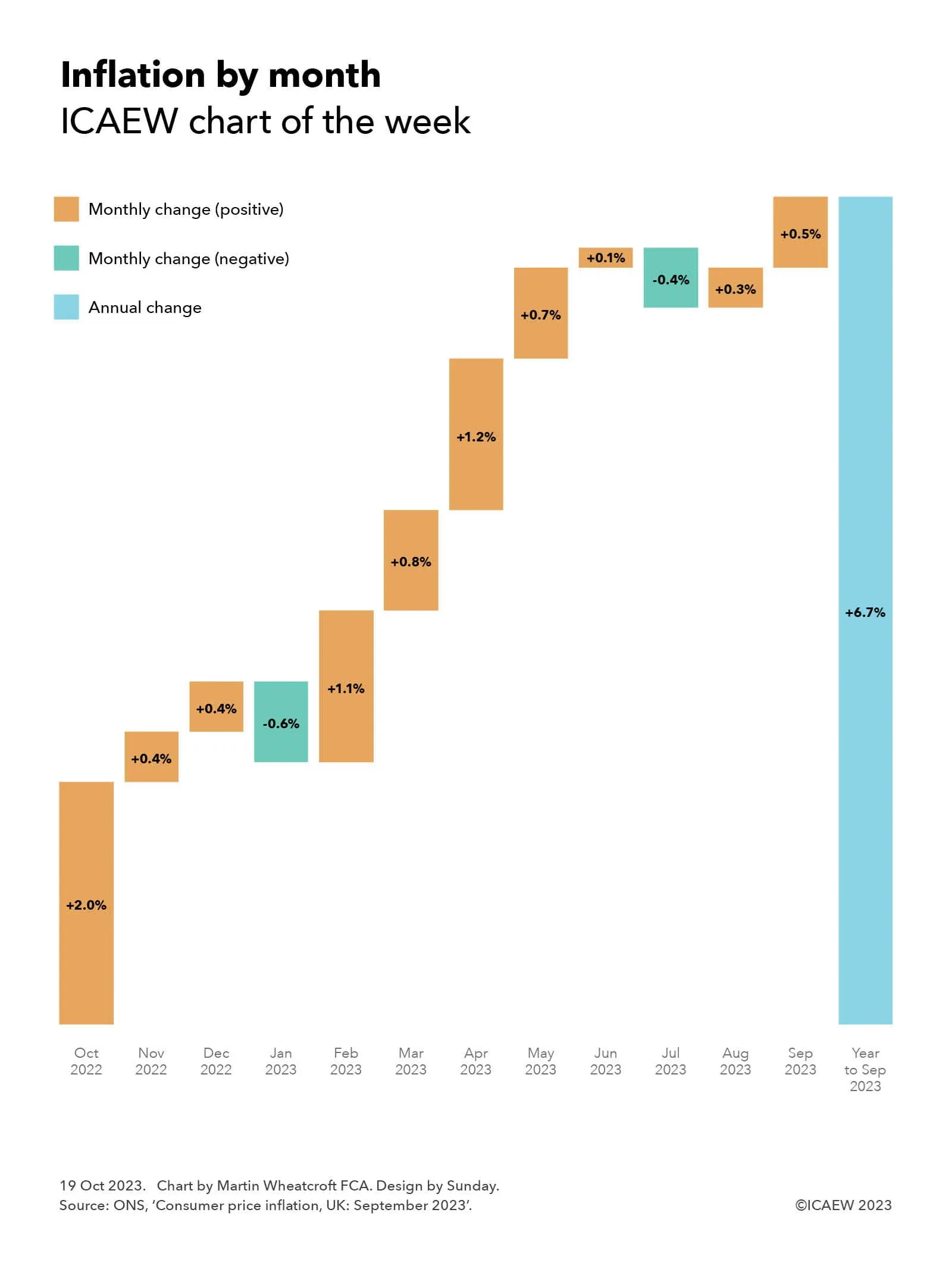

My chart this week looks at how September’s inflation rate of 6.7% is made up by month, and why a big drop in the annual rate is predicted next month.

The Office for National Statistics (ONS) reported on 18 October 2023 that the annual rate of consumer price inflation (CPI) for the year to September 2023 was 6.7%.

Our chart this week illustrates how this is made up of monthly inflation rates from October 2022 through September 2023 of +2.0%, +0.4%, +0.4%, -0.6%, +1.1%, +0.8%, +1.2%, +0.7%, +0.1%, -0.4%, +0.3% and +0.5% respectively.

As well as highlighting how the monthly inflation rate can bounce around from month to month, including a couple of times where prices went down, it shows how a big jump in the consumer prices index of +2.0% in October 2022 is a significant component in the annual rate reported for the year to September 2023.

This provides an insight into what is likely to happen to inflation when it is reported next month. Instead of a large rise in domestic energy prices (a 17% increase in the cost of electricity and a 37% increase in the cost of domestic gas between September and October 2022 according to the ONS) that drove the +2.0% reported a year ago, the expectation is that energy prices will drop between September and October 2023 following Ofgem’s decision to reduce the energy price cap by 7% for the current quarter.

When the +2.0% monthly increase from October 2022 drops out of the index to be replaced by a much smaller monthly increase for October 2023 (or even potentially a monthly decrease), the annual rate of inflation should reduce significantly – potentially to as low as the 5.3% ‘halved’ rate of inflation aspired to by the Prime Minister.

