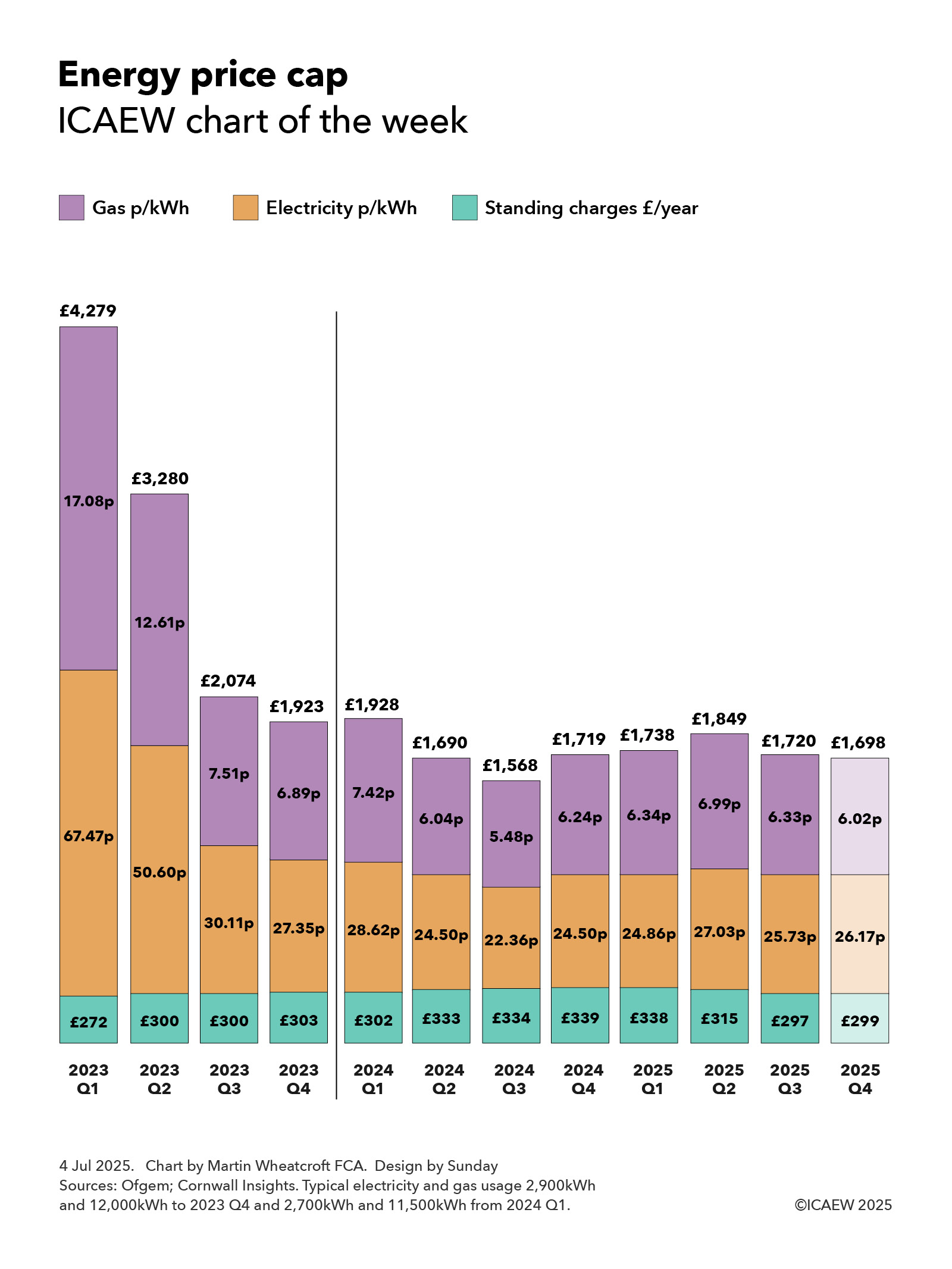

My chart for ICAEW this week looks at the domestic energy price cap since its peak in the first quarter of 2023.

According to Ofgem, the domestic energy price cap in Great Britain for the third quarter of 2025 commencing on 1 July is £1,720 per year. This is a 7% reduction from the £1,849 per year price cap in the previous quarter, based on typical energy usage of 2,700kWh of electricity per year and 11,500kWh of gas per year.

