As Germany heads to the polls this weekend to elect a new federal parliament, the topic of the public finances has moved to centre stage. Our chart this week looks at the federal budget for 2022 and the current plan to sharply reduce the deficit from 2023 onwards.

The coronavirus pandemic has been accompanied by relaxations in both European and German constitutional limitations on the size of the federal deficit for 2020, 2021 and 2022, with Chancellor Angela Merkel of the Union parties (the Christian Democratic Union (CDU) together with Bavaria’s Christian Social Union (CSU)) and Finance Minister and chancellor-candidate Olaf Scholtz of the Social Democratic Party (SPD) setting out a plan earlier this year to reduce federal borrowing significantly by 2023.

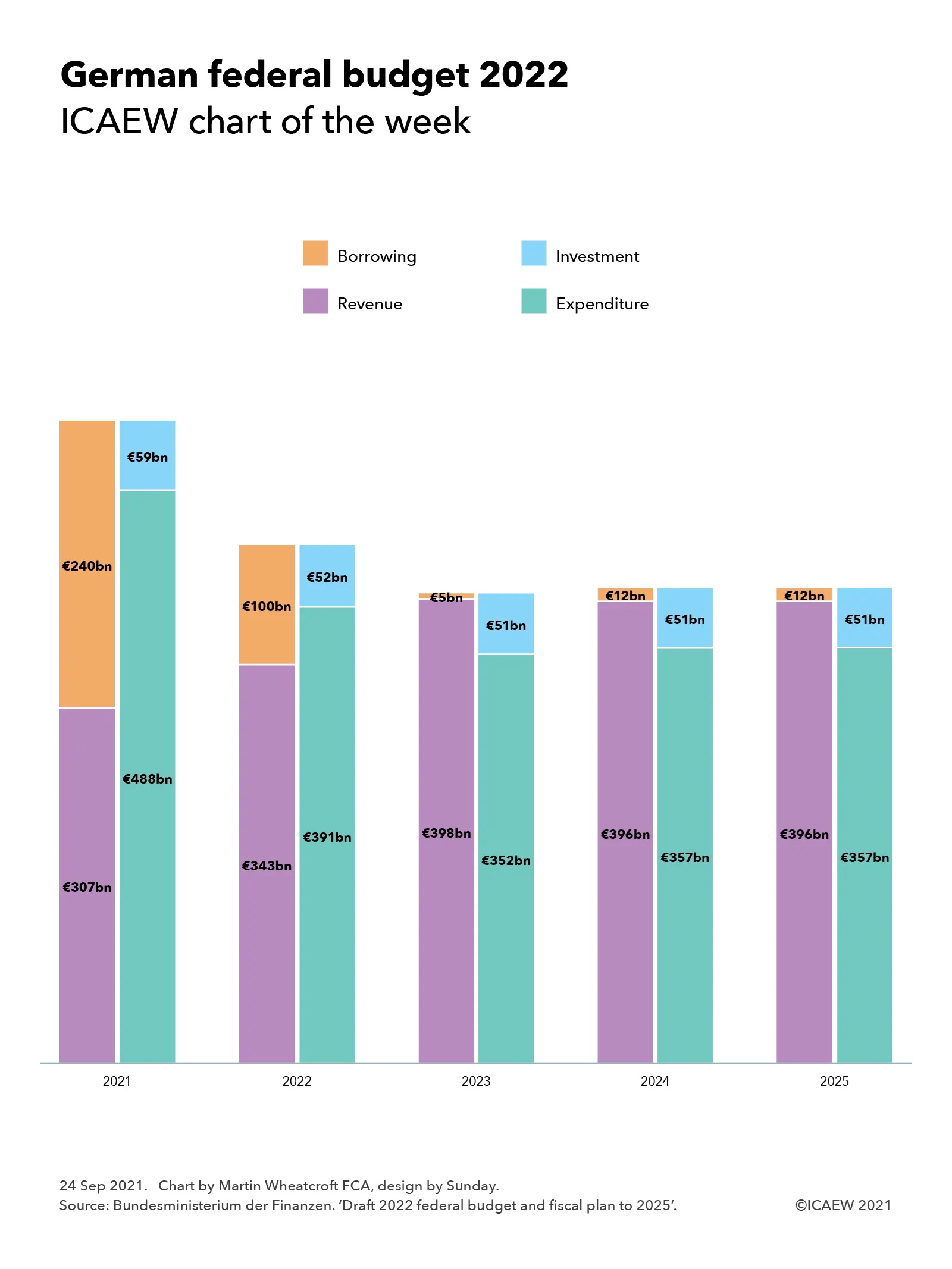

As the #icaewchartoftheweek illustrates, the plan is to continue to run a sizeable deficit of €100bn in 2022 with tax and other revenue of €343bn being offset by €391bn in expenditure and €52bn in investment spending. This is a smaller deficit than the €240bn forecast for the current year (revenue €307bn – expenditure €488bn – investment €59bn) and the €131bn recorded in 2020 (not shown in the chart: revenue €311bn – expenditure €392bn – investment €50bn), both of which contained significant amounts of emergency spending in response to the pandemic.

The hope is that revenues will recover in 2023 to €398bn at the same time as expenditures and investment return to pre-pandemic levels of €352bn and €51bn respectively to leave only a €5bn shortfall to be covered by borrowing. The forecast deficit for both 2024 and 2025 is €12bn, comprising revenue of €396bn in both years, less expenditure of just under €396bn in 2024 and just over €396bn in 2025 and investment in both years of €51bn. It is important to note that this is the budget for the federal government only and excludes the share of joint taxes going to Germany’s states (Länder) as well as expenditures funded from state and local taxation.

The challenge for the three principal candidates for the chancellorship: Olaf Scholtz of the SPD, Armin Laschet of the Union parties and Annalena Baerbock of the Green party, is in how to make promises to spend more on their respective priorities while maintaining the low levels of borrowing required by the constitution outside of fiscal emergencies.

Major flooding earlier this year has put climate change at the top of the electoral agenda, with the need to increase investment to achieve net zero a key theme of party platforms. Together with promises to invest more in infrastructure and the need to cover the cost of more people living longer, higher defence spending and other financial commitments, there are significant questions about whether the path to near-budget balance can be achieved. Given the economic uncertainty, the prospect of returning to the pre-pandemic policy of paying down government debt seems unlikely, although that policy helped reduce general government debt from a peak of 82% of GDP in 2010 following the financial crisis. Despite the additional borrowing because of the pandemic, general government debt is still below that level at somewhere in the region of 75% of GDP – putting Germany in a much better fiscal position than many of its European neighbours, including the UK.

One candidate to be the next finance minister is Christian Lindner of the liberal Free Democratic Party (FDP), a possible partner in either a ‘traffic-light coalition’ of SPD (red), Greens (green) and FDP (yellow) or a ‘Jamaica coalition’ of the Union parties (black), Greens (green) and FDP (yellow) although this will of course depend on how the parties perform in the election on Sunday 26 September. Alice Weidel and Tino Chrupalla, joint leaders of the hard-right Alternative for Germany (AfD), and Janine Wissler & Dietmar Bartch, joint leaders of the Left Party (Die Linke), are considered unlikely to find their way into the federal cabinet in most scenarios.

Unlike in the UK, where a new prime minister customarily takes up residence in 10 Downing Street the next day, there is unlikely to be an instant change in national leadership. Chancellor Angela Merkel and most of her existing Union/SPD ‘Grand coalition’ cabinet are likely to stay in caretaker positions for several weeks or potentially months as fresh coalition negotiations between the parties elected to the Bundestag are concluded.