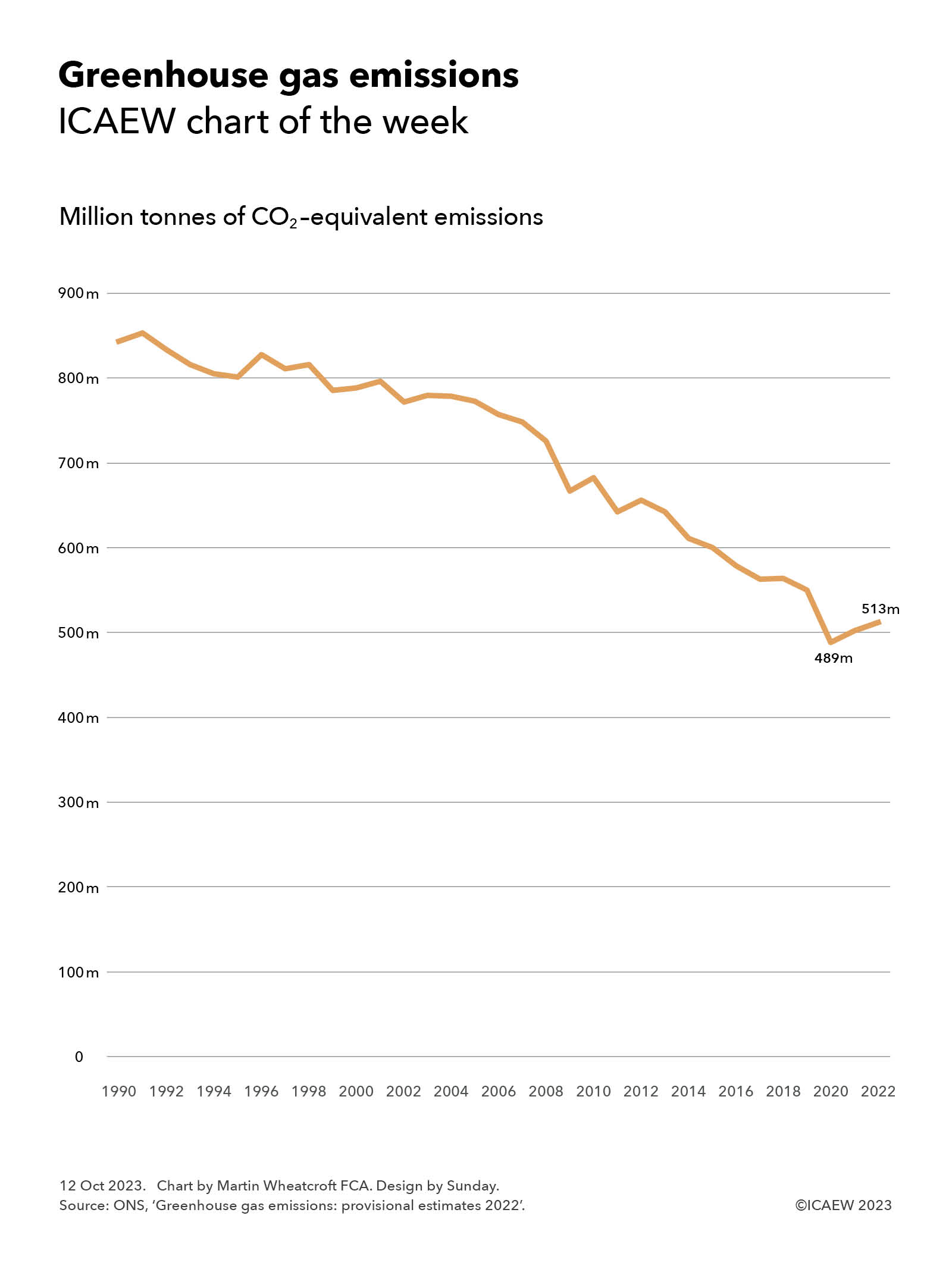

My chart this week looks at how greenhouse gas emissions increased again in 2022 after a big dip during the pandemic. Was that just a blip or will the downward trend resume?

The Office for National Statistics (ONS) recently reported provisional numbers for greenhouse gas emissions in 2022, reporting that UK residents and UK-resident businesses emitted a total of 513m tonnes of carbon dioxide equivalents (tCO2e).

Our chart this week shows the overall trend since 1990 according to the ONS. Emissions were 843m tCO2e in 1990, rising to 853m tCO2e in 1991, from which point they have declined in most years since then apart from the odd upward blip.

The 513m tCO2e provisionally estimated to have been emitted in 2022 is up 2% over 2021 and just under 5% higher than the 489m tCO2e emitted during 2020, the first year of the pandemic when much of the country was locked down.

The good news is that this is still 7% lower than the 551m tCO2e emitted during 2019.

This disruption to the downward trend is primarily due to the pandemic, which saw emissions drop by a massive 11% in 2020 compared with 2019, before rising by 3% in 2021 and 2% in 2022.

The hope is that the downward trend will resume in 2023 and 2024 as decarbonisation efforts continue.

Most of the fall in emissions since 1991 has been delivered by the shift from coal to gas and renewable sources in electricity generation, combined with greater energy efficiency in appliances and equipment – what many commentators call “the easy bit”. The next stages of decarbonisation will be much harder as it involves switching everyone from fossil-fuel-powered vehicles to electric, completing the shift to renewable electricity generation, decarbonising most industrial processes and radically changing how we heat our homes and offices.

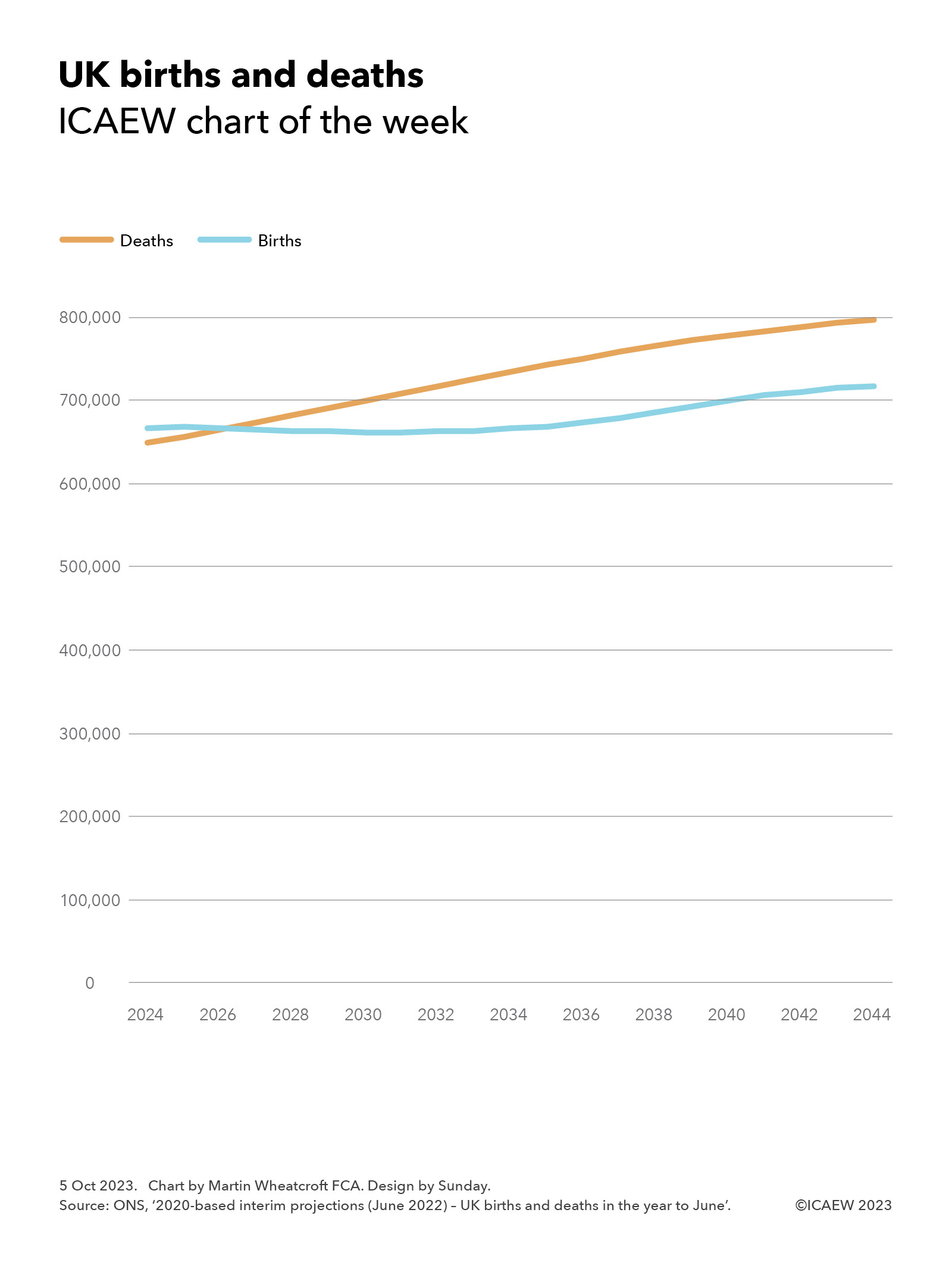

My chart this week looks at how deaths in the UK are expected to exceed births within just a couple of years – a major change in our demographic story.

The big drivers of population change in the UK (and in many other developed countries) have been a declining birth rate and more people living longer, resulting in a growing population even before taking account of net inward migration.

However, that growth is starting to slow as the birth rate has declined as a proportion of the overall population – absent migration, it is expected to start to go into reverse as the death rate rises, driven by the bulge in the population constituted by the ‘baby boomer’ generation reaching their 60s and 70s.

As illustrated by my chart this week, the number of births is expected to fall slightly over the next few years (from 667,000 in the year to June 2024 and 668,000 in the year to June 2024 to 662,000 in the year to June 2031) before gradually rising to 718,000 in the year to June 2044. At the same time deaths are expected to rise throughout the period, from 650,000 in the year to June 2024 to 797,000 in the year to June 2044.

The projection is for births of 667,000 and deaths of 665,000 in the year to June 2026, a small net increase of 2,000, before reversing after that to reach 80,000 more deaths than births in the year to June 2044.

The population is still expected to grow, despite this shift from (to use the statistical terminology) ‘natural’ growth in the population (births exceeding deaths) to ‘natural’ contraction (deaths exceeding births). This is because the ONS has assumed net inward migration will continue at an average of 245,000 a year for most of the projection period, resulting in a projected growth in the population of 4.0m people or 6% (from 68.1m to 72.1m) over the next 20 years, in contrast with the 8.4m or 14% increase in the UK’s population over the past two decades.

