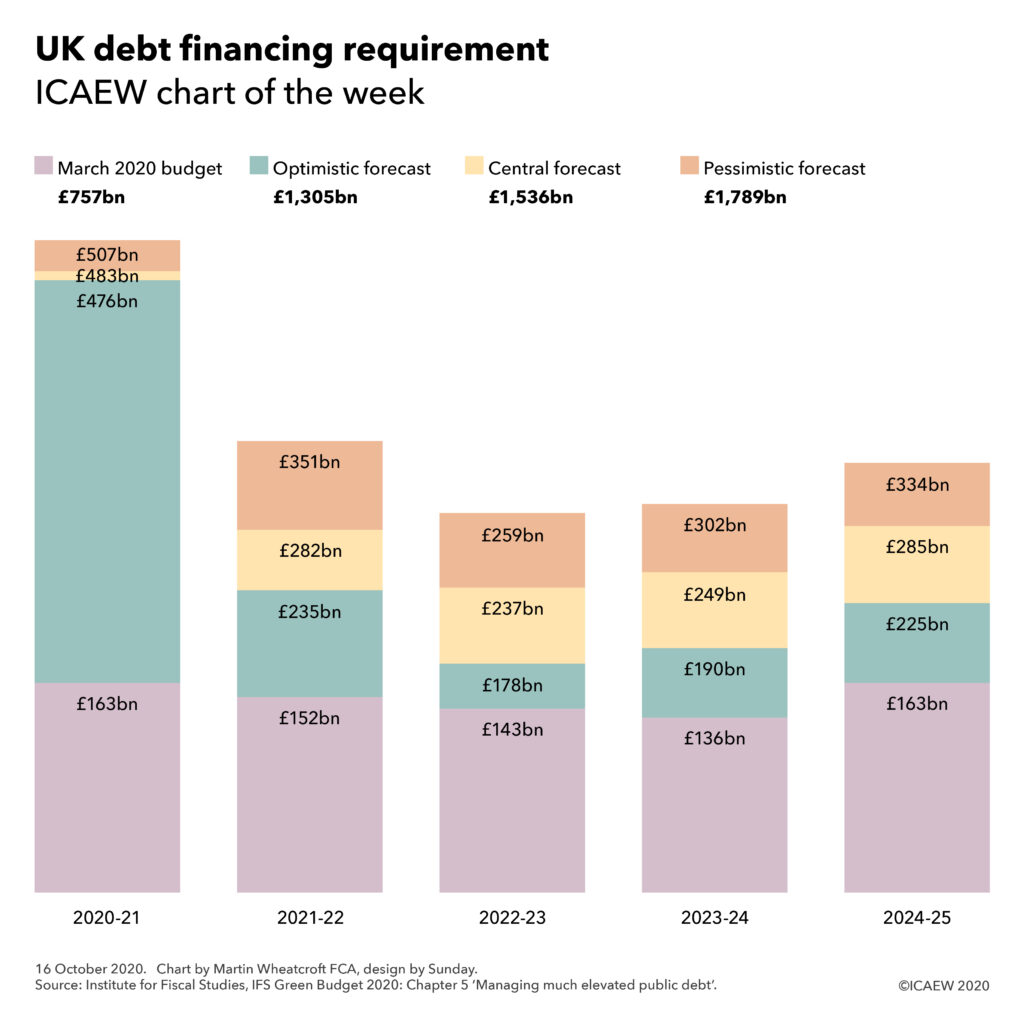

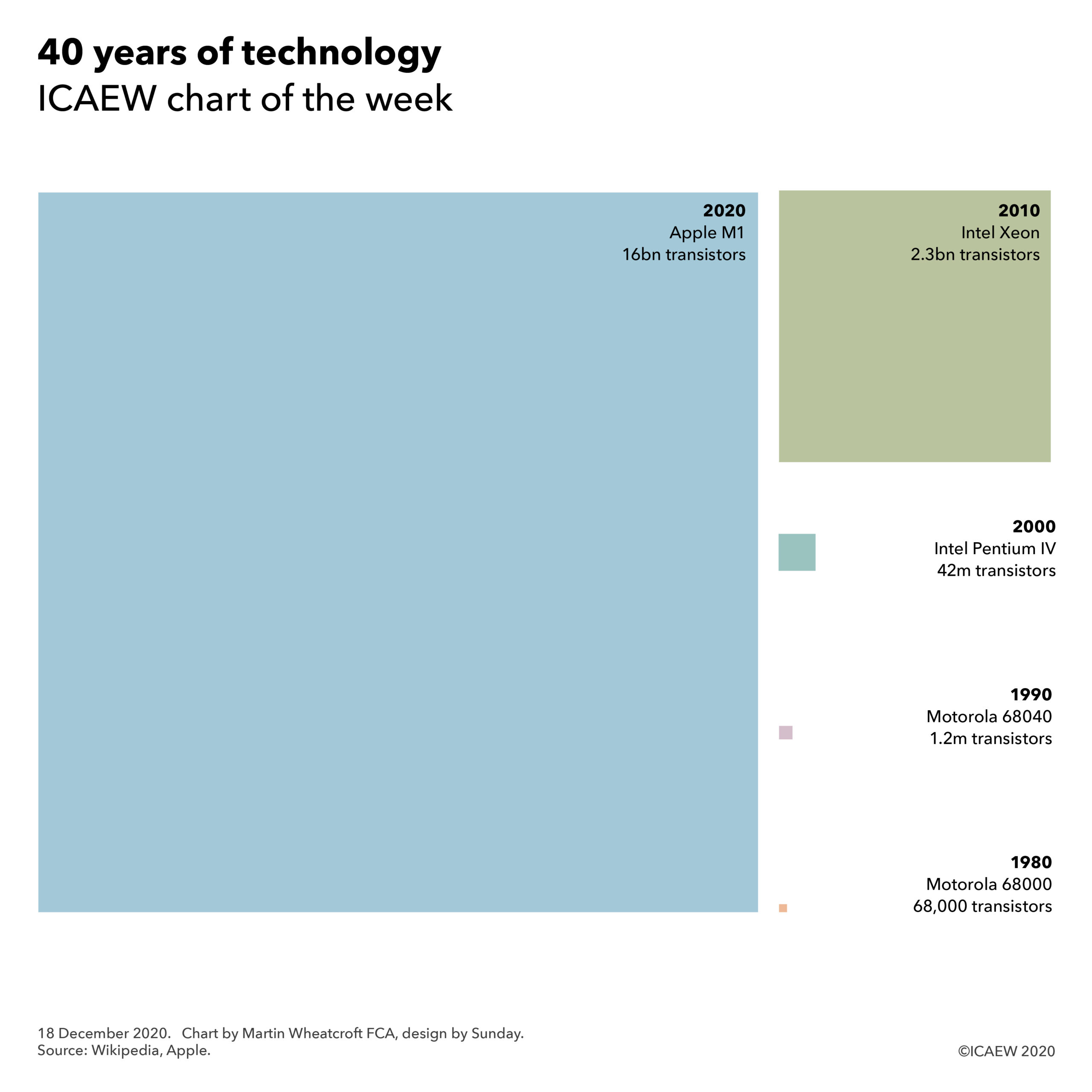

18 December 2020: Our last chart this year takes a look at how technology has advanced over the last forty years, using the number of transistors in central processing unit microprocessors as a proxy for technological advancement.

As we look back over the course of a difficult year, the contribution of technology to keeping the economy working has become apparent. Working from home instead of the office, joining video calls instead of in-person meetings and collaborating using online tools have made it possible for most businesses to continue to operate, albeit perhaps not quite as normal. Similarly, consumers have been able to turn to online retail, streaming services and cashless technology to cope with closed stores and shuttered entertainment venues during lockdowns and tiered restrictions.

This has only been possible as a consequence of huge advancements in technology over the past forty years, with the arrival of affordable personal computers in the 1980s, mobile phones in the 1990s, practical laptops and broadband connections in the 2000s, and smartphones and tablets in the 2010s.

We have used the number of transistors in central processing unit (CPU) microprocessors as a proxy for technological advancement in the #icaewchartoftheweek, but of course there have been many other advancements that have been just as significant, from processing capabilities, memory size, data storage, video quality and broadband speeds.

Back in 1980, the Motorola 68000 chip with 68,000 transistors was the leading chip. It was originally used in high-end business computers before lower production costs enabled it to be included in the original Apple Macintosh launched in 1984. That first Macintosh had separate chips to provide 64K of read-only-memory (ROM), 128k of random-access memory (RAM), a built-in 400KB floppy disk drive and 512 x 342 monochrome display.

A decade later, Intel had caught up with Motorola in chip design, with the Intel 80486 containing 1,180,235 transistors, matching Motorola’s 68040 chip that contained approximately 1.2 million transistors. The Intel 80486 was used in many IBM-compatible PCs while the Motorola 68040 was used in the Commodore Amiga 4000 and HP Series 400 desktops.

