My chart for ICAEW this week takes a look at how UK public debt has exploded since the financial crisis to more than quintuple from £0.6trn in March 2008 to a projected £3.1trn in March 2029.

As illustrated by our chart this week, the sums borrowed by the government since the financial crisis of a decade and half ago have been truly astonishing.

In March 2008, the official measure of net debt for the UK public sector was less than £0.6trn. During the financial crisis, government borrowing totalled £0.7trn over a four-year period, causing public sector net debt to more than double to £1.3bn in March 2012.

The eight austerity years saw government cut spending on public services to a significant degree but still borrow a further £0.5trn to see net debt reach £1.8trn in March 2020 – arguably not mending the roof while the sun was shining. This was then followed by an exceptional amount of borrowing during four years of pandemic and energy crisis (including the current financial year) that is expected to see net debt increase by a total of £0.9trn to reach £2.7trn in March 2024.

The Autumn Statement 2023 on Wednesday 22 November saw the Chancellor set out his latest plan for the UK public finances over the next five financial years. This includes a further £0.4trn of borrowing, with public sector net debt projected to amount to £3.1trn in March 2029 – more than quintuple the net amount owed by the UK state 21 years earlier in March 2008.

This assumes that the government can stick to its borrowing plans – many commentators have suggested that planned cuts in spending on public services are unrealistic, meaning more borrowing if taxes are not to rise.

The £2.5trn increase in debt between 2008 and 2029 comprises £2.2trn in borrowing to fund 21 years of deficits (the annual shortfall between receipts and spending) and £0.3trn in other borrowing to fund government lending (such as student loans) and working capital requirements.

As a share of the economy, the increase is less dramatic but still significant – rising from a net debt to GDP ratio of 35.6% in March 2008, to 74.3% in March 2012, to 85.2% in March 2020, to an anticipated 97.9% in March 2024. However, the good news is that net debt / GDP is expected to fall to 94.1% in March 2029 as inflation and economic growth offset the additional borrowing.

The worry for this (or any alternative) government is that while borrowing levels in the OBR’s forecast spreadsheet for the next five years appear manageable and are (just) within the current fiscal rules, the numbers assume that we don’t enter another recession or other economic crisis in that time. Otherwise, we could see debt exploding again.

Monthly public sector finances for October saw spending continue to exceed receipts by a large margin, even if by less than was predicted earlier in the year.

The Office for National Statistics (ONS) released the month public sector finances for October on Tuesday 21 November 2023. It reported a provisional deficit for the month of October of £15bn, bringing the cumulative deficit for the first seven months of the year to £98bn, £22bn more than in the same period last year.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “Although it is positive that the cumulative deficit to October of £98bn is less than the £115bn predicted by the OBR, cash going out continues to exceed cash coming in by a very large margin. Public sector net debt has now exceeded £2.6 trillion for the first time, which is a staggering new record.

“Tomorrow’s Autumn Statement will see the OBR revise and roll forward its forecast, giving the Chancellor so-called headroom to cut taxes or increase spending. But in reality there is no headroom when the public finances continue to be on an unsustainable path without a long-term fiscal strategy to fix them.”

Month of October 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the month of October 2023 was £15bn, made up of tax and other receipts of £85bn less total managed expenditure of £100bn, up 3% and 6% respectively compared with October 2022.

This was the second highest October deficit on record since monthly records began in 1993, following a monthly deficit of £18bn in October 2020 at the height of the pandemic.

Public sector net debt as of 31 October 2023 was £2,644bn or 97.8% of GDP, the first time it has exceeded £2.6trn – only eight months after it first reached £2.5trn.

Seven months to October 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the seven months to October 2023 was £98bn, £22bn more than the £76bn deficit reported for the first seven months of 2022/23. This reflected a widening gap between tax and other receipts for the seven months of £595bn and total managed expenditure of £693bn, up 5% and 8% respectively compared with April to October 2022.

Inflation benefited tax receipts for the first seven months compared with the first half of the previous year, with income tax up 10% to £137bn and VAT up 9% to £117bn. Corporation tax receipts were up 12% to £55bn, partly reflecting the increase in the corporation tax rate from 19% to 25% from 1 April 2023, while national insurance receipts were down by 4% to £99bn because of the abolition of the short-lived health and social care levy last year. Stamp duty on properties was down by 27% to £8bn and the total for all other taxes was up just 3% to £115bn, much less than inflation as economic activity slowed. Non-tax receipts were up 10% to £63bn, primarily driven by higher investment income.

Total managed expenditure of £693bn in the seven months to October 2023 can be analysed between current expenditure excluding interest of £587bn, up £39bn or 7% over the same period in the previous year, interest of £76bn, up £4bn or 5%, and net investment of £30bn, up £9bn or 44%.

The increase of £39bn in current expenditure excluding interest was driven by a £20bn increase in pension and other welfare (including cost-of-living payments), £12bn in higher central government pay, £6bn in additional central government procurement spending, plus £1bn in net other changes.

The rise in interest costs for the seven months of £4bn to £76bn comprises a £18bn or 53% increase to £52bn for interest not linked to inflation as the Bank of England base rate rose, mostly offset by an £14bn or 37% fall to £24bn for interest accrued on index-linked debt from lower inflation than last year.The £9bn increase in net investment spending to £30bn in the first seven months of the current year reflects high construction cost inflation amongst other factors that saw a £11bn or 17% increase in gross investment to £65bn, less a £2bn or 6% increase in depreciation to £35bn.

The cumulative deficit of £98bn is £17bn lower than the Office for Budget Responsibility (OBR)’s official forecast of £115bn for the first seven months of 2023/24 as compiled in March 2023. The OBR is expected to revise its forecast for the full year deficit down from £132bn in tomorrow’s Autumn Statement, but it is still on track to be more than double the £50bn projection for 2023/24 set out in the official forecast from a year earlier (March 2022).

Balance sheet metrics

Public sector net debt was £2,644bn at the end of October 2023, equivalent to 97.8% of GDP.

The debt movement since the start of the financial year was £105bn, comprising borrowing to fund the deficit for the seven months of £98bn plus £7bn in net cash outflows to fund lending to students, businesses and others net of loan repayments together with working capital movements.

Public sector net debt is £829bn more than the £1,815bn reported for 31 March 2020 at the start of the pandemic and £2,106bn more than the £538bn number as of 31 March 2007 before the financial crisis, reflecting the huge sums borrowed over the last couple of decades.

Public sector net worth, the new balance sheet metric launched by the ONS this year, was -£716bn on 31 October 2023, comprising £1,565bn in non-financial assets, £1,029bn in non-liquid financial assets, £2,644bn of net debt (£305bn in liquid financial assets less public sector gross debt of £2,949bn) and other liabilities of £666bn. This is a £102bn deterioration from the -£614bn reported for 31 March 2023.

Revisions

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The latest release saw the ONS revise the reported deficit for the six months to September 2023 up by £1.7bn as estimates of tax receipts and expenditure were updated for better data, while the debt to GDP ratio at the end of September 2023 was revised down by 1.4 percentage points from 97.8% to 96.4% as a consequence of updated estimates of GDP.