Without inward migration, the likelihood is that the gap between deaths and births would be even larger than illustrated in our chart, given that a proportion of the children expected to be born will be the children of migrants.

This change in the demographics of the UK will have significant implications for the debate about migration over the coming decades, especially if the population absent migration is shrinking by 80,000 a year by 2044 as projected by the ONS.

There are also implications for the public finances as, even with net inward migration, population growth is expected to be less than 0.3% a year over the next two decades instead of the 0.7% a year seen over the past 20 years. Not only will that reduce the potential for economic growth, but it will reduce the opportunities for efficiencies of scale in public spending that have been possible in previous decades.

The demographic tale of the 20th century in the UK was one of a rapidly growing population as many more children survived into adulthood, life expectancy increased significantly and migration offset a declining birth rate. The 21st century looks like being a very different story.

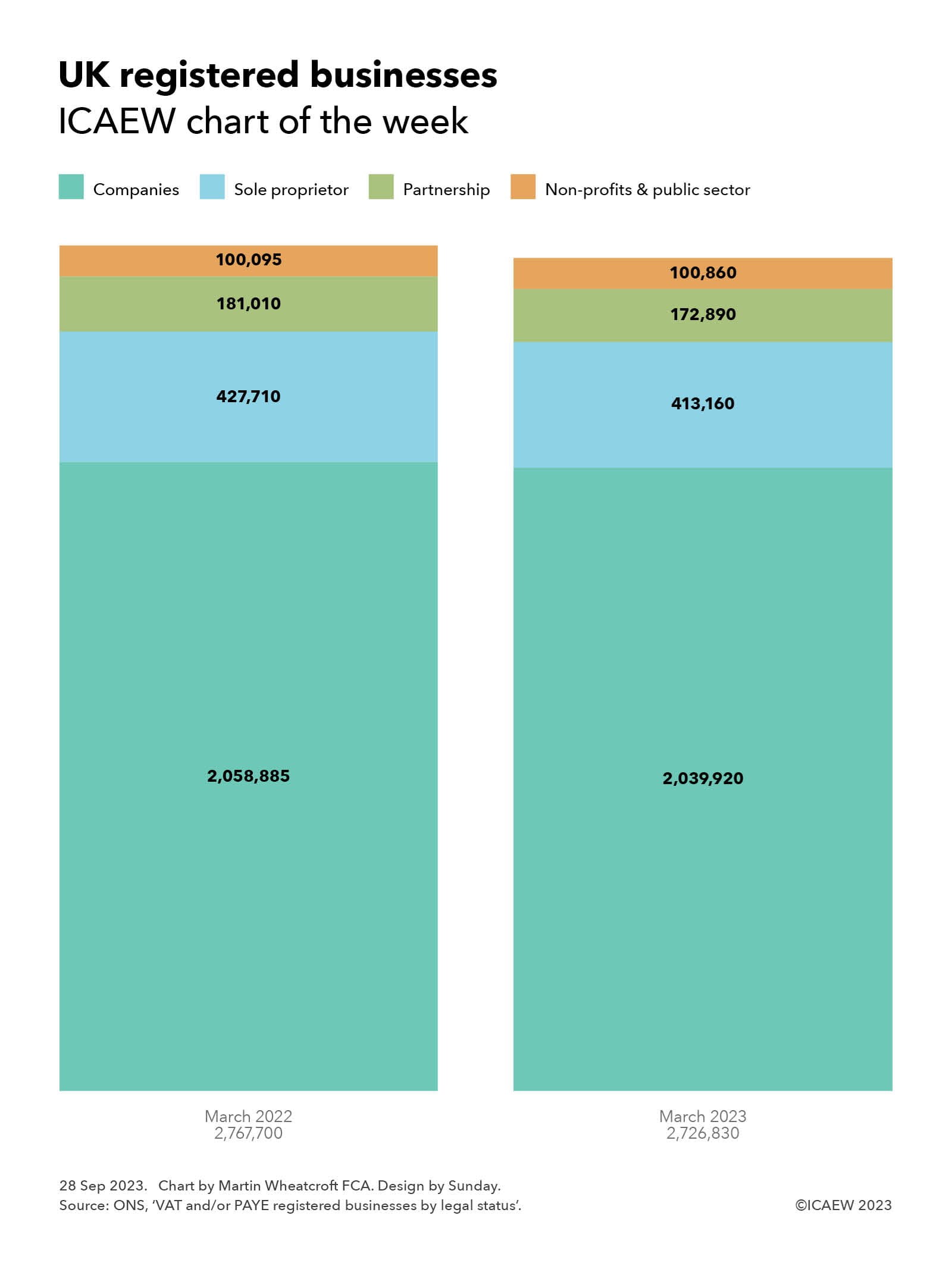

My chart this week looks at the 1.5% drop in the number of VAT- and PAYE-registered businesses in the year to 31 March 2023.

On 27 September 2023, the Office for National Statistics (ONS) published data on the 2,726,830 businesses that were registered for VAT and/or PAYE in the UK as of March 2023, a 1.5% fall from the 2,767,700 businesses that were registered a year previously.

As illustrated by our chart this week, the number of VAT- and PAYE-registered companies fell by 0.9% from 2,058,885 to 2,039,920, sole proprietorships fell by 3.4% from 427,710 to 413,160, and partnerships fell by 4.5% from 181,010 to 172,890.

Bucking the trend were non-profit bodies, mutual associations and public sector organisations, which rose by 0.8% from 100,095 to 100,860. The latter comprised 88,375 non-profit bodies and mutuals, 9,030 local authority entities, 3,280 central government entities and 175 public corporations and other publicly owned businesses, as of March 2023.

Not shown in the chart are in the order of 2.8m ‘unregistered’ businesses that are not registered for VAT or PAYE. Most of these are self-employed individuals, sole traders, or one-person companies that generate revenue below the VAT threshold of £85,000 and do not have any payrolled employees.

The number of registered businesses in March 2023 by industry group are comprised as follows:

415,250 professional, scientific and technical (down 3.7% on March 2022);

402,165 motor trades (-2.8%);

377,585 construction (+0.7%);

226,285 business administration and support services (-1.1%);

187,360 information and communication (-4.5%);

184,420 arts, entertainment, recreation and other services (+2.0%);

174,830 accommodation and food services (-0.2%);

151,710 production (-1.8%);

141,390 agriculture, forestry and fishing (-0.8%)

128,600 transport and storage including postal (-6.9%);

113,785 (+2.8%) property, 109,095 health (+2.8%);

59,210 finance and insurance (-2.0%);

47,340 education (+1.3%); and

7,805 public administration and defence (+0.4%).

There were 2,115,105 businesses with between zero and four employees as of March 2023, followed by 313,780 (five to nine employees), 157,955 (10-19), 86,285 (20-49), 27,660 (50-99). 15,135 (100-249) and 10,910 (250+).

By turnover band, the numbers as of March 2023 were: 445,020 (£0-£49,999); 563,610 (£50,000-£99,999); 846,615 (£100,000-£249,999); 367,315 (£250,000-£499,999); 222,155 (£500,000-£999,999); 123,995 (£1m-£2m); 85,655 (£2m-£5m); 32,100 (£5m-£10m); 29,080 (£10m-£50m); and 9,285 (£50m+).

The fall in the number of businesses in 2022/23 is perhaps not surprising given the significant amount of support provided to many businesses during the pandemic, which will have delayed the normal process of business closure during the previous two years. Meanwhile, the cost-of-living and energy crises will have also made it difficult for some businesses to survive in the year to March 2023. Even though energy prices have come down, the cost-of-living crisis and consequent reductions in consumer demand could see further businesses fail during 2023/24.