The above statement may be confusing because the amounts quoted are not what is capped and the price cap only lasts for a quarter rather than a year.

There is, however, a method to Ofgem’s madness. There are actually 252 price caps set by Ofgem each quarter that it distils into one headline number, being the average of fourteen regional prices for a dual-fuel standard credit user multiplied by typical annual usage plus the 5% VAT that is payable on domestic energy supplies.

This single annualised number makes it much easier to communicate what is happening to energy prices and also avoids getting into the complications of seasonal variations in energy usage during the course of each year.

The 252 price caps comprise two caps – a maximum per kWh price and a maximum daily standard charge – for each of three different types of users (single-rate users of electricity, multi-rate ‘Economy 7’ users of electricity and users of gas), multiplied by three different categories of customers (standard credit, direct debit and prepayment meters), and then multiplied by 14 regional variations

The headline price cap is not the maximum that households will pay in a year, nor should you divide by four to guess at the amount payable for that individual quarter. Those paying by direct debit or using prepayment meters (since July 2023, previously prepayment customers paid more) are capped at 7% and 10% on average less than standard credit users based on typical usage, while maximum prices and standing charges also vary by region. Larger homes are likely to use much more energy and so pay a lot more, while smaller homes are likely to pay less.

Meanwhile, energy suppliers have started to offer annual or longer fixed-rate deals again, typically at a discount to the current maximum prices but with the price protection that such deals offer offset by the risk that the fixed-rate in the deal could exceed the price cap in subsequent quarters if prices go down.

As my chart this week illustrates, the annual price cap peaked at £4,279 in the first quarter of 2023, based on average maximum standing charges of £272 per year for both electricity and gas meters, plus 2,900kWh of electricity at 67.47p and 12,000kWh of gas at 17.08p. The price cap fell to £3,280 in the second quarter (£300 standing charges, 50.60p/kWh for electricity and 12.61p/kWh for gas), £2,074 in the third quarter (£300, 30.11p/kWh and 7.51p/kWh) and £1,923 in the fourth quarter of 2023 (£303, 27.35p/kWh and 6.89p/kWh).

Ofgem changed its estimate of typical annual usage to 2,700kWh in electricity and 11,500kWh in gas from the first quarter of 2024, so the £1,928 headline price cap was actually a 3% increase compared with the previous quarter once the change is adjusted for. The price cap fell to £1,690 in the second quarter (£333 standing charges, 24.50p/kWh for electricity and 6.04p/kWh for gas) and £1,568 in the third quarter (£334, 22.36p/kWh and 5.48p/kWh) before rising to £1,179 in the fourth quarter of 2024 (£339, 24.50p/kWh and 6.24p/kWh).

Prices rose in the first quarter of 2025 to £1,738 (£338 standing charges, 24.86p/kWh for electricity and 6.34p/kWh for gas) and £1,849 in the second quarter (£315, 27.03p and 6.99p) before falling to £1,720 in the current quarter that commenced on 1 July and ends on 30 September 2025 (£297, 25.73p/kWh and 6.33p/kWh).

Cornwall Insight projects that the price cap could fall slightly to £1,698 in the fourth quarter (£299 standing charges, 26.17p/kWh and 6.02p/kWh) based on data up to 29 June 2025. However, this could easily change depending on what happens to wholesale prices over the next month and a half before Ofgem sets the next quarterly price cap on 27 August 2025.

Despite the significant fall in energy prices from their peak in the first quarter of 2023, the cap continues to be much higher than it was before the pandemic and the cost-of living crisis. After adjusting for consumer price inflation and changes in estimated typical usage, the £1,720 per year price cap in the current quarter is approximately 26% higher than the original price cap of £1,137 in the first quarter of 2019 (not shown in the chart, based on £177 a year in standing charges, 16.52p/kWh x 3,100kWh typical annual usage of electricity and 3.73p/kWh x 12,000kWh of gas).

While it is positive that energy prices appear to have stabilised at around the current level over the past couple of years, there continue to be significant geopolitical risks that mean that prices could rise significantly in some specific scenarios.

Time to keep our fingers crossed and hope those risks don’t materialise