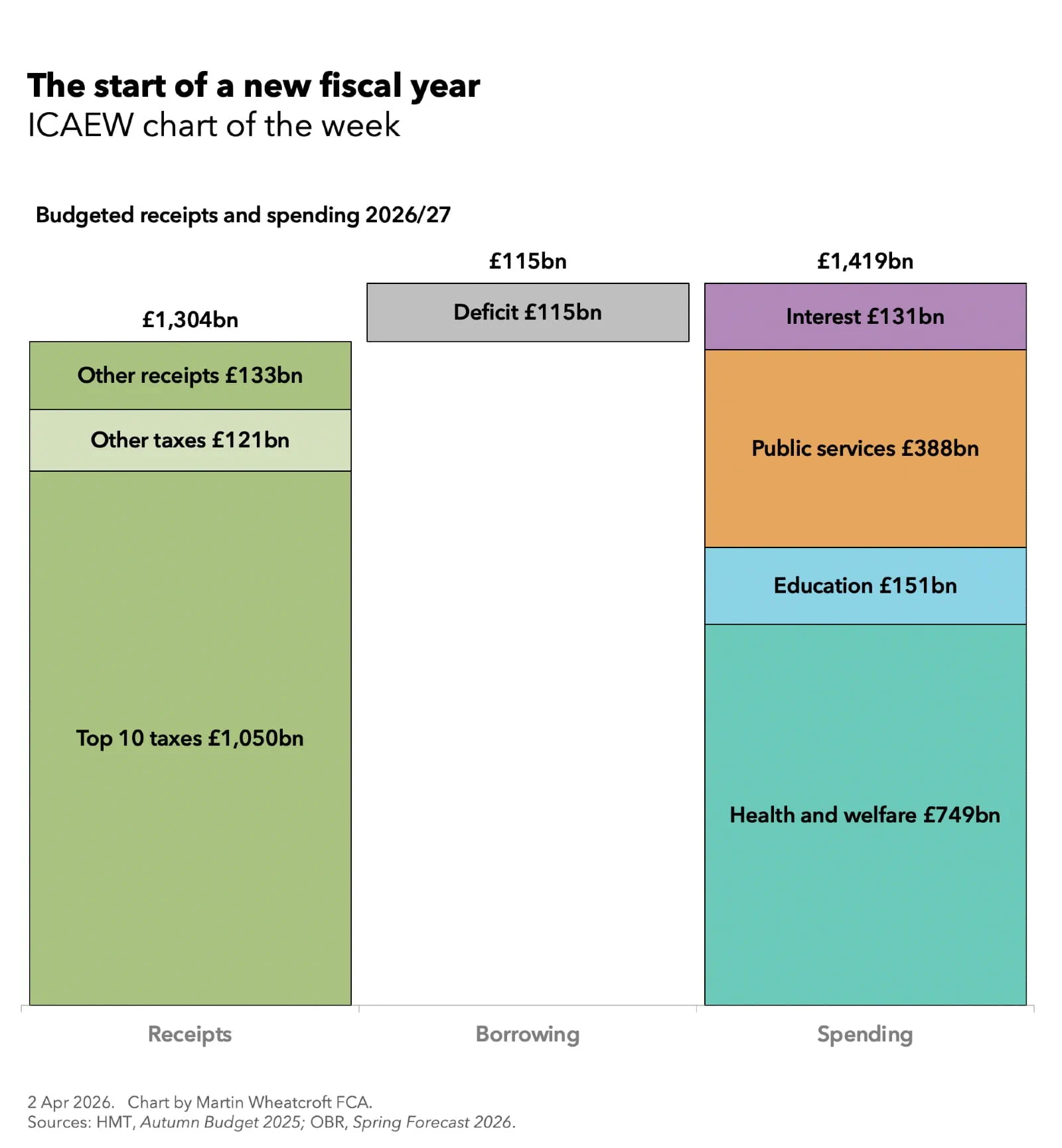

My first chart of the financial year starting 1 April 2026 for ICAEW looks at the government’s £1.4tn budget for 2026/27.

My chart fir ICAEW this week is on the public sector budget for the 2026/27 financial year which began on 1 April 2026, showing how there is expected to be a shortfall of £116bn between anticipated receipts of £1,304bn and planned spending of £1,419bn.

This is equivalent to a deficit of 3.6% of GDP, calculated as receipts of 41.2% of GDP less total managed expenditure of 44.8% of GDP.

The chart highlights how the top 10 taxes are expected to generate £1,050bn (81% of total receipts), with all other taxes contributing £121bn (9%) and other receipts generating £133bn (10%).

The top 10 taxes comprise: income tax which generates £360bn, VAT (£220bn), employer national insurance (£155bn), corporation tax (£102bn), employee and self-employed national insurance (£57bn), council tax (£54bn), business rates (£37bn), fuel duties (£24bn), capital gains tax (£21bn) and property transaction taxes (stamp duty in England) generating £20bn.

The remaining £121bn of tax receipts comprises £84bn from the next 10 largest taxes: environmental duties (£16bn), alcohol duties (£13bn), vehicle excise duty (£10bn), inheritance tax (£9bn), insurance premium tax (£9bn), tobacco duties (£7bn), air passenger duty (£5bn), stamp duty on shares (£5bn), customs duties (£5bn) and the apprenticeship levy (£5bn), and £37bn from all other taxes and duties.

Other receipts comprise £87bn from operating surpluses (including social housing rents and the profits of public corporations), £43bn in interest and dividends (on investments and cash balances), and £3bn other receipts.

On the spending side, the chart illustrates how the £749bn budgeted for health and welfare is more than half of the total (approximately 53%), while education spending is budgeted to be £151bn (11%), public services outside of health, social care and education amount to £388bn (27%) and interest is forecast to be £131bn (9%).

Health and welfare spending comprises £401bn on welfare (including the state pension), £294bn on health (principally the NHS), and social care provision of £54bn. Budgeted spending on public services outside of health, social care and education include defence and security of around £70bn, transport £69bn, public order and safety £62bn, industry, agriculture and employment £56bn, and housing and environment £51bn, together with £80bn across the hundreds of other public services provided by central and local government.

The planned borrowing to fund the deficit of £116bn, the difference between receipts and total managed expenditure, excludes £15bn in other borrowing to fund government lending activities and working capital movements, with public sector net debt scheduled to rise above £3tn during the coming financial year.

The problem for the Chancellor – and for all of us – is that the actual numbers for 2026/27 could be significantly worse from the budgeted amounts presented in our chart. Not only is she already under significant pressure to increase defence spending and alleviate student loans (amongst many other spending challenges), but the conflict with Iran will make the situation even more challenging for both the government and the nation.

On that cheery note, we would like to wish you all the best for the new (financial) year.