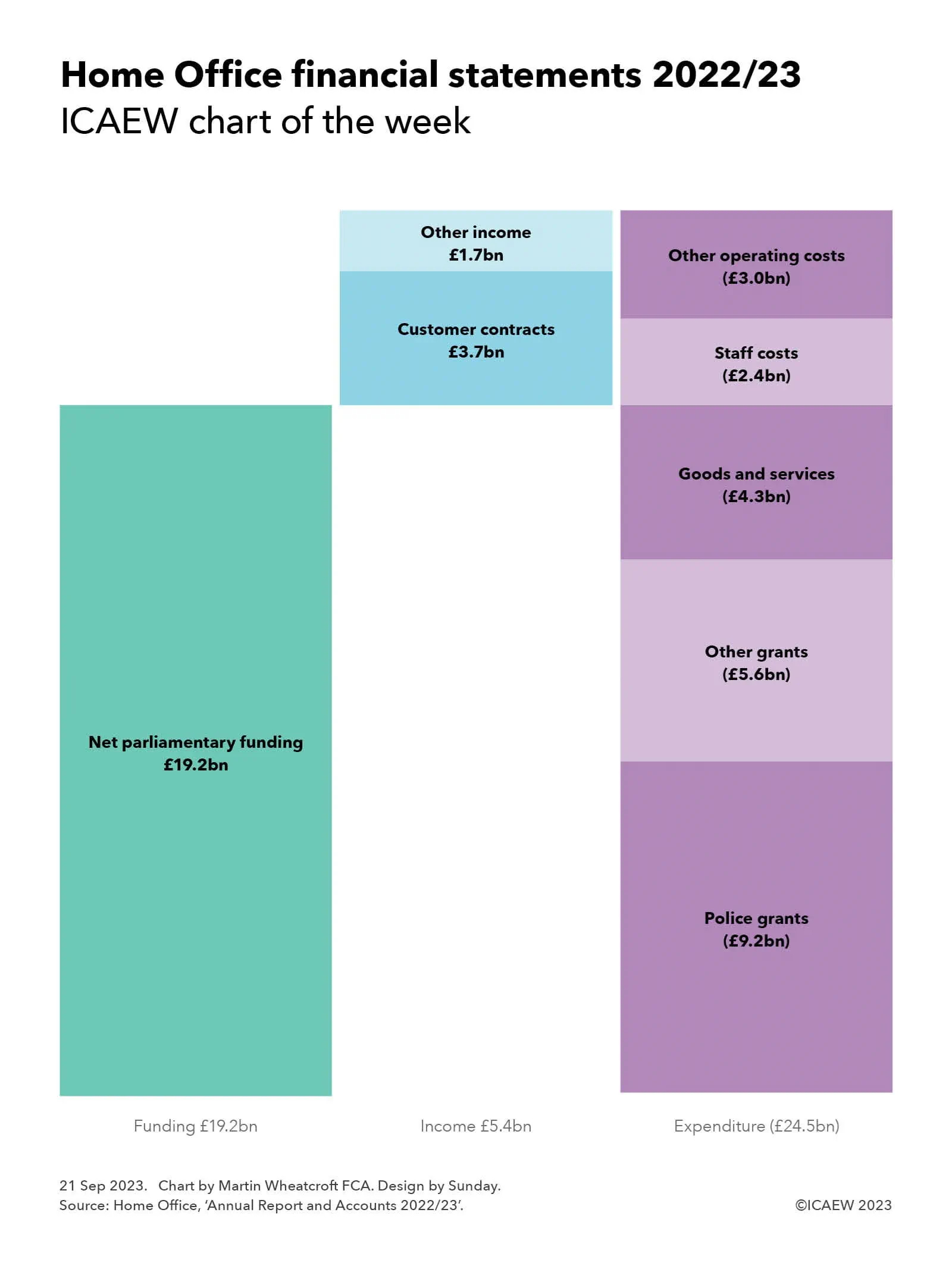

The Home Office spent £24.5bn in 2022/23 according to its recently published annual financial report, funded by £5.4bn in income and £19.2bn in net parliamentary funding.

The Home Office published its Annual Report and Accounts for the year ended 31 March 2023 on 19 September 2023.

Net expenditure in 2022/23 was £19.1bn, comprising expenditure of just over £24.5bn net of income of £5.4bn, while parliamentary funding net of other items amounted to £19.2bn.

The Home Office breaks down its income for the year of £5.4bn between revenue from contracts with customers of £3.7bn and other income of £1.7bn. The former includes £2.2bn from visa and immigration charges, £0.6bn in passport fees, £217m for the disclosure and barring service (DBS), and £0.7bn from other sources. Other income is primarily comprised of immigration health surcharges payable by foreign residents and visitors for the use of the National Health Service, a proportion of which is transferred to the Department of Health and Social Care and the devolved administrations.

As our chart this week illustrates, the majority of the Home Office’s spending is in the form of grants. The largest grants, totalling £9.2bn, are to local police forces across England to supplement the council tax precepts they raise locally. Other grants include £1.7bn to top up police pensions, £0.4bn to top up fire and rescue services pensions, £3.3bn in other operating grants (many of which also go to police forces, in addition to transfers to other government departments) and £209m in capital grants.

Purchases of goods and services of £4.3bn is dominated by the £3.1bn paid in relation to asylum and detention, together with £287m in facilities management and staff services, £229m on professional fees, £219m for media and IT, £169m for passport printing and stationery and £120m for visa and immigration commercial partners amongst other costs.

Staff costs of £2.4bn cover the costs of employing full-time equivalent averages of 41,607 permanent staff, seven ministers, seven special advisers, and 6,489 other staff during 2022/23. Wages and salaries amounted to £1.8bn, equivalent to an average full-time equivalent salary of £37,900.

At 31 March 2023 there were 345 senior civil servants on salaries in excess of £70,000, of which 251 were between £70,000 and £100,000, 86 between £100,000-£150,000 and eight between £150,000 and £190,000. The average of seven government ministers who served during the year (a total of 22 different individuals!) earned the equivalent of an average annual salary not including pension entitlements of around £49,000 in addition to their parliamentary salary or House of Lords attendance allowances.

Other operating costs of £3.0bn include £1.6bn on IT and accommodation-related service charges, £0.7bn for depreciation and amortisation of assets, and £113m in asset recovery costs together with other costs.

Parliamentary funding net of other items of £19.2bn is reported in the consolidated statement of taxpayers’ equity and comprised £19.4bn in drawn-down parliamentary funding, £0.3bn in deemed funding less £0.5bn in amounts repayable.

Not shown in the chart is the Home Office’s consolidated balance sheet, which comprised £2.6bn in non-current assets, trade and other receivables of £0.7bn and cash and cash equivalents of £0.6bn less trade and other payables of £3.7bn, £0.6bn in lease liabilities and £0.5bn in provisions to give net liabilities of £0.9bn.

Reported in the notes to the accounts are £0.8bn in capital additions, of which £374m was incurred on software and other intangible assets.