Intel was the leading chip-maker in 2000 with the Pentium series of microprocessors being the core of many PCs, albeit against strong competition from AMD’s Athlon x86 compatible CPUs. The Pentium 4 had 42 million transistors, while by 2010, Intel had taken over from Motorola in Apple’s range of computers, although its Xeon series of chips (with 2.3 million transistors in 2010) was primarily used in high-end workstations and servers rather than in desktops or laptops.

In 2020, Apple has started to replace Intel in its computers with the launch of its ARM-based M1 chip. This has 16 billion transistors, more than 235,000 times as many as there were in the leading edge Motorola 68000 of 40 years ago. Processing power and capability is expected to continue to expand: for example, we didn’t have enough room on the chart to fit in AMD’s Epyc Rome microprocessor with 39.5billion transistors on a single chip.

The recently launched M1-based edition of the Apple MacBook Air has a specification that would unimaginable to the personal computer owner of four decades past, with a base configuration containing 8Gb of memory (62,500 times as much RAM as the original Macintosh desktop), 256 GB of storage (640,000 times) and a 2560 x 1600 colour display.

Our ability to cope with the pandemic would have been much harder even a mere decade ago when smartphones were only just emerging, let alone if we had been back in the world of dial-up modems and fax machines of 40 years ago. This demonstrates just how much technology has improved our ability to deal with a global crisis such as the coronavirus pandemic.

The #icaewchartoftheweek is taking a break for a couple of weeks in order to enjoy socially-distanced Christmas and New Year celebrations and will be returning on 8 January 2021. After such a difficult year, we hope you will be able to take some time off to recharge and return to your home-office (and eventually your actual office) energised for what we hope will be a much improved 2021!