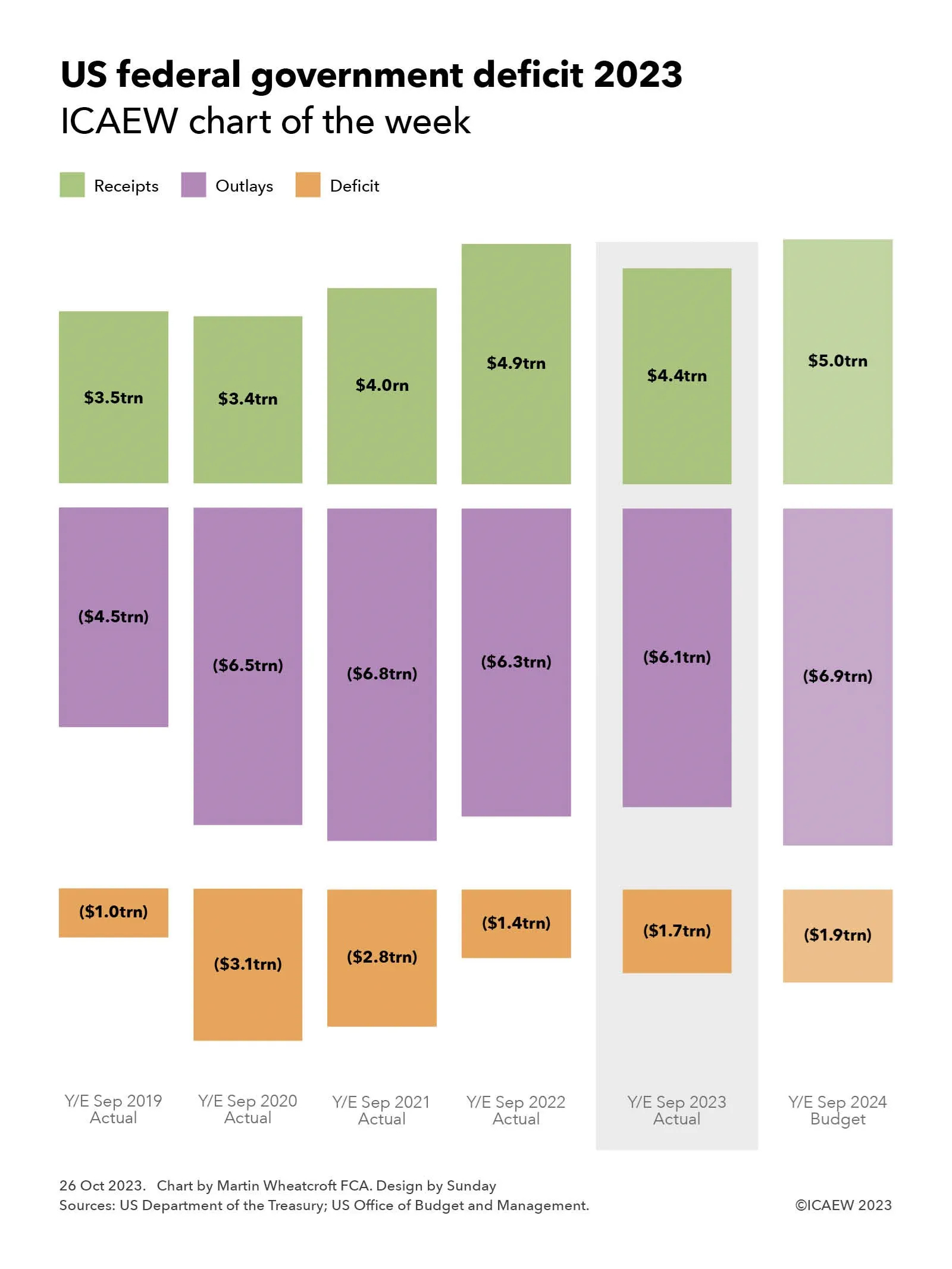

My chart this week looks at the federal deficit of $1.7trn reported by the US government for its recently completed financial year ended 30 September 2023.

The US Department of Treasury published on 20 October 2023 its final monthly treasury statement for the US government’s financial year ended 30 September 2023 (FY2023), enabling our chart this week to look at the actual numbers over the past five years and the budget for the new financial year that started on 1 October.

Our chart illustrates how the deficit increased significantly from the $1.0trn reported for FY2019 ($3.5trn receipts less $4.5trn outlays) to $3.1trn in FY2020 ($3.4trn-6.5trn) and $2.8trn in FY2021 ($4.0trn-$6.8trn) at the height of the pandemic, before falling to $1.4trn in FY2022 ($4.9trn-$6.3trn) as the US economy recovered. The deficit by $0.3trn increased to $1.7trn in FY2023 ($4.4trn-$6.1trn) and is budgeted to increase by a further $0.2trn to $1.9trn in FY2024 ($5.0trn forecast receipts-$6.9trn forecast outlays).

Not shown in the chart is the excess of financial liabilities over financial assets, which increased by $1.7trn from $22.3trn on 30 September 2022 to $24.0trn on 30 September 2023. This differs from ‘debt held by the public’ (the headline measure of federal debt), which increased by $2.0trn from $24.3trn to $26.3trn, more than the federal deficit because of movements in other financial assets and liabilities.

Receipts in FY2023 of $4,439bn comprised $2,176bn in individual income taxes, £1,614bn in social security and retirement contributions, $420bn in corporation income taxes, $80bn in customs duties, $76bn in excise taxes, £34bn in estate and gift taxes and $39bn in other receipts. Outlays for same period of $6,134bn comprised $1,737bn on health and Medicare, $1,354bn on social security, $821bn on defence, $774bn in welfare benefits, $659bn in interest, $302bn for veteran services and benefits, $127bn on transportation, $100bn on commerce, and $260bn on other outlays.

The latter includes the administration of justice, agriculture, community and regional development, education, training, employment and social services, energy, general government, general science, space and technology, international affairs, natural resources and environment, and undistributed offsetting receipts.

These amounts are different from the accruals-based US GAAP federal government financial statements for FY2023 that are expected to be published next April, which will show a much larger accounting loss than the federal deficit reported here. For example, the FY2022 net operating cost (ie accounting loss) of $4.2trn was $2.8trn higher than the federal deficit of $1.4trn for last year, of which the largest difference of $2.6trn related to accruals for federal employee and veteran benefits.

These amounts appear astronomical, especially to those of us living in smaller (and unfortunately) less prosperous countries than the 335m people who live in the US, with its estimated GDP of $26.3trn in FY2023 – equivalent to around $6,600 per person per month.

Federal receipts and outlays in FY2023 represented 17% and 23% of GDP respectively or on a per capita basis were approximately $1,105 and $1,525 per person per month. The federal deficit was therefore equivalent to 6% of GDP or $420 per person per month.

The excess of financial liabilities over financial assets and debt held by the public were 91% and 100% of GDP respectively, equivalent to an amount owed of around $71,500 or $78,500 per person, depending on which measure is used.

Deficit marginally better than had been expected according to the latest figures from the ONS, but costly public sector problems emerge.