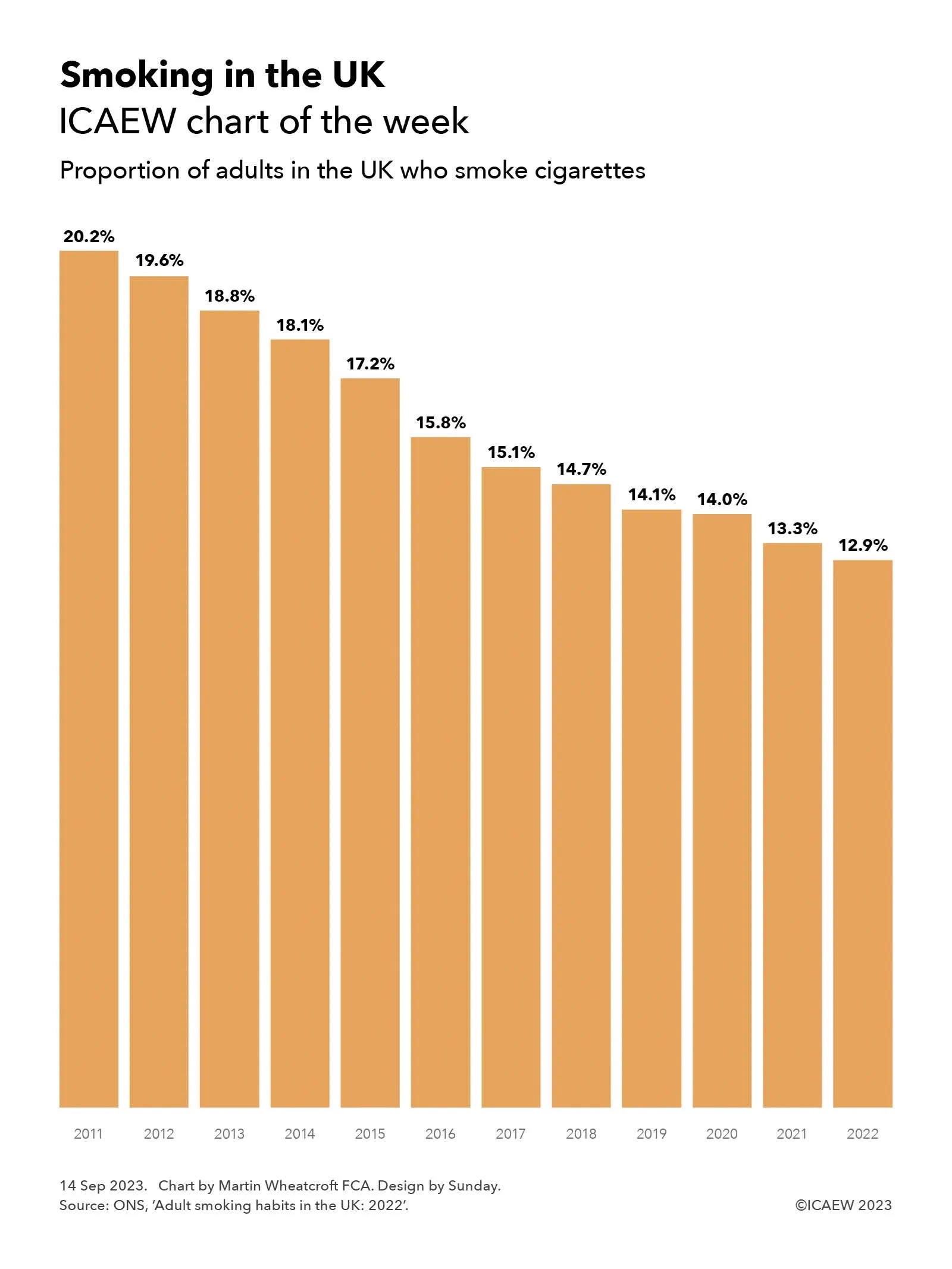

My chart of the week looks at how the prevalence of smoking in the UK population has continued to decline over the past decade.

The Office for National Statistics (ONS) has recently published its latest statistics on adult smoking habits in the UK, showing a continuing decline in the prevalence of smoking in the UK population over the past decade or so.

As my chart this week highlights, the proportion of those aged 18 or over in the UK who smoke cigarettes has fallen from 20.2% in 2011 to 19.6% (2012), 18.8% (2013), 18.1% (2014), 17.2% (2015), 15.8% (2016), 15.1% (2017), 14.7% (2018), 14.1% (2019), 14.0% (2020), 13.3% (2021) and 12.9% in 2022.

Over this period the decline is dramatic, with the respective proportion of men and women smoking down from 22.4% and 18.2% in 2011 to 14.6% and 11.2% in 2022.

The proportion of people smoking in all age groups has fallen over the past 11 years, with those aged 18-24, 25-34, 35-44, 45-54, 55-64 and 65+ who smoke declining from 25.7%, 25.8%, 23.3%, 21.6%, 18.5% and 10.2% in 2011 to 11.6%, 16.3%, 14.5%, 14.3%, 13.6% and 8.3% in 2022.

While the government and anti-smoking campaigners will be pleased by the continued progress in persuading people to give up smoking, they will be more concerned by the increase in the numbers vaping, particularly among those in their late teens and early 20s.

The proportion of those aged 16 or over in Great Britain who use e-cigarettes on a daily or occasional basis increased from 6.4% in 2020 to 8.7% in 2022. For those aged 16-24, 25-34, 35-49, 50-59 and 60+ the increase was from 7.0%, 8.6%, 7.5%, 7.9% and 3.5% in 2020 to 15.5%, 10.6%, 9.5%, 8.5%, 4.4% in 2022. (These percentages are not properly comparable with the smoking statistics as they are for a different comparator period, include those aged 16 and 17, are for different age bands, and exclude Northern Ireland.)

The continued decline in smoking has had a consequent impact on tobacco duty as despite a 70% rise in tobacco duty rates between 2011 and 2022, the amount collected has declined from £9.9bn in 2011/12 to £9.4bn in 2022/23, a drop in cash terms of 5% and in real terms of 26%.

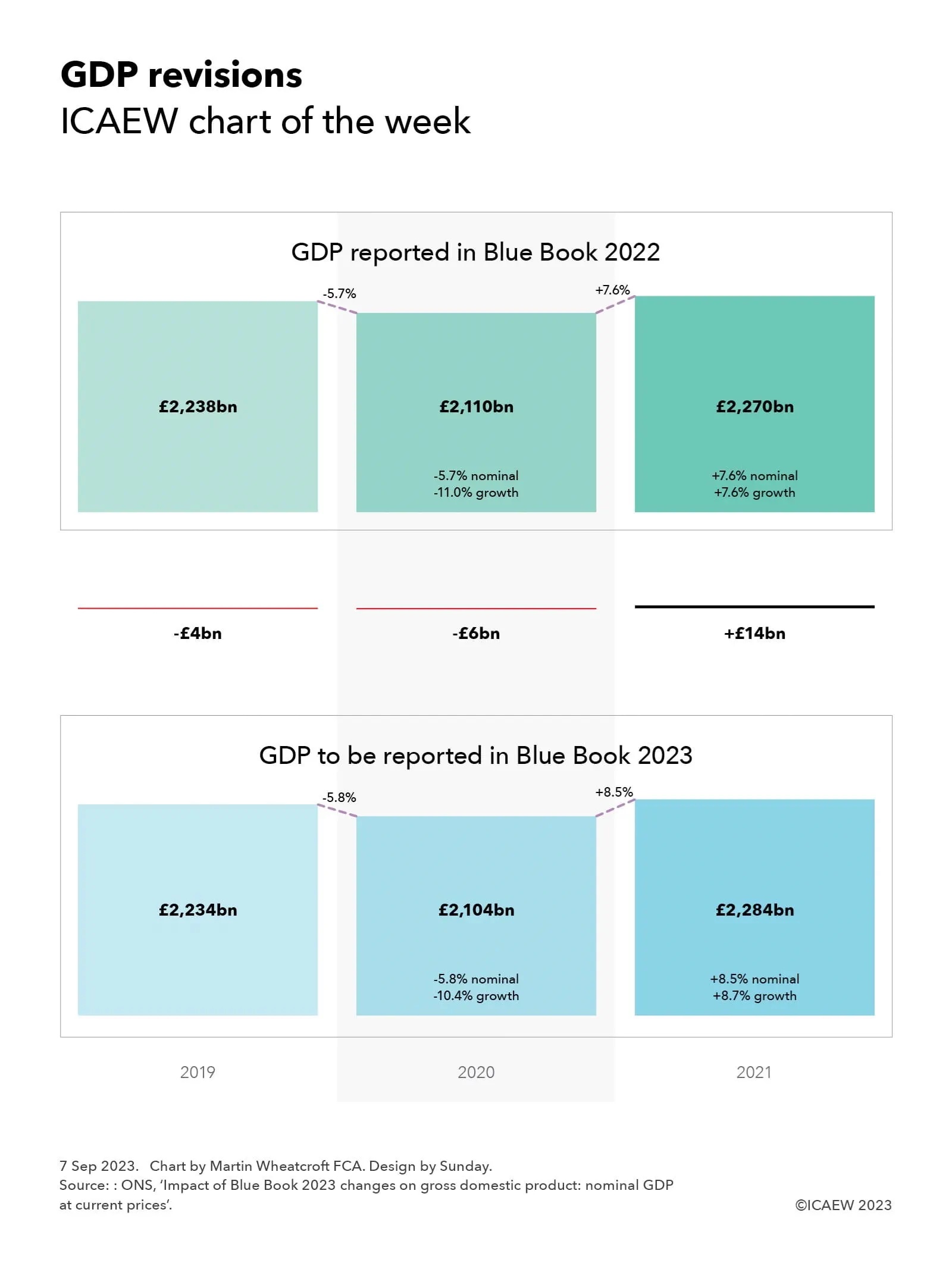

This week’s chart takes a look at recent revisions to GDP that have caused some consternation in the world of statistics.

