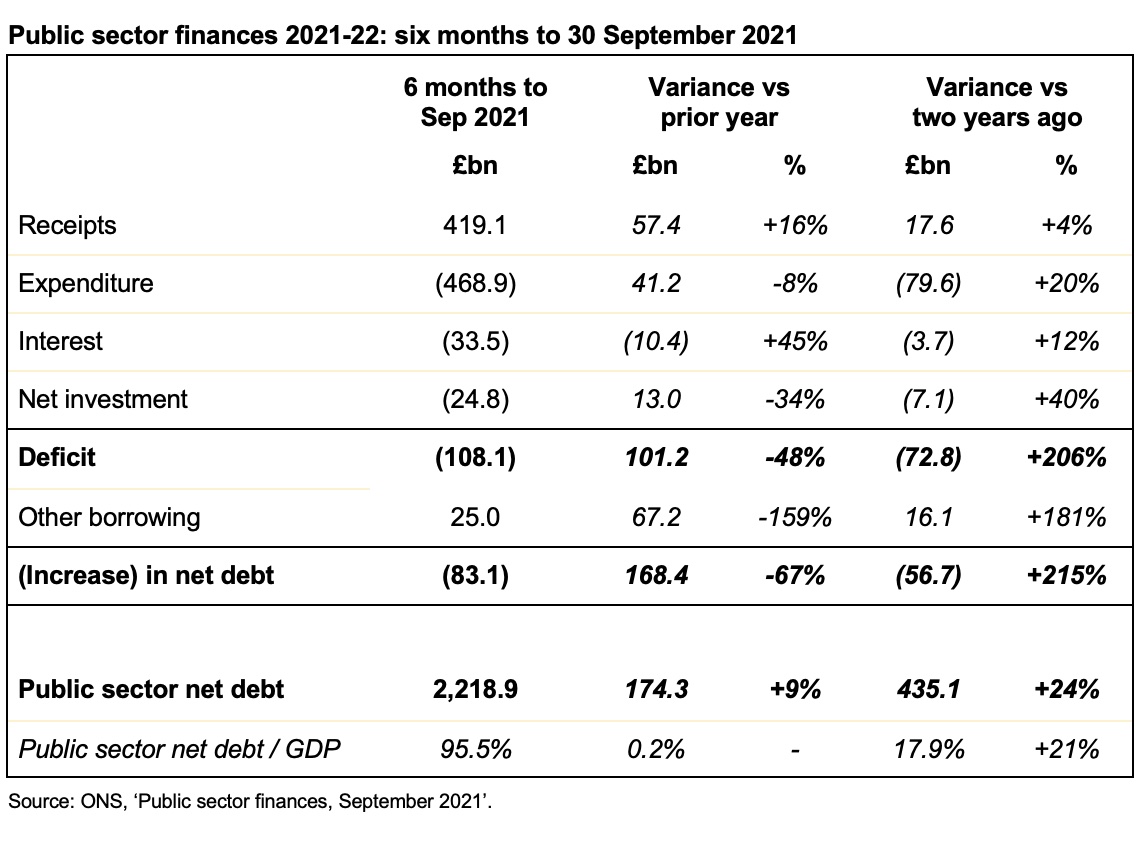

The public sector finances for September 2021 released on Thursday 21 October reported a monthly deficit of £21.8bn – better than the £28.7bn reported for September 2020 but still much higher than the deficit of £8.1bn reported for September 2019.

This brings the cumulative deficit for the first half of the financial year to £108.1bn compared with £209.3bn last year and £35.3bn two years ago.

Public sector net debt increased from £2,205.4bn at the end of August to £2,218.9bn or 95.5% of GDP at the end of September. This is £83.1bn higher than at the start of the financial year and an increase of £425.8bn over March 2020.

As in previous months this financial year, the deficit came in below the official forecast for 2021-22 prepared by the Office for Budget Responsibility (OBR) in March 2021, when the outlook appeared less positive. The OBR is expected to significantly reduce its projected deficit of £234bn for the full year when it updates its forecasts for the Autumn Budget and Spending Review on 27 October 2021.

Cumulative receipts in the first six months of the 2021-22 financial year amounted to £419.1bn, £57.4bn or 16% higher than a year previously, but only £15.2bn or 4% above the level seen a year before in 2019-20. At the same time cumulative expenditure excluding interest of £468.9bn was £41.2bn or 8% lower than the first six months of 2020-21, but £79.6bn or 20% higher than the same period two years ago.

Interest amounted to £33.5bn in the six months to September 2021, £10.4bn or 45% higher than the same period in 2020-21, principally because of higher inflation affecting index-linked gilts. Despite debt being 24% higher than two years ago, interest costs were only £3.7bn or 12% more than the equivalent six months ended 30 September 2019.

Cumulative net public sector investment in the six months to September 2021 was £24.8bn. This was £13.0bn less than the £37.8bn in the first half last year, which includes over £16bn for bad debts on coronavirus lending that are not expected to be recovered. Investment was £7.1bn or 40% more than two years ago, principally reflecting a higher level of capital expenditure.

Debt increased by £83.1bn since the start of the financial year, £25.0bn less than the deficit. This reflects cash inflows from delayed tax receipts and the repayment of coronavirus loans more than offsetting other borrowing to fund student loans and business lending.

Alison Ring, ICAEW Public Sector Director, said: “Upward revisions by the ONS to GDP brought the ratio of public debt to GDP down to 95.5% at the end of September, which is good news for the Chancellor as he gets ready for a potentially difficult Autumn Budget and Spending Review. September’s numbers continue to track below what now appear to be over-prudent forecasts from the Office for Budget Responsibility back in March, and the OBR will likely improve its projections for the Spending Review period when it reports next week.

“However, at £108.1bn the deficit for the first half of the financial year to September 2021 is almost twice the deficit recorded for the last full financial year before the pandemic, and the Chancellor is a long way from getting the public finances back under control. Difficult decisions await Rishi Sunak in the Spending Review given rising debt-interest costs and existing commitments on health, schools and defence will limit the capacity he has available to address significant spending pressures in many public services.”

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The ONS made a number of revisions to prior month and prior year fiscal numbers to reflect revisions to estimates. These had the effect of reducing the reported fiscal deficit for the five months to August 2021 from £93.8bn to £86.3bn and the deficit for the year ended 31 March 2021 from £325.1bn to £319.9bn.