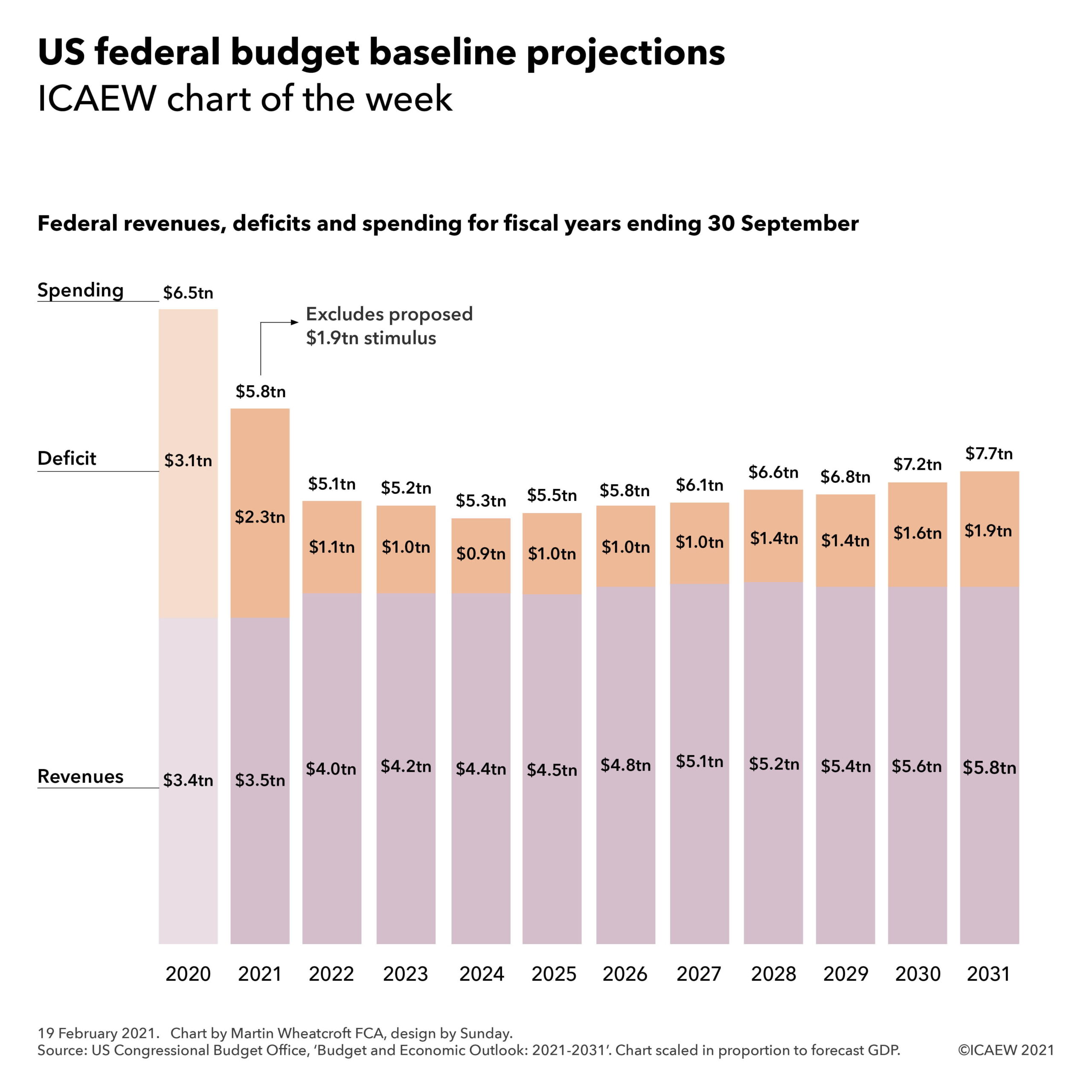

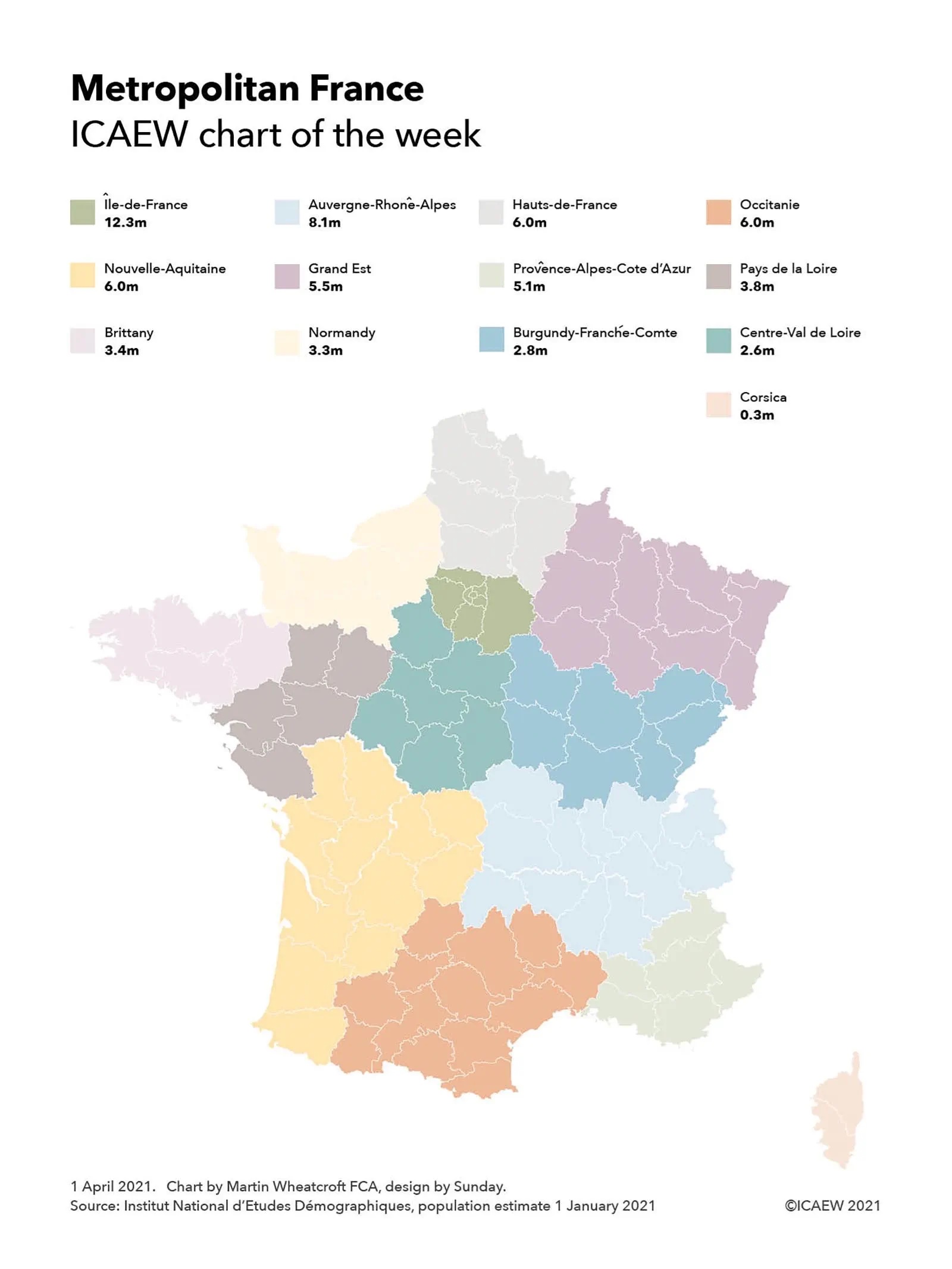

This week’s chart examines how France inserted a layer of regional administration between the national government in Paris and the 96 departments in mainland France and Corsica.

France’s regional tier of government was created in 1982 with 22 regions in Metropolitan France (ie mainland France and Corsica) and has generally seen to be a success. However, it was concluded that there were too many regions, resulting in a consolidation in 2015 into the current 13 regions, as illustrated by the #icaewchartoftheweek.

The regions range in size from the 12.3m population eight-department Île de France that includes Paris, to the 2.6m six-department Centre – Val de Loire region in mainland France and the 0.3m two-department Corsica region. This excludes the five overseas one-department regions of Guadeloupe, French Guiana, Réunion, Martinique and Mayotte.

Regional councils in mainland France and the assembly in Corsica can raise taxes and control substantial budgets, in particular over education and infrastructure investment, as well as having some regulatory powers (but not statutory law-making powers). Elections are on a proportional representation system, with regional presidents chosen by the elected councillors or assembly members.

The establishment of the regions has been part of a process of devolving power from the central government, moving away from the highly centralised control exercised since the French Revolution, which saw the establishment of departments, broadly equivalent to county councils in England. Although each of the 96 departments in Metropolitan France has an elected departmental council and president, many responsibilities for local administration (such as policing) still sit with departmental prefects and subprefects that are appointed by the central government. The lowest tier of local government comprises 36,552 communes, each with an elected council and mayor, with the exception of central Paris, Lyon and Marseille that are further divided into municipal arrondissements.

The comprehensive reforms adopted in France for regional government contrast with the patchwork approach in England, where regional authorities in the form of metropolitan councils were abolished in 1986, only to see a regional tier return in 2000 with the creation of the Greater London Authority. This has been followed over the last decade by the establishment of 10 regional combined authorities, comprising Greater Manchester (2011), Liverpool City Region (2014), Sheffield City Region (2014), North East (2014), West Yorkshire (2014), Tees Valley (2016), West Midlands (2016), West of England (2017), Cambridgeshire & Peterborough (2017) and North of Tyne (2018).

The stop-start approach in England has involved a process of negotiation between central and local government on whether to establish regional combined authorities in particular areas, with a number of proposals across the country under consideration. However, even if they are approved, this will still leave many parts of the country without a regional tier of government. The elections in May in England will therefore see elections for regional authorities only in some areas (including the first-ever elected mayor of West Yorkshire), for between one and three different tiers of local government, and for police & crime commissioners outside of Greater London and Greater Manchester. A rather complex picture!

Back in France, the regional elections scheduled for March have had to be postponed. Instead, a new set of regional administrations across the entirety of Metropolitan France are expected to be elected in June 2021.