Each year the Office for National Statistics (ONS) publishes the ‘Blue Book’ on the national accounts, its definitive analysis of economic activity over the course of the previous year. This analysis supersedes the preliminary and revised monthly and quarterly estimates issued up until that point, based on extensive analysis by the official statisticians.

The 2023 edition of the Blue Book is scheduled to be published on 31 October 2023. It will be eagerly pored over by economists in and outside government who will be eager to understand how the UK economy performed during 2022, and how this ‘final’ version of the 2022 numbers line up with those preliminary and revised estimates, just as they did last year when looking at GDP for 2021.

However, in the world of statistics numbers are never final. On 1 September 2023, the ONS announced methodological and data improvements to last year’s Blue Book – the numbers for 2021 and earlier years. These prior-period adjustments partly reflected a methodology change in the way the three different methods of calculating GDP (output, income and expenditure) are reconciled, but much more significant were revisions to the data used to calculate some of the key statistics, causing much wailing and gnashing of teeth by some prominent economic commentators as the narrative around the UK’s emergence from the pandemic changed.

As our chart this week illustrates, the revisions to GDP do not at first sight appear to be that significant. GDP for 2019 has been revised down by £4bn from the previously reported £2,238bn to a new official number of £2,234bn; GDP for 2020 is £6bn down from £2,110bn to £2,104bn; and GDP for 2021 has been revised up by £14bn from £2,270bn to £2,284bn. These seem relatively small changes when looking at trillions of pounds of economic activity.

Where the change really has an impact is in looking at the trends, especially after adjusting for inflation. On a nominal basis, a 5.7% nominal decrease in 2020 followed by a 7.6% increase in 2021 has changed to a 5.8% decrease and an 8.5% increase, but in real terms the previously reported economic contraction of 11.0% in 2020 followed by a 7.6% recovery has changed to a smaller contraction of 10.4% followed by a stronger recovery of 8.7%.

Of course, the devil is in the detail and some of the revisions at an industry level have been much more dramatic, with wholesalers and retailers now believed to have grown more strongly than previously believed, while the iron and steel industry changed from growth to contraction.

Many economic commentators have focused on the change in quarterly GDP (not shown in the chart) where the arithmetical changes have been more pronounced. The movement from the fourth quarter of 2019 (previously £568bn, now £566bn) and the fourth quarter for 2021 (previously £593bn, now £597bn) has gone from a 4.4% increase over two years to a 5.5% increase; in real terms from a 1.2% contraction in the economy to growth of 0.7%. Still anaemic, but at least in positive territory.

Despite this small improvement in the economic story portrayed by the GDP statistics, we should not get too carried away. Economic growth remains well below the pre-financial crisis levels and the public finances are in a significantly worse state than they were back in 2008.

In the meantime, the Office for Statistics Regulation has commenced a review into how these small revisions with big implications for our understanding of the economy were not identified at the time.

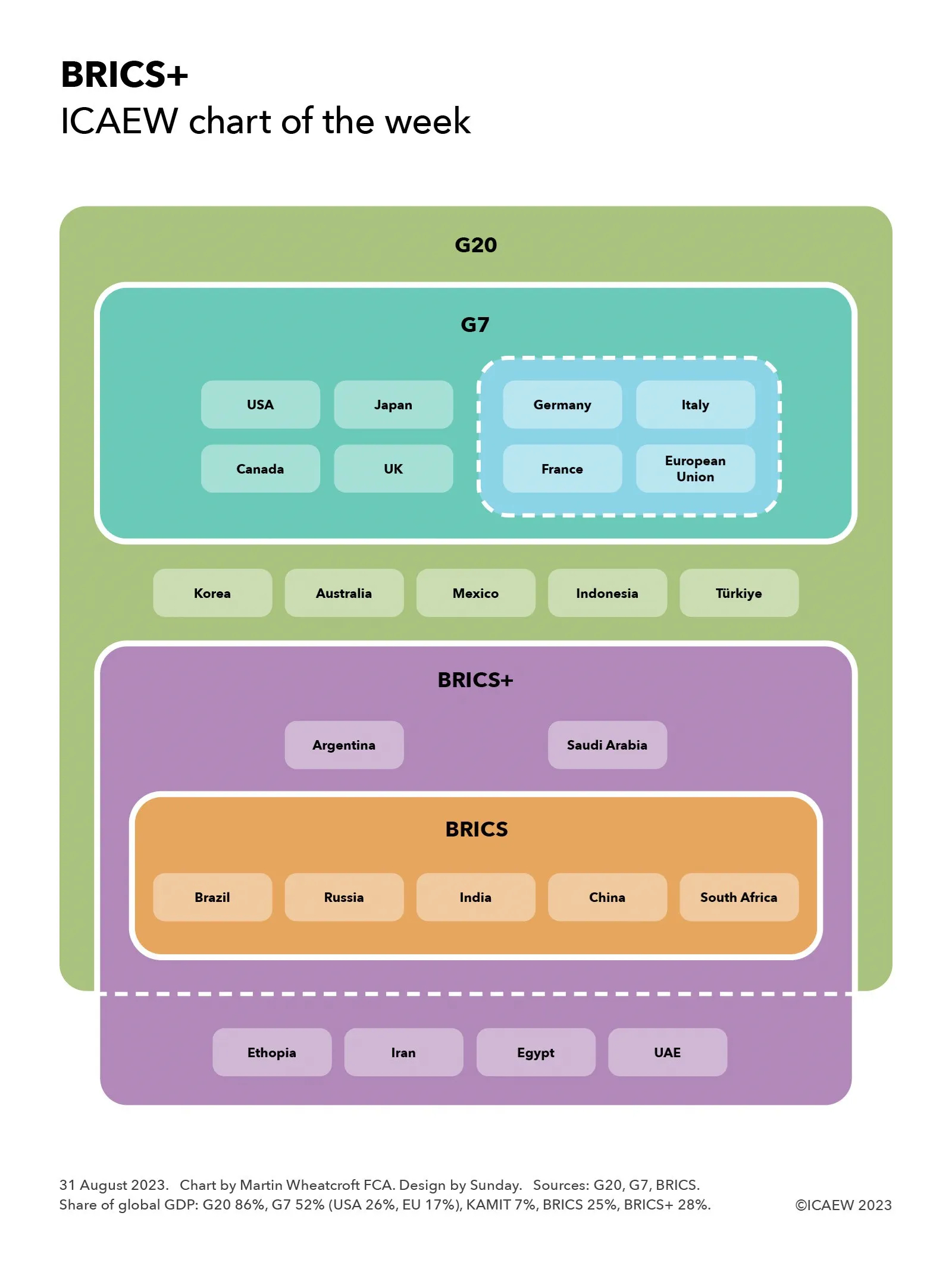

The ICAEW chart of the week returns from its summer holidays to look at the planned expansion of BRICS from five to 11 countries.

“The BRICs” was originally coined by Jim O’Neill in 2001 as an abbreviation for Brazil, Russia, India and China, four fast-growing economies that he predicted would come to dominate the world economy.

This investment shorthand evolved into something more substantive in 2006 when ministers from the four countries got together on the sidelines of a meeting at the UN. Leader summits started in 2009, followed by the addition of South Africa in 2011, which resulted in the capitalisation of the final ‘s’ to form BRICS.

BRICS has developed over time to become a counterweight to the G7, providing an alternative forum for leaders of these five major nations to discuss common concerns such as economic development, currency stability, climate change, and tackling drug trafficking and organised crime. BRICS has been increasingly important to Russia since its ejection from the G7 (then the G8) following its invasion of Crimea in 2014 and to China as relations with the G7 have deteriorated over the last decade.

Our chart this week takes the form a Venn diagram to illustrate how BRICS, and the expanded “BRICS+” grouping (pending a new official name), fit with two other major intergovernmental organisations where leaders meet on a regular basis – the G7 and the G20.