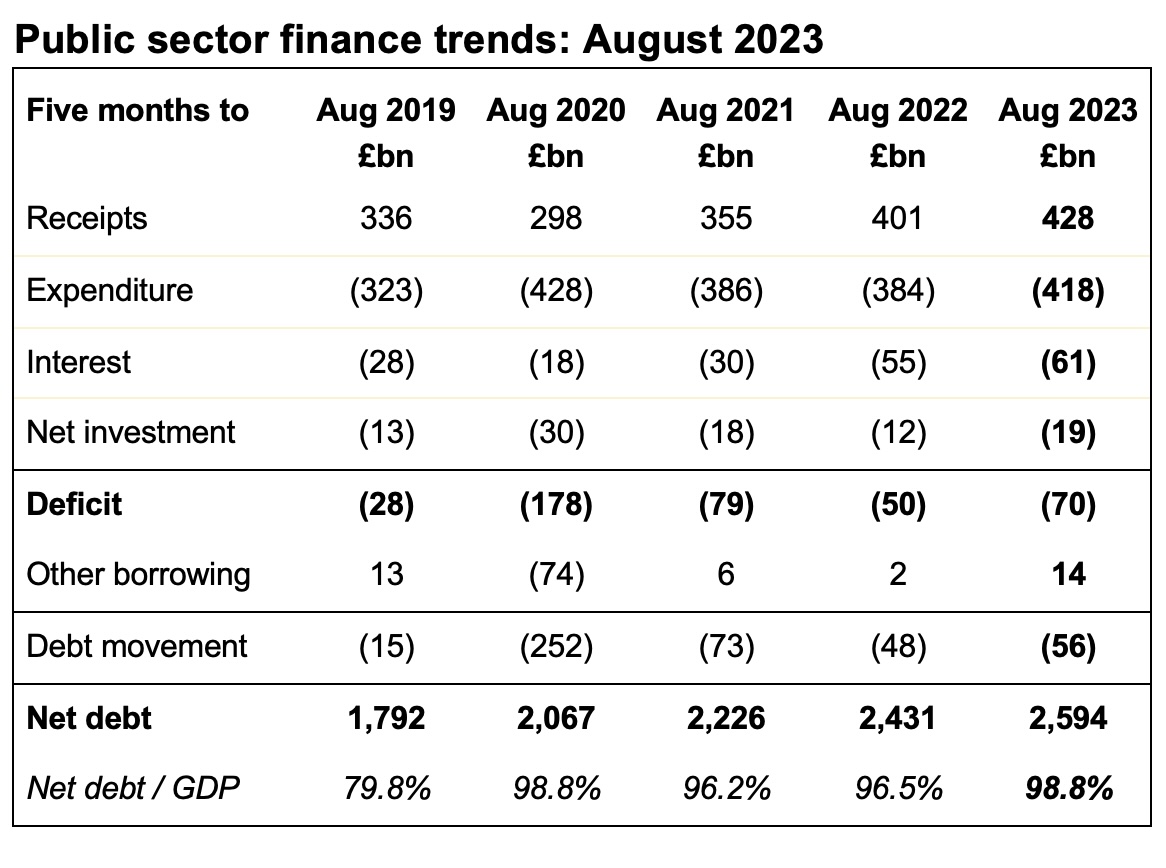

The monthly public sector finances for August 2023 were released by the Office for National Statistics (ONS) on Thursday 21 September 2023. These reported a provisional deficit for the fifth month of the 2023/24 financial year of £12bn, bringing the total deficit for the five months to £70bn, £19bn more than in the same period in the previous year.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “While August’s deficit was marginally better than expected, problems costly to the public sector continue to emerge, from crumbling concrete in public buildings to Birmingham Council’s recent bankruptcy, and are likely to weigh on the Chancellor’s mind as he considers November’s Autumn Statement.

“Both main parties are rightly cautious about making new public spending commitments in the current economic environment, including whether or not to extend the state pension triple lock into the next parliament. Whether they can hold this position as they enter into the party conference season remains to be seen.”

Month of August 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the month of August 2023 was just under £12bn, being tax and other receipts of £84bn less total managed expenditure of £96bn – up 5% and 8% respectively compared with August 2022.

This was the fourth highest August deficit on record since monthly records began in 1993, following the deficits of £14bn in August 2021 and £24bn in August 2020 during the pandemic and £12bn in August 2009 during the financial crisis.

Five months to August 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the five months to August 2023 was £70bn, £20bn more than the £50bn deficit reported for the first five months of 2022/23. This reflected a widening gap between tax and other receipts for the five months of £428bn and total managed expenditure of £498bn, up 7% and 10% respectively compared with April to August 2022.

Inflation benefited tax receipts for the first five months compared with the previous year, with income tax and VAT receipts both up 12% to £104bn and £84bn respectively. However, corporation tax was only up 13% to £37bn despite the increase in the corporation tax rate from 19% to 25% from 1 April 2023, and national insurance receipts were down by 3% to £71bn because of the abolition of the short-lived health and social care levy last year. Stamp duty on properties was down by £2bn or 29% to £6bn and the total for all other taxes was up just 3% to £82bn as economic activity slowed. Non-tax receipts were up 12% to £44bn, primarily driven by higher investment income.

Total managed expenditure of £428bn in the five months to August can be analysed between current expenditure excluding interest of £418bn (up £34bn or 9% over the same period in the previous year), interest of £61bn (up £6bn or 11%), and net investment of £19bn (up £7bn or 57%).

The increase of £34bn in current expenditure excluding interest compared with the prior year has been driven by a £14bn increase in benefit payments, £9bn in higher central government staff costs, £5bn in additional central government procurement spending and £5bn in energy support scheme costs, plus £1bn in net other changes.

The rise in interest costs of £6bn to £61bn reflects a £14bn increase in interest on non-inflation linked debt to £38bn as the Bank of England base rate rose, offset by an £8bn fall in the interest payable on index-linked debt to £23bn as inflation is running at a lower level than it was for the same period last year.

The £7bn increase in net investment spending to £15bn in the first five months of the current year reflects high construction cost inflation among other factors that saw an £8bn or 23% increase in gross investment to £44bn, less a £1bn increase in depreciation to £25bn.

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The latest release saw the ONS revise the reported deficit for the four months to July 2023 up by £2bn as estimates of tax receipts and expenditure were updated for better data, and it also reduced the reported deficit for the 2022/23 financial year by £1bn to £128bn for methodology changes in addition to new data.

The methodology changes also saw small revisions in the reported deficits for previous periods back to 1999, most notably reductions of £1bn to the deficits in 2019/20 and 2020/21 and an increase of £2bn in the reported deficit for 2021/22.

Balance sheet metrics

Public sector net debt was £2,594bn at the end of August 2023, equivalent to 98.8% of GDP.

The debt movement since the start of the financial year was £56bn, comprising borrowing to fund the deficit for the five months of £70bn less £14bn in net cash inflows as loan repayments and positive working capital movements exceeded cash outflows for lending to students, business and others.

Public sector net debt is £779bn or 43% higher than it was on 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic.

Public sector net worth, the new balance sheet metric launched by the Office for National Statistics this year, was -£618bn on 31 August 2023, comprising £1,604bn in non-financial assets, £1,038bn in non-liquid financial assets, £2,594bn of net debt (£339bn in liquid financial assets less public sector gross debt of £2,933bn) and other liabilities of £667bn. This is a £61bn deterioration from the -£557bn reported for 31 March 2023.