It starts with the G20, a grouping of 19 nations and the European Union that together represent 86% of the global economy. Within this sit the eight members of the G7 group of advanced economies, representing 52% of the global economy: the USA (26%), Japan (4%), the UK (3%), Canada (2%), Germany (4%), France (3%), Italy (2%) and the European Union (17% including Germany, France and Italy). The five BRICS nations represent 25% of the global economy comprising: Brazil (2%), Russia (1.7%), India (4%), China (17%) and South Africa (0.4%).

The diagram is complicated by the expanded BRICS+ as although invitees Argentina (0.6%) and Saudi Arabia (1.0%) are also members of the G20, the other four new members – Ethiopia (0.2%), Iran (0.3%), Egypt (0.3%) and the United Arab Emirates (0.5%) – are outside the G20. These new members together represent 3% of the global economy, taking the expanded BRICS+ to 28%.

Squeezed between the G7 and BRICS+ are five G20 members that together make up around 7% of the global economy that are not in either grouping, being (South) Korea (1.6%), Australia (1.6%), Mexico (1.8%), Indonesia (1.4%) and Türkiye (0.8%). As yet there is no sign of an intergovernmental organisation for these “KAMIT” nations to complement the G7 and BRICS, although in practice they are often invited as guests to G7 summits in addition to their participation in meetings of the G20.

The attraction of intergovernmental forums such as the G7, BRICS and the G20 is that they enable national leaders to engage directly with their counterparts on a wide range of topics, in contrast to the often narrower focus and more formal diplomatic structures of treaty-based international organisations such as the Organisation for Economic and Co-operation Development (OECD), the World Bank or the Organisation of American States (OAS) for example.

Their informal nature gives national leaders more flexibility to (for example) change their memberships without lengthy treaty negotiations or to work together on pressing issues of mutual concern. However, that informality also makes it difficult to create binding resolutions, which is perhaps why the global alternative reserve currency proposed at the first BRICS summit in 2009 had still not been implemented by the time of the 15th summit this August.

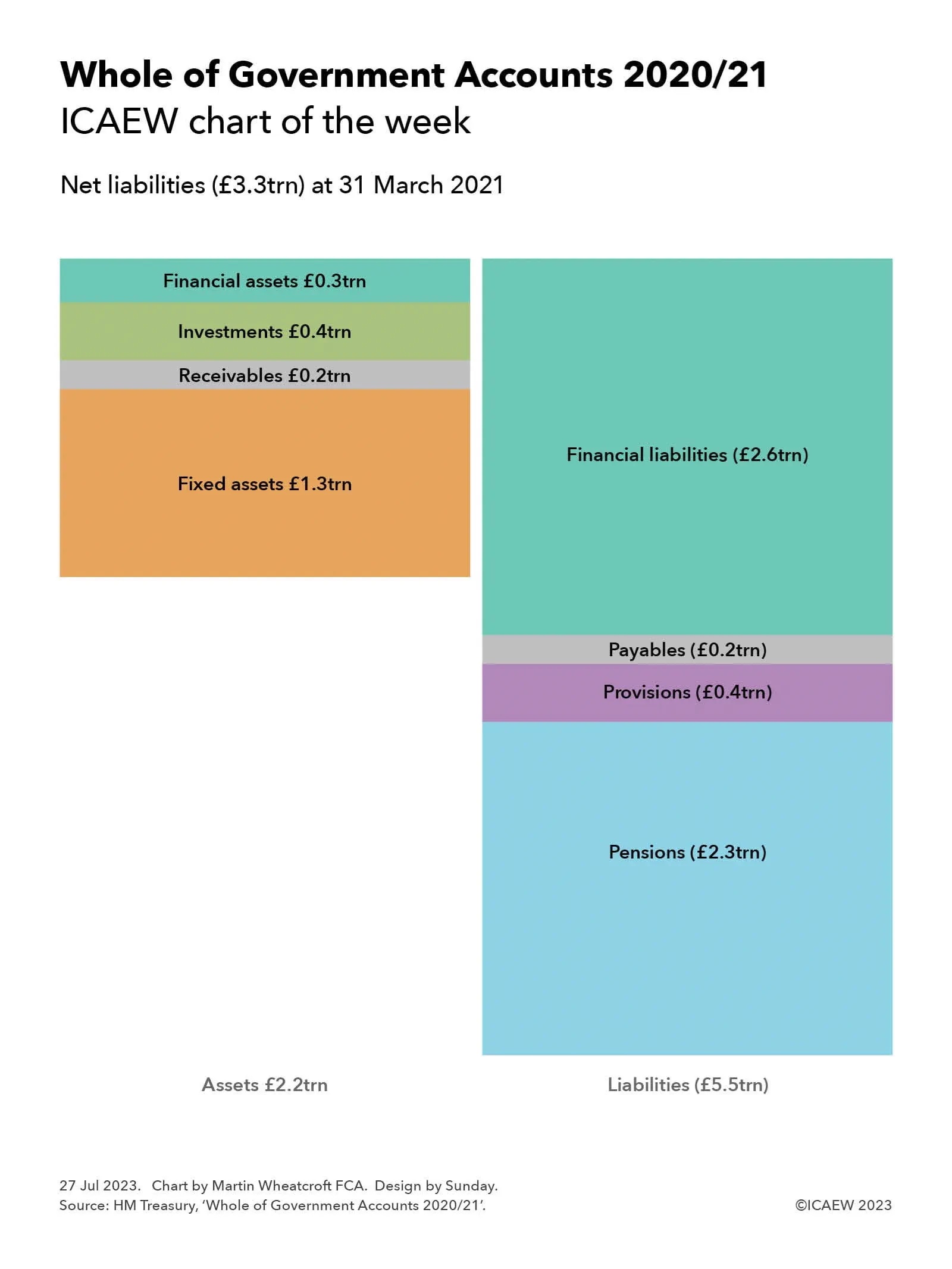

My chart this week looks at the £3.3trn of net liabilities presented in the UK government’s consolidated financial statements for the year ended 31 March 2021 that were finally published more than 27 months after the balance sheet date.

The UK’s Whole of Government Accounts for the year ended 31 March 2021 were published and submitted to Parliament on 20 July 2020, more than 27 months after the balance sheet date. These are consolidated financial statements prepared in accordance with International Financial Reporting Standards (IFRS) that incorporate the financial results of more than 10,000 public bodies in the UK across central government, local government, and other parts of the public sector.

The Whole of Government Accounts provide a much more comprehensive picture of the financial performance and position of the UK public sector than is presented in the statistics-based National Accounts, using a financial language familiar to millions of users of financial reports in the private sector.

As our chart this week highlights, the statement of financial position (balance sheet) of the UK public sector at 31 March 2021 was in heavily negative territory with £3.3trn in net liabilities, comprising assets of £2.2trn less liabilities of £5.5trn. This compares with net liabilities of £2.8trn a year earlier.

Assets of £2.2trn comprised £1.3trn in tangible and intangible fixed assets, £0.2trn in receivables and other non-financial assets, £0.4trn in non-current investments and £0.3trn in cash and other current financial assets. Liabilities of £5.5trn comprised £2.6trn in debt and other financial liabilities, £0.2trn in payables, £0.4trn in provisions and £2.3trn in net pension obligations.

Fixed assets of £1,313bn consisted of infrastructure assets of £677bn, land and buildings of £409bn, plant and equipment of £184bn, and intangible assets of £41bn. Receivables and other non-financial assets of £218bn comprised £164bn in tax receivable and accrued, £39bn in other receivables, prepayments and accruals, and £15bn in inventories. Non-current investments of £360bn comprised £152bn in loans and deposits, £85bn in student loans, £44bn in equities, £60bn in other financial investments, £16bn in investment properties, and £3bn in assets held for sale. Cash and other current financial assets of £317bn comprised £40bn in cash and cash equivalents, £12bn in gold, £129bn in debt securities, £101bn in loans and deposits, and £35bn of other financial assets.

Debt and other financial liabilities of £2,639bn comprised £1,265bn in externally held gilts, £203bn in direct borrowing from the public through National Savings & Investments, £53bn in short-term treasury bills, £815bn in Bank of England deposits, £84bn in bank and other borrowing, £85bn in banknotes, £27bn in derivatives, £20bn in financial guarantees, and £87bn in other financial liabilities. Payables of £221bn comprised £44bn in trade and other payables, £81bn in accruals and deferred income, £55bn in tax refunds, and £41bn on PFI, finance leases and other contracts. Provisions of £366bn consisted of £159bn for nuclear decommissioning, £87bn for clinical negligence, £36bn for payments to the EU, £29bn for the Pension Protection Fund, and £55bn in other provisions for liabilities and charges. Net public sector pension obligations of £2,306bn comprised £2,168bn in unfunded pension obligations (including £792bn for the NHS, £501bn for teachers, £339bn for the civil service, £254bn for the armed forces, £209bn for police and fire services, and £73bn other) and a net £138bn (£479bn of obligations less £341bn in fund assets) for local government and other funded pension schemes.

Not shown in the chart is the revenue and expenditure statement, which reported revenue of £732, expenditure of £1,063bn and finance and other items of £73bn to give a net accounting loss for the year of £404bn – more than twice the £192bn loss reported for the pre-pandemic year. The financial statements covered the first year of the coronavirus pandemic, which saw income fall and costs soar, resulting in net borrowing during the year of £524bn according to the cash flow statement.

The Whole of Government Accounts is probably the most important report published by the UK government each year, but you wouldn’t have known that by the lack of fanfare on its publication amid the wave of hundreds of other documents released ahead of the parliamentary recess. This may be driven by understandable embarrassment by the length of time it has taken to prepare them – more than 27 months after the balance sheet date compared with the nine months that is its long-term aim – as well as by the gaps in preparation caused by local authorities and other public bodies that are substantially behind in producing their individual financial statements, leading to an additional audit qualification for completeness this year.

Despite that, and the other audit qualifications that highlight problems with the numbers reported, every citizen ideally should read the Whole of Government Accounts 2020/21. After all, it tells the financial story of the most dramatic year in recent history.

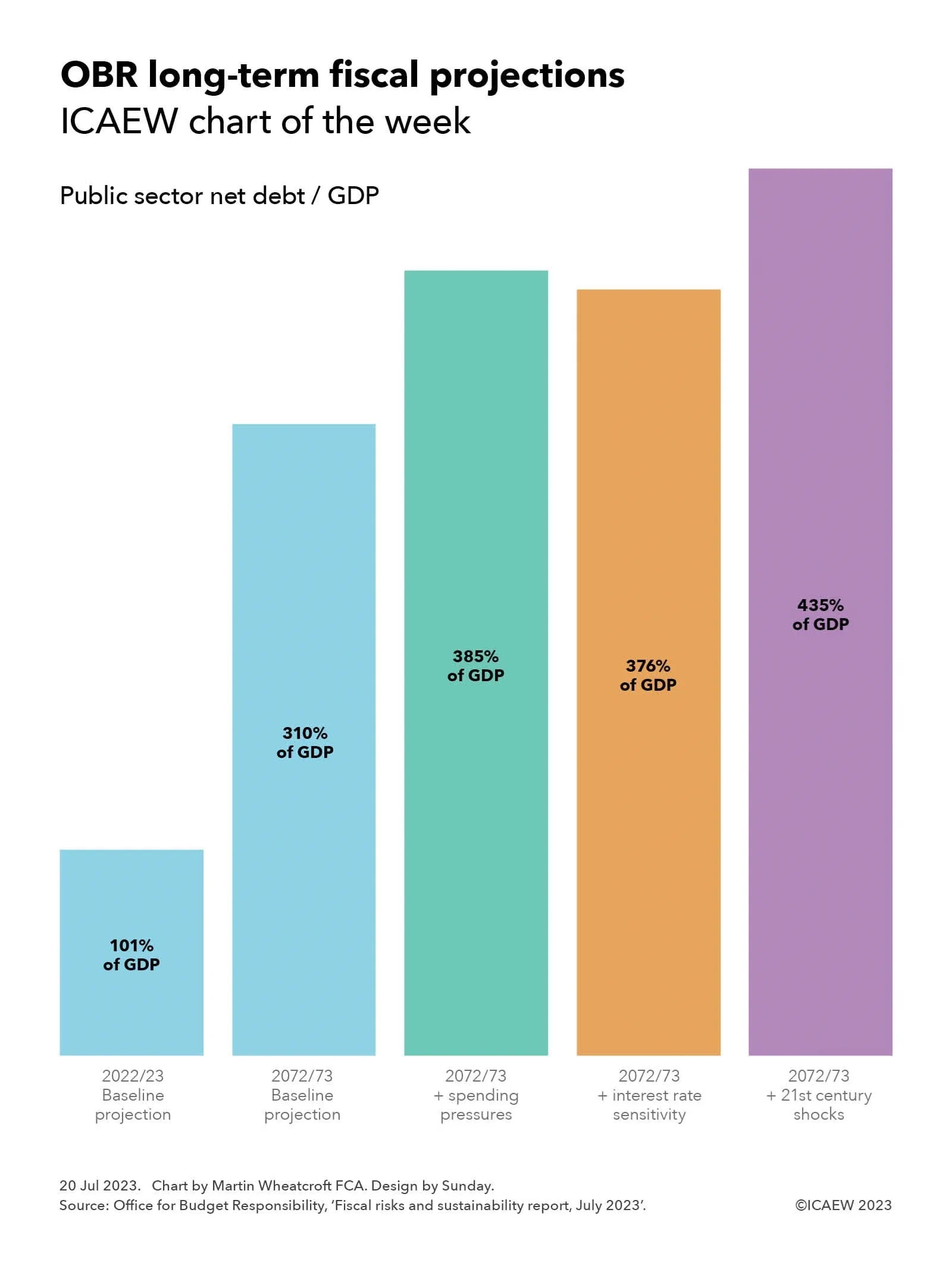

The OBR’s July 2023 fiscal risks and sustainability report indicates that, without higher taxes, public sector net debt as a share of GDP could triple or more over the next 50 years.

The Office for Budget Responsibility (OBR) published its latest fiscal risks and sustainability report on 13 July 2023, providing its analysis of the key risks confronting the UK public finances and long-term fiscal projections for the next 50 years.

This is a sobering report, suggesting that public sector net debt as a share of economic activity as measured by GDP could more than triple between March 2023 and March 2073 – and perhaps go even higher in certain circumstances. The OBR concludes that the public finances are on an unsustainable path.

As illustrated by this week’s chart, the OBR’s baseline projection suggests that the ratio of public sector net debt to GDP could rise from 101% of GDP in 2022/23 to 310% of GDP in 2072/73. The OBR also presented three alternate scenarios: the first is based on higher levels of spending, which could result in the ratio reaching 385% of GDP; one involves higher interest rates, where the ratio might reach 376% of GDP; and a further scenario assuming additional economic shocks, where the ratio might hit 435% of GDP.

The projections are based on the government’s current medium-term fiscal plans as set out in the March 2023 Spring Budget, extrapolated into the future based on existing trends. The starting point is the already high level of public debt that has built up over the past 15 years, together with the current government’s plan to cut spending on public services over the next five years.

The OBR has then overlayed its view of economic growth over the next half century and expected changes in patterns of public spending. This reflects a substantial rise in spending on pensions, health and social care as the proportion of the population in retirement rises, among other drivers that include the financial costs and benefits of delivering net zero. Other key assumptions relate to productivity, demographics (births, deaths and net migration), interest rates and inflation.

The one thing the OBR hasn’t been able to do is to include probable but not enacted tax changes in its projections, with increases in public spending assumed to be financed by higher levels of borrowing instead of the tax rises that future governments are in reality going to opt for.

The projections therefore reflect borrowing that compounds over time to result in some very large headline debt numbers in March 2073, rather than the 1.5% of GDP rise in the tax burden each decade that would, according to the OBR, maintain the debt to GDP ratio at close to its current level.

The fiscal projections calculated by the OBR highlight just how difficult a position the UK’s public finances are in and the major fiscal challenges that will face the incoming government – whoever that may be – after the next general election.