This new measure seeks to capture more assets and liabilities than the narrowly focused public sector net debt measure traditionally used to assess the financial position of the UK public sector. However, it excludes unfunded employee pension liabilities that amounted to over £2trn at 31 March 2021 according to the Whole of Government Accounts, although they are expected to be much lower today as discount rates have risen significantly since then.

Higher self-assessment tax receipts and end of energy support payments help improve what is otherwise a disappointing set of numbers.

The monthly public sector finances for July 2023 were released by the Office for National Statistics (ONS) on Tuesday 22 August 2023. These reported a provisional deficit for the fourth month of the 2023/24 financial year of £4bn, bringing the total deficit for the four months to £57bn, £14bn more than in the first third of the previous year.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “These numbers reflect a mixed set of results for the first four months of the financial year, as higher self assessment tax receipts and the end of energy price guarantee support payments led to an improved fiscal situation in July. But debt remains on track to hit £2.7trn by the end of the year, up from £1.8trn before the pandemic, adding to the scale of the challenge facing the government and taxpayers in repairing the public finances.

“Stubbornly high core inflation and the prospect of further interest rate rises will concern the Chancellor as he bears down on public spending in the hope of freeing up the money he needs to both pay for the state pension triple-lock and find room for pre-election tax cuts.”

Month of July 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the month of July 2023 was £4bn, being tax and other receipts of £93bn less total managed expenditure of £97bn, up 5% and 9% respectively compared with July 2022.

This was the fifth-highest July deficit on record since monthly records began in 1993, despite being a £3bn improvement over July 2022, driven by higher self assessment tax receipts and the end of payments under the energy price guarantee.

Four months to July 2023

The provisional shortfall in taxes and other receipts compared with total managed expenditure for the four months to July 2023 was £57bn, £14bn more than the £43bn deficit reported for the first third of the previous financial year (April to July 2022). This reflected a widening gap between tax and other receipts for the four months of £343bn and total managed expenditure of £400bn, up 7% and 10% respectively compared with April to July 2022.

Inflation benefited tax receipts for the four months, with income tax up 13% to £85bn and VAT up 9% to £65bn. The rise in corporation tax, up 17% to £30bn, reflected both inflation and the increase in the corporation tax rate to 25% from 1 April 2023. However, national insurance receipts were down by 3% to £57bn because of the abolition of the short-lived health and social care levy last year, while the total for all other taxes was down by 1% to £69bn as economic activity slowed. Other receipts were up 17% to £37bn, driven by higher investment income.

Total managed expenditure of £400bn in the four months to July can be analysed between current expenditure excluding interest of £334bn (up £26bn or 8% over the same period in the previous year), interest of £51bn (up £7bn or 16%), and net investment of £15bn (up £4bn or just over a third).

The increase of £26bn in current expenditure excluding interest compared with the prior year has been driven by £11bn from the uprating of benefit payments, £8bn in higher central government staff costs, £3bn in central government procurement and £5bn in energy support scheme costs, less £1bn in net other changes.

The rise in interest costs of £7bn to £51bn reflects a fall in the interest payable on index-linked debt of £6bn from £30bn to £24bn as inflation has moderated compared with the same period last year, combined with a £13bn increase in interest on non-inflation linked debt from £14bn to £27bn as the Bank of England base rate rose.

The £4bn increase in net investment spending to £15bn in the first four months of the current year reflects high construction cost inflation among other factors that saw a £5bn or 17% increase in gross investment to £35bn, less a £1bn increase in depreciation to £20bn.

Public sector finance trends: July 2023

Four months to

Jul 2019 (£bn)

Jul 2020 (£bn)

Jul 2021 (£bn)

Jul 2022 (£bn)

Jul 2023 (£bn)

Receipts

270

234

282

320

343

Expenditure

(259)

(348)

(310)

(308)

(334)

Interest

(24)

(15)

(23)

(44)

(51)

Net investment

(10)

(26)

(13)

(11)

(15)

Deficit

(23)

(155)

(64)

(43)

(57)

Other borrowing

4

(66)

(22)

5

10

Debt movement

(19)

(221)

(86)

(38)

(47)

Net debt

1,796

2,036

2,239

2,420

2,579

Net debt / GDP

80.1%

96.9%

97.7%

96.6%

98.5%

Source: ONS, ‘Public sector finances, July 2023’.

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled. The latest release saw the ONS revise the reported deficit for the three months to June 2023 down by £2bn as estimates of tax receipts and expenditure were updated for better data, as well as reduce the reported deficit for the 2022/23 financial year by £1bn from £132bn to £131bn for similar reasons. The ONS also revised its estimates of GDP for more recent economic data, resulting in a lower reported net debt / GDP ratio.

Balance sheet metrics

Public sector net debt was £2,579bn at the end of July 2023, equivalent to 98.5% of GDP.

The debt movement since the start of the financial year was £47bn, comprising borrowing to fund the deficit for the four months of £57bn plus £10bn in net cash inflows as loan repayments and positive working capital movements exceeded cash outflows for lending to students, business and others.

Public sector net debt is £764bn or 42% higher than it was on 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic.

Public sector net worth, the new balance sheet metric launched by the Office for National Statistics this year, was -£631bn on 31 July 2023, comprising £1,604bn in non-financial assets, £1,011bn in non-liquid financial assets and £336bn in liquid financial assets less public sector gross debt of £2,915bn and other liabilities of £667bn. This is a £54bn deterioration from the -£577bn reported for 31 March 2023.

This new measure seeks to capture more assets and liabilities than the narrowly focused public sector net debt measure traditionally used to assess the financial position of the UK public sector. However, it excludes unfunded employee pension liabilities that amounted to more than £2trn at 31 March 2021 according to the Whole of Government Accounts, although they are expected to be much lower today as discount rates have risen significantly since then.

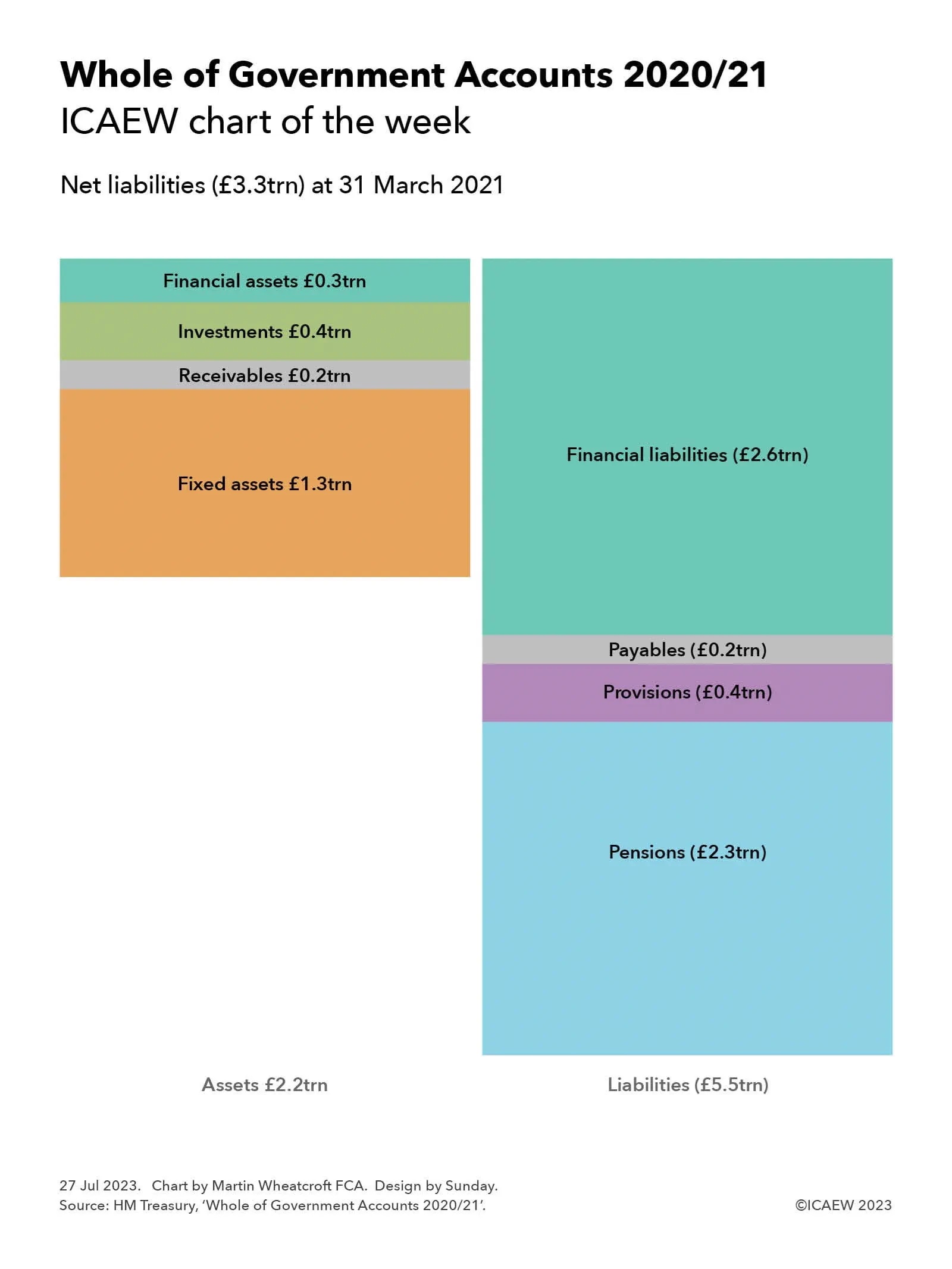

My chart this week looks at the £3.3trn of net liabilities presented in the UK government’s consolidated financial statements for the year ended 31 March 2021 that were finally published more than 27 months after the balance sheet date.

The UK’s Whole of Government Accounts for the year ended 31 March 2021 were published and submitted to Parliament on 20 July 2020, more than 27 months after the balance sheet date. These are consolidated financial statements prepared in accordance with International Financial Reporting Standards (IFRS) that incorporate the financial results of more than 10,000 public bodies in the UK across central government, local government, and other parts of the public sector.

The Whole of Government Accounts provide a much more comprehensive picture of the financial performance and position of the UK public sector than is presented in the statistics-based National Accounts, using a financial language familiar to millions of users of financial reports in the private sector.

As our chart this week highlights, the statement of financial position (balance sheet) of the UK public sector at 31 March 2021 was in heavily negative territory with £3.3trn in net liabilities, comprising assets of £2.2trn less liabilities of £5.5trn. This compares with net liabilities of £2.8trn a year earlier.

Assets of £2.2trn comprised £1.3trn in tangible and intangible fixed assets, £0.2trn in receivables and other non-financial assets, £0.4trn in non-current investments and £0.3trn in cash and other current financial assets. Liabilities of £5.5trn comprised £2.6trn in debt and other financial liabilities, £0.2trn in payables, £0.4trn in provisions and £2.3trn in net pension obligations.

Fixed assets of £1,313bn consisted of infrastructure assets of £677bn, land and buildings of £409bn, plant and equipment of £184bn, and intangible assets of £41bn. Receivables and other non-financial assets of £218bn comprised £164bn in tax receivable and accrued, £39bn in other receivables, prepayments and accruals, and £15bn in inventories. Non-current investments of £360bn comprised £152bn in loans and deposits, £85bn in student loans, £44bn in equities, £60bn in other financial investments, £16bn in investment properties, and £3bn in assets held for sale. Cash and other current financial assets of £317bn comprised £40bn in cash and cash equivalents, £12bn in gold, £129bn in debt securities, £101bn in loans and deposits, and £35bn of other financial assets.

Debt and other financial liabilities of £2,639bn comprised £1,265bn in externally held gilts, £203bn in direct borrowing from the public through National Savings & Investments, £53bn in short-term treasury bills, £815bn in Bank of England deposits, £84bn in bank and other borrowing, £85bn in banknotes, £27bn in derivatives, £20bn in financial guarantees, and £87bn in other financial liabilities. Payables of £221bn comprised £44bn in trade and other payables, £81bn in accruals and deferred income, £55bn in tax refunds, and £41bn on PFI, finance leases and other contracts. Provisions of £366bn consisted of £159bn for nuclear decommissioning, £87bn for clinical negligence, £36bn for payments to the EU, £29bn for the Pension Protection Fund, and £55bn in other provisions for liabilities and charges. Net public sector pension obligations of £2,306bn comprised £2,168bn in unfunded pension obligations (including £792bn for the NHS, £501bn for teachers, £339bn for the civil service, £254bn for the armed forces, £209bn for police and fire services, and £73bn other) and a net £138bn (£479bn of obligations less £341bn in fund assets) for local government and other funded pension schemes.

Not shown in the chart is the revenue and expenditure statement, which reported revenue of £732, expenditure of £1,063bn and finance and other items of £73bn to give a net accounting loss for the year of £404bn – more than twice the £192bn loss reported for the pre-pandemic year. The financial statements covered the first year of the coronavirus pandemic, which saw income fall and costs soar, resulting in net borrowing during the year of £524bn according to the cash flow statement.

The Whole of Government Accounts is probably the most important report published by the UK government each year, but you wouldn’t have known that by the lack of fanfare on its publication amid the wave of hundreds of other documents released ahead of the parliamentary recess. This may be driven by understandable embarrassment by the length of time it has taken to prepare them – more than 27 months after the balance sheet date compared with the nine months that is its long-term aim – as well as by the gaps in preparation caused by local authorities and other public bodies that are substantially behind in producing their individual financial statements, leading to an additional audit qualification for completeness this year.

Despite that, and the other audit qualifications that highlight problems with the numbers reported, every citizen ideally should read the Whole of Government Accounts 2020/21. After all, it tells the financial story of the most dramatic year in recent history.

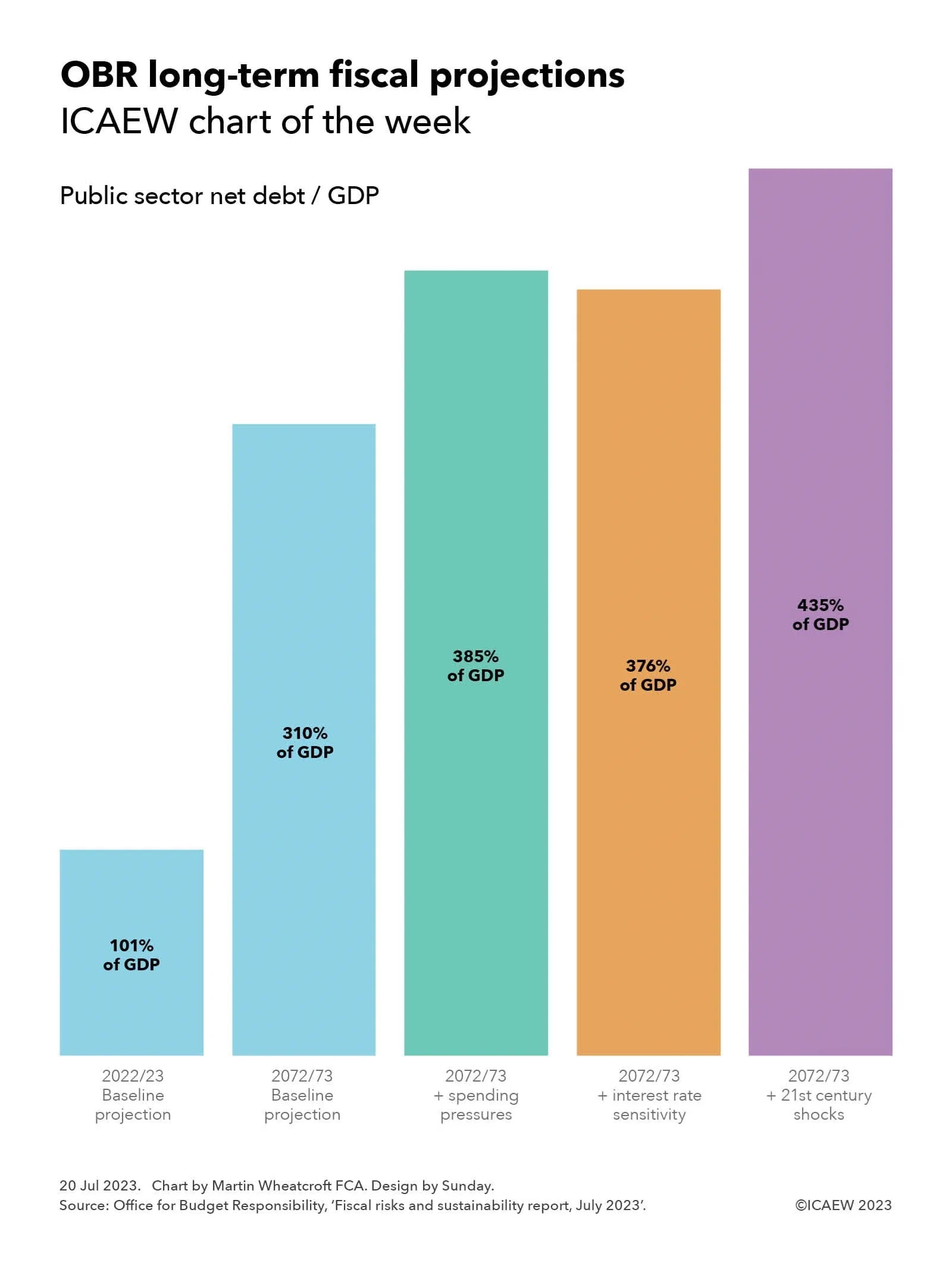

The OBR’s July 2023 fiscal risks and sustainability report indicates that, without higher taxes, public sector net debt as a share of GDP could triple or more over the next 50 years.

The Office for Budget Responsibility (OBR) published its latest fiscal risks and sustainability report on 13 July 2023, providing its analysis of the key risks confronting the UK public finances and long-term fiscal projections for the next 50 years.

This is a sobering report, suggesting that public sector net debt as a share of economic activity as measured by GDP could more than triple between March 2023 and March 2073 – and perhaps go even higher in certain circumstances. The OBR concludes that the public finances are on an unsustainable path.

As illustrated by this week’s chart, the OBR’s baseline projection suggests that the ratio of public sector net debt to GDP could rise from 101% of GDP in 2022/23 to 310% of GDP in 2072/73. The OBR also presented three alternate scenarios: the first is based on higher levels of spending, which could result in the ratio reaching 385% of GDP; one involves higher interest rates, where the ratio might reach 376% of GDP; and a further scenario assuming additional economic shocks, where the ratio might hit 435% of GDP.

The projections are based on the government’s current medium-term fiscal plans as set out in the March 2023 Spring Budget, extrapolated into the future based on existing trends. The starting point is the already high level of public debt that has built up over the past 15 years, together with the current government’s plan to cut spending on public services over the next five years.

The OBR has then overlayed its view of economic growth over the next half century and expected changes in patterns of public spending. This reflects a substantial rise in spending on pensions, health and social care as the proportion of the population in retirement rises, among other drivers that include the financial costs and benefits of delivering net zero. Other key assumptions relate to productivity, demographics (births, deaths and net migration), interest rates and inflation.

The one thing the OBR hasn’t been able to do is to include probable but not enacted tax changes in its projections, with increases in public spending assumed to be financed by higher levels of borrowing instead of the tax rises that future governments are in reality going to opt for.

The projections therefore reflect borrowing that compounds over time to result in some very large headline debt numbers in March 2073, rather than the 1.5% of GDP rise in the tax burden each decade that would, according to the OBR, maintain the debt to GDP ratio at close to its current level.

The fiscal projections calculated by the OBR highlight just how difficult a position the UK’s public finances are in and the major fiscal challenges that will face the incoming government – whoever that may be – after the next general election.

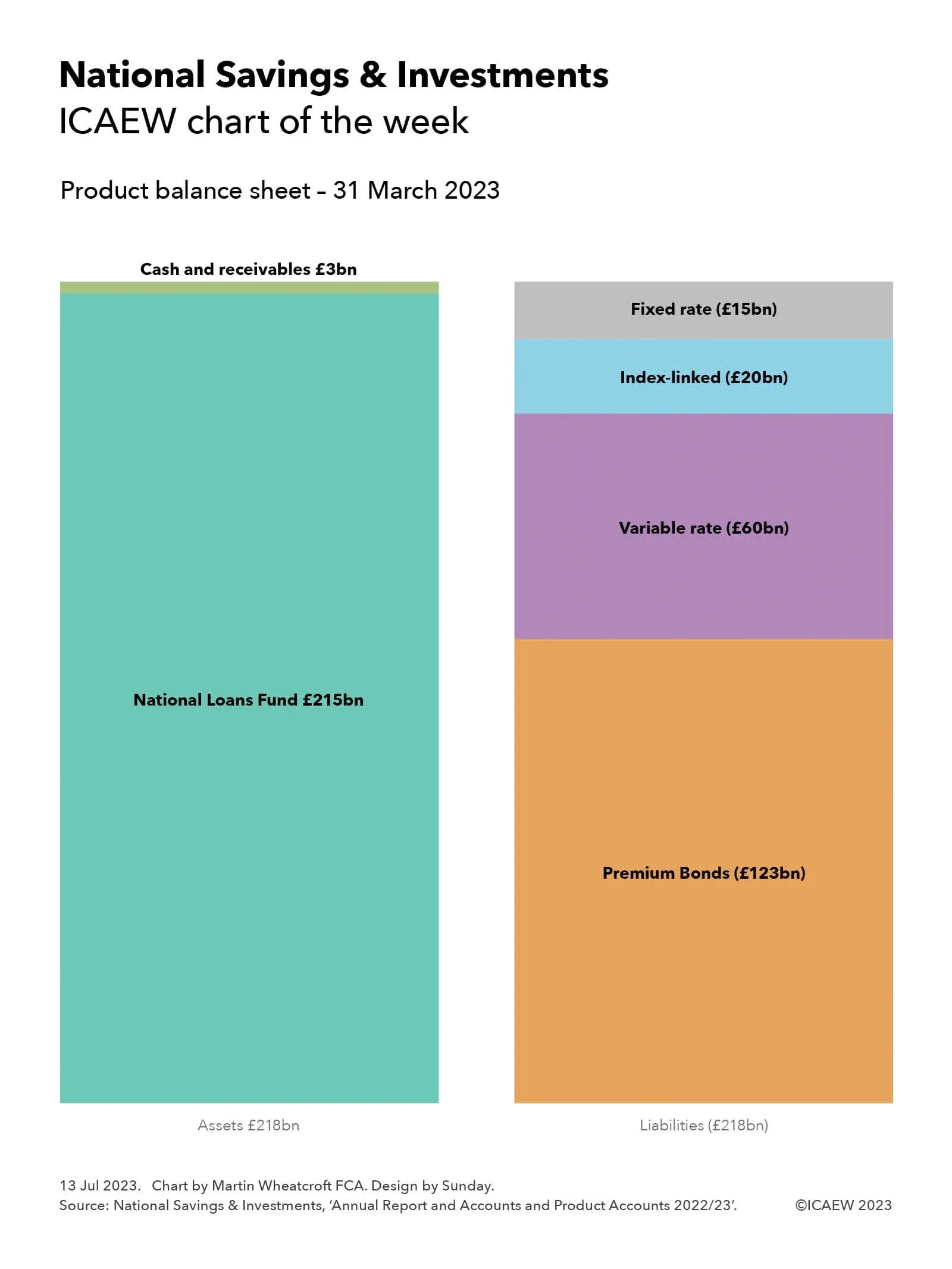

My chart this week is on the £218bn balance sheet of the state-owned retail financial institution that borrows from the public to help fund the UK government.

While the bulk of the UK national debt is financed through the sale of government bonds primarily purchased by institutional investors, the UK government also borrows money directly from the public through its in-house ‘bank’, National Savings & Investments (NS&I).

Originally established as the Post Office Savings Bank in 1861, NS&I has a long history of funding the UK government, for example through the sale of war bonds direct to the public in the twentieth century. Today it is a non-ministerial department for its banking or ‘product’ activities, managed by an executive agency of HM Treasury of the same name.

As my chart this week illustrates, NS&I’s product assets as of 31 March 2023 of £218bn were balanced by its liabilities. As a government-backed financial institution, it is not technically a bank and so does not need to maintain equity reserves, unlike commercial banks.

The primary job of NS&I is to attract money from the public to help finance the government’s operations, with a total of £215bn lent to the National Loans Fund as of 31 March 2023. This lending formed the bulk of the NS&I’s product assets, with the balance of assets of £3bn comprising mostly cash together with some receivables.

Liabilities of £218bn on 31 March 2023 were owed to depositors, comprising £123bn in Premium Bonds, £60bn in other variable rate savings products, an estimated £20bn in Index-Linked Savings Certificates, and £15bn in fixed-interest certificates and bonds.

Premium Bonds were introduced in 1956 and (from the NS&I’s perspective) pay a variable rate of interest (currently 4.00%). From a savers’ perspective, however, bonds do not attract any interest at all and instead represent a refundable ticket to a regular tax-free prize draw, with a 22,000 to 1 chance of winning a prize each month, ranging from £25 up to £1m.

Other variable rate savings products include £32bn in on demand Direct Saver accounts that pay interest monthly (currently 3.40% gross/3.45% AER), £20bn on demand Income Bonds paid annually (currently 3.40%), £5bn in ISAs (paying 2.40%) and Junior ISAs (paying 3.65%), and £3bn in Investment Account (paying 0.85%) and legacy savings products that pay either 0.25% or 0%.

Index-Linked Savings Certificates of approximately £20bn (the exact number is not disclosed) are no longer on sale. They are of three years’ duration and can be rolled over by existing holders. These typically attract interest equivalent to Consumer Price Inflation + 0.01% AER, a very low amount in the last decade, but of course much more recently.

Fixed rate liabilities of £15bn principally comprise £12bn in Guaranteed Bonds, £2bn in Fixed Interest Savings Certificates and £1bn in Green Savings Bonds. Guaranteed Bonds are one-year fixed-term fixed interest accounts, with Guaranteed Income Bonds that today pay 3.90% gross/3.97% AER in monthly instalments and Guaranteed Growth Bonds that pay 4.00% on maturity, higher than previous issues. Three-year Fixed Interest Savings Certificates are no longer on sale but can be rolled over by existing holders, however savers can opt instead for three-year Green Savings Bonds, with issue 4 on sale at a fixed interest rate of 4.20% credited annually.

The above numbers do not include NS&I’s separate executive agency operational balance sheet that comprised £0.18bn in assets, £0.15bn in liabilities and equity of £0.03bn on 31 March 2023.

The £218bn lent by the public to NS&I is equivalent to 7.7% of public sector gross debt of £2,836bn on 31 March 2023. While this may seem relatively small in comparison to the £1,320bn in British government securities (gilts) and other debt securities and loans that have been raised from institutional debt investors, or the £1,298bn in currency and central bank deposit liabilities, NS&I provides both a useful public service and a useful alternative source of funding.

Prime Minister Henry Temple (Viscount Palmerston) and Chancellor of the Exchequer William Gladstone would no doubt be extremely pleased to see that their creation was still funding the nation 162 years on. Even if, with £10bn in net new deposits received during the year ended 31 March 2023, it is an increasing liability.

The public finances continue to be battered by economic shocks as this week’s chart on the past five years of red ink illustrates.

The monthly public sector finances for March 2023 released on Tuesday 25 April contained the first cut of the government’s financial result for 2022/23, with our chart this week illustrating trends over the past five years in receipts, expenditure and the deficit.

As our chart highlights, tax and other receipts increased from £813bn in 2018/19 to £827bn in 2019/20, before falling to £793bn during the first year of the pandemic. They recovered to £920bn in 2021/22 before rising with inflation to a provisional estimate of £1,016bn for the year ended 31 March 2023.

Total managed expenditure (TME) increased from £857bn in 2018/19 to £888bn in 2019/20, before exceeding £1trn for the first time in 2020/21 as the pandemic caused expenditure to rise significantly. TME fell in 2021/22 to £1,041bn as pandemic-released spending was scaled back, before rising this year to £1,155bn as inflation, higher interest rates and energy support packages more than offset the pandemic related spending that was not repeated in 2022/23.

The deficit of £44bn in 2018/19 was the lowest it had been since the financial crisis, following an extended period of spending restraint over a decade. The purse strings were loosened a little in 2019/20 as previous government plans to eliminate the deficit were abandoned, with the deficit rising to £61bn. The huge cost of the pandemic saw the deficit rise to £313bn in 2020/21 as the borrowing rose to meet the huge costs of dealing with the pandemic, before falling back to £121bn in 2021/22.

There were hopes that the situation would improve further, with the government in October 2021 budgeting for a deficit of £83bn. Unfortunately, rampant inflation and the energy crisis following Russia’s invasion of Ukraine mean that the government does not currently expect to reduce the deficit to below £50bn until 2027/28 at the earliest. And that is with what some commentators believe are unrealistic assumptions about the government’s ability to reduce spending on public services beyond the cuts already delivered.

Provisional receipts in 2022/23 were 25% higher than the outturn for 2018/19, which in the absence of economic growth has principally been driven by inflation of around 15% over that period combined with an increase in the level of taxation and other receipts from around 37% to approaching 41% of the economy. Total managed expenditure is provisionally 35% higher than in 2018/19, although this includes substantial amounts of one-off expenditures on the energy support packages and index-linked debt interest that should moderate, at least assuming inflation reduces in the coming financial year.

Not shown in the chart is what these numbers mean for public sector net debt, which has increased by £753bn over the past five years from £1,757bn at 1 April 2018 to a provisional £2,530bn at 31 March 2023. This comprises £678bn in borrowing to fund the deficits shown in the chart, and £75bn to fund lending by government and working capital requirements.

Our chart this week may be well presented, but it is not a pretty picture.

February fiscal deficit hits £17bn, while the cumulative deficit for 11 months of £132bn doesn’t include backdated public sector pay awards.

The monthly public sector finances for February 2023 released on Tuesday 21 March 2023 reported a provisional deficit for the month of £17bn, which is a return to red after a surplus of £8bn last month in January 2023.

The deficit was £10bn more than the £7bn deficit reported for the same month last year (February 2022), as higher interest costs, higher inflation on index-linked debt, and the cost of the energy price guarantee for households and businesses incurred during the month drove up the need to borrow.

The cumulative deficit for the first 11 months of the financial year was £132bn, which is £15bn more than in the same period last year but £155bn lower than in 2020/21 during the first stages of the pandemic. It was £78bn more than the deficit of £54bn reported for the first 11 months of 2019/20, the most recent pre-pandemic pre-cost-of-living-crisis comparative period.

The reported deficit does not reflect backdated public sector pay settlements that have been or are expected to be agreed in March 2023, although the numbers are broadly in line with the £152bn estimated deficit for the full year in the Office for Budget Responsibility (OBR)’s revised forecasts made at the time of the Spring Budget. This was lower than their previous forecast of £177bn in November, primarily because the energy price guarantee is costing less than anticipated.

Public sector net debt was £2,507bn or 99.2% of GDP at the end of February 2023. This is £692bn higher than net debt of £1,815bn on 31 March 2020, reflecting the huge sums borrowed since the start of the pandemic. The OBR’s latest forecast is for net debt to reach £2,546bn by March 2023 and to exceed £2.9trn by March 2028.

Tax and other receipts in the 11 months to 28 February 2023 amounted to £924bn, £91bn or 11% higher than a year previously. Higher income tax and national insurance receipts were driven by rising wages and the higher rate of national insurance for part of the year, while VAT receipts benefited from inflation in retail prices.

Expenditure excluding interest and investment for the 11 months of £888bn was £52bn or 6% higher than the same period in 2021/22, with Spending Review planned increases in spending, the effect of inflation, and the cost of energy support schemes partially offset by the furlough programmes and other pandemic spending in the comparative period not being repeated this year.

Interest charges of £120bn for the 11 months were £51bn or 73% higher than the £69bn reported for the equivalent period in 2021/22, through a combination of higher interest rates and higher inflation driving up the cost of RPI-linked debt.

Cumulative net public sector investment to February was £48bn, £4bn more than this time last year. This is much less than might be expected given the Spending Review 2021 pencilled in significant increases in capital expenditure budgets in the current year.

The increase in net debt of £125bn since the start of the financial year comprised borrowing to fund the deficit for the 11 months of £132bn, less £7bn in net cash inflows from repayments of deferred taxes, and loans made to businesses during the pandemic, less funding for student, business and other loans together with working capital requirements.

Alison Ring OBE FCA, Public Sector and Taxation Director for ICAEW, said: “The public finances are back in the red this month as a deficit of £17bn brings the total for the 11 months to February to £132bn, with public sector net debt in excess of £2.5trn. Although broadly in line with the OBR’s improved estimate accompanying the Spring Budget, the numbers don’t reflect the cost of backdated public sector pay settlements to be recorded in the final month of the 2022/23 financial year.

“The chancellor still needs to top up departmental budgets for pay awards in the next financial year, reducing his capacity to address inflationary cost pressures in other areas. HS2 may not be the only capital programme at risk of being scaled back or delayed as he seeks to make savings.”

Caution is needed with respect to the numbers published by the ONS, which are expected to be repeatedly revised as estimates are refined and gaps in the underlying data are filled.

The ONS made several revisions to prior period fiscal numbers to reflect revisions to estimates. These had the effect of reducing the reported fiscal deficit for the 10 months ended 31 January 2023 by £1bn to £116bn.

![Exploding debt

Step chart showing how UK public sector net has changed between March 2008 and the projected position in March 2029.

[debt bars shaded orange, changes shaded in purple]

March 2008: £0.6trn

Financial crisis: +£0.7trn

March 2012: £1.3trn

Austerity years: +£0.5trn

March 2020: £1.8trn

Pandemic / energy crisis: +£0.9trn

March 2024: £2.7trn

[bar colours shaded by 50% to indicate the following are projected numbers]

Latest plan: +£0.4trn

March 2029: £3.1trn

30 Nov 2023.

Chart by Martin Wheatcroft FCA. Design by Sunday.

Source: OBR, 'Public finances databank - Nov 2023'.](https://martinwheatcroft.com/wp-content/uploads/2023/11/icaewchart286debt.jpg)

![Public sector finance trends: October 2023

Table showing receipts, expenditure, interest, net investment, deficit, other borrowing and debt movement for the seven months to October 2023 plus net debt and net debt / GDP at 31 October 2023.

Receipts: £466bn (Oct 2019), £425bn (Oct 2020), £500bn (Oct 2021), £565bn (Oct 2022), £595bn (Oct 2023)

Expenditure: (£457bn), (£582bn), (£536bn), (£548bn), (£587bn)

Interest: (£38bn), (£26bn), (£41bn), (£72bn), (£76bn)

Net investment: (£20bn), (£42bn), (£28bn), (£21bn), (£30bn)

[line above subtotal]

Deficit: (£49bn), (£225bn), (£105bn), (£76bn), (£98bn)

Other borrowing: £5bn, (£61bn), (£61bn), £5bn, (£7bn)

[line above total]

Debt movement: (£44bn), (£286bn), (£166bn), (£71bn), (£105bn)

[line below total]

Net debt: £1,821bn, £2,101bn, £2,319bn, £2,454bn, £2,644bn.

Net debt / GDP: 82.1%, 99.3%, 97.5%, 95.5%, 97.8%](https://martinwheatcroft.com/wp-content/uploads/2023/11/2023-10-Trends